|

市場調査レポート

商品コード

1913474

商用車向けADAS市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Commercial Vehicle ADAS Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 商用車向けADAS市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

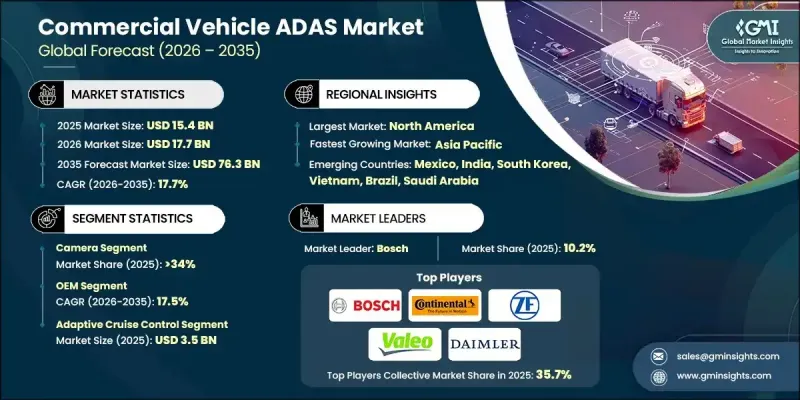

世界の商用車向けADAS市場は、2025年に154億米ドルと評価され、2035年までにCAGR 17.7%で成長し、763億米ドルに達すると予測されています。

この強い成長勢いは、道路安全に対する規制当局の注目度の高まりと、商用車フリートにおける事故関連コスト削減への重視の増大によって牽引されています。フリート所有者や運営者は、ADAS(先進運転支援システム)を、運用上の安全性と効率性を向上させるための必須ツールとしてますます認識しています。これらのシステムは、ドライバーの認識向上、車両制御の改善、手動操作への依存度低減を通じて運転者を支援します。運輸会社がリスク軽減と安全要件への準拠を優先するにつれ、導入は加速しています。技術進歩が需要をさらに強化しており、人工知能と機械学習によりデータ処理の高速化とリアルタイム意思決定の精度向上が実現されています。これらの革新は車両の応答性を高め、システム全体の信頼性を向上させます。世界の商用輸送活動の増加に伴い、ADASの統合は現代の車両設計とフリート管理戦略における重要な要素として、引き続き注目を集めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 154億米ドル |

| 予測金額 | 763億米ドル |

| CAGR | 17.7% |

OEMチャネルセグメントは、2026年から2035年にかけてCAGR17.5%で成長する見込みです。自動車メーカーは生産工程においてADASを直接統合するため、先進的な安全機能を標準装備またはカスタマイズ可能なオプションとして提供することが可能となります。このアプローチにより、システム互換性と性能が向上するとともに、一貫した品質基準が確保されるため、流通構造におけるOEMの強固な地位が説明されます。

アダプティブ・クルーズ・コントロール(ACC)セグメントは2025年に35億米ドルに達しました。このセグメントは、交通の流れに基づいて速度を自動的に調節することで、長時間の運転条件下でもドライバーの快適性をサポートし、車両の安定した運転を維持できることから、主導的地位を維持しています。

米国の商用車向けADAS市場は2025年に39億米ドルに達しました。事故リスクや増加する運用コストに対処するため、フリート事業者が先進安全技術を求め、需要が増加しました。人的要因による運転ミス削減への注力は、国内の商用車フリート全体におけるADAS導入の重要性を引き続き強化しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 商用車に対する政府の厳格な安全規制

- 大型車両および商用車両が関与する交通事故の増加

- フリート安全対策およびテレマティクスソリューションの導入拡大

- 電子商取引とラストマイル配送車両の急速な成長

- 業界の潜在的リスク&課題

- 過酷な気象条件および道路状況における信頼性の課題

- 既存車両へのADAS後付けにおける複雑性

- 市場機会

- 電気商用車におけるADASの需要増加

- 新興市場および発展途上経済圏における成長可能性

- ADASとV2X通信システムの統合

- 老朽化した車両群向けADAS後付けソリューションの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 連邦自動車安全基準(FMVSS)

- IIHS商用車安全評価プログラム

- SAEインターナショナル先進運転支援システム(ADAS)および自動運転基準

- カナダ運輸省自動車安全規制

- 欧州

- EU一般安全規制(EU)

- 国連欧州経済委員会(UNECE)車両規制

- ユーロNCAP商用車安全評価プロトコル

- EU道路安全政策の枠組み

- アジア太平洋地域

- 日本の国土交通省によるADAS安全規制

- 中国GB規格:知能化・ネットワーク化車両

- 中国新車評価プログラム(C-NCAP)ADAS評価ガイドライン

- インド商用車安全基準(AIS)

- ラテンアメリカ

- ラテンNCAP安全評価プロトコル

- ブラジル国家道路交通局(CONTRAN)車両安全決議

- アルゼンチン国家交通安全規制

- メキシコNOM車両安全基準

- 中東・アフリカ

- アラブ首長国連邦連邦交通安全規制

- 南アフリカ共和国道路交通法車両基準

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 持続可能性と環境影響

- 環境影響評価

- 社会的影響と地域社会への貢献

- ガバナンスと企業の社会的責任

- 持続可能な金融と投資動向

- リスク評価

- 市場リスク

- 技術的リスク

- 規制およびコンプライアンスリスク

- サイバーセキュリティとデータプライバシーリスク

- リスク軽減戦略

- 事例研究

- 将来展望と機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:システム別、2022-2035

- アダプティブ・クルーズ・コントロール

- 死角検知システム

- 車線逸脱警報システム

- 自動緊急ブレーキ(AEM)

- 前方衝突警報

- 暗視システム

- ドライバー監視

- タイヤ空気圧監視システム

- ヘッドアップディスプレイ

- 駐車支援システム

- その他

第6章 市場推計・予測:センサー別、2022-2035

- レーダー

- ライダー

- 超音波

- カメラ

- その他

第7章 市場推計・予測:車種別、2022-2035

- LCV

- MCV

- 大型商用車(HCV)

第8章 市場推計・予測:レベル別、2022-2035

- レベル1

- レベル2

- レベル3

- レベル4

第9章 市場推計・予測:推進力別、2022-2035

- 内燃機関(ICE)

- 電気自動車(EV)

- ハイブリッド

第10章 市場推計・予測:流通チャネル別、2022-2035

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- マレーシア

- インドネシア

- ベトナム

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域(MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- Bosch

- Continental

- ZF Friedrichshafen

- Valeo

- Denso

- Mobileye

- Magna

- Autoliv

- Hyundai Mobis

- Aptiv

- Knorr-Bremse

- Forvia(Hella)

- Daimler

- Volvo

- Ford

- 地域企業

- Stoneridge

- Brigade Electronics

- Seeing Machines

- MAN Truck &Bus

- Iveco

- Gauzy

- Renault

- 新興企業

- Huawei

- Horizon Robotics

- Black Sesame

- Applied Intuition