モータースポーツ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Motorsport Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708151

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

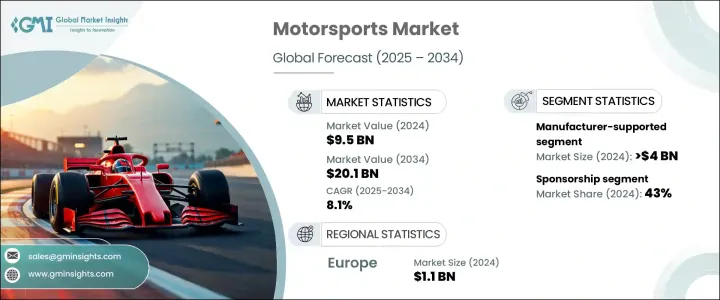

世界のモータースポーツ市場は2024年に95億米ドルに達し、2025年から2034年にかけてCAGR 8.1%で成長すると予測されています。

業界が急速に進化する中、技術の進歩、持続可能性への取り組み、観客の嗜好の変化がモータースポーツの未来を形成しています。同市場は、持続可能性の重視の高まりと、電気およびハイブリッド・レーシング・シリーズの採用によって、顕著な転換期を迎えています。主要な自動車メーカーやレース組織は、電気ドライブトレイン、代替燃料、再生可能素材などのグリーン技術に多額の投資を行っています。このシフトに拍車をかけているのは、規制圧力の高まり、環境意識の高まり、環境にやさしいイノベーションへの需要の高まりです。持続可能性が優先されるようになるにつれ、チームやスポンサーは環境意識の高い新世代のファンや利害関係者にアピールするために戦略を調整しています。

モータースポーツ業界もまた、世界の視聴者数の急増を目の当たりにしており、デジタル・プラットフォーム、放映権、チケット販売、マーチャンダイジングなどの収益源が拡大しています。スポンサーシップ部門は、企業がモータースポーツの広範なリーチを活用して知名度を獲得することで、財政成長の重要な柱であり続けています。2024年には、スポンサーシップが業界総収入の43%を占め、ブランド・パートナーシップの有利な性質が浮き彫りになります。デジタル・エンゲージメントはブランドの露出を増幅し続け、何百万人ものファンがプレミア・イベントにチャンネルを合わせ、スポンサーシップの価値と観客のエンゲージメントを高めています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 95億米ドル |

| 予測金額 | 201億米ドル |

| CAGR | 8.1% |

モータースポーツ市場のオーナーシップ構造には、個人所有チーム、企業支援団体、メーカー支援チームがあります。2024年には、メーカーが支援するセグメントは40億米ドルを生み出し、業界の支配的勢力としての地位を固めました。メーカーはモータースポーツをイノベーションの拠点として活用し、極限のレース条件下でエアロダイナミクス、ハイブリッド・パワートレイン、軽量素材における画期的な進歩をテストしています。これらの開発は、レース性能を向上させるだけでなく、高性能モータースポーツ・エンジニアリングと主流自動車の進歩のギャップを埋めることで、市販自動車技術の進化にも影響を与えています。

ドイツのモータースポーツ市場は2024年に11億米ドルを生み出し、世界のモータースポーツの中心地としての地位を固めました。名だたる自動車大手と世界クラスのレーシング・サーキットを擁するドイツは、多額の投資、人材、スポンサーシップを引き付け続けています。この国は、最先端のモータースポーツ技術の進歩において極めて重要な役割を果たし、権威あるレースイベントを主催し、業界内の革新を促進しています。自動車工学とモータースポーツの卓越性における強力な遺産を持つドイツは、世界のモータースポーツ市場の将来展望を牽引する重要なプレーヤーであり続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- メーカー

- サービスプロバイダー

- 技術プロバイダー

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 電気およびハイブリッドレース技術の進歩

- 世界の視聴者数とデジタル・エンゲージメントの増加

- 自動車メーカーやスポンサーからの投資の増加

- モータースポーツ観光とファン体験の拡大

- 業界の潜在的リスク&課題

- チームとインフラの高コスト

- 環境規制の強化と持続可能性への懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:レースシリーズ別、2021年~2034年

- 主要動向

- ワンメイクシリーズ

- ポルシェ・スーパーカップ

- フェラーリ・チャレンジ

- ランボルギーニ・スーパートロフェオ

- ツーリングカーレース

- 世界ツーリングカー選手権

- BTCC(イギリスツーリングカー選手権)

- DTM(ドイツツーリングカーマスターズ)

- ストックカーレース

- NASCAR(全米自動車競走協会)

- ARCA Menardsシリーズ

- GTレース

- GTシリーズ・ワールドチャレンジ(ブランパンGTシリーズ)

- スーパーGT

- インターコンチネンタルGTチャレンジ

- 耐久レース

- 世界耐久選手権(WEC)

- IMSAウェザーテック・スポーツカー・チャンピオンシップ

- 24Hシリーズ

- ラリー/オフロードレース

- 世界ラリー選手権(WRC)

- 欧州ラリー選手権(ERC)

- ダカールラリー

- SCORE国際オフロードレース

- エクストリームE

- NHRAドラッグレースシリーズ

- フォーミュラレース

- フォーミュラ1

- フォーミュラ2

- フォーミュラE

- インディカー

- バイクレース

- MotoGP

- WorldSBK(スーパーバイク世界選手権)

- FIM EWC(国際モーターサイクリズム連盟耐久世界選手権)

- スーパーモトクロス選手権(MX)

- ブリティッシュ・スーパーバイク選手権(BSB)

- モトクロス世界選手権(MXGP)

- モトアメリカスーパーバイク選手権

第6章 市場推計・予測:収益源別、2021年~2034年

- 主要動向

- 放送

- チケット販売

- スポンサーシップ

- マーチャンダイジング

第7章 市場推計・予測:所有別、2021年~2034年

- 主要動向

- 個人所有

- メーカー支援型

- 企業・スポンサー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Ferrari

- Red Bull Racing

- Mercedes-Benz Grand Prix

- Formula One Group

- Team Penske

- Hendrick Motorsports

- Chip Ganassi Racing

- McLaren Racing

- Aston Martin Aramco Cognizant F1 Team

- Williams Racing

- Alpine F1 Team

- Scuderia AlphaTauri

- Haas F1 Team

- Joe Gibbs Racing

- Richard Childress Racing

- Stewart-Haas Racing

- Toyota Gazoo Racing

- Andretti Autosport

- Rahal Letterman Lanigan Racing

- Arrow McLaren SP

目次

The Global Motorsport Market reached USD 9.5 billion in 2024 and is projected to grow at a CAGR of 8.1% between 2025 and 2034. With the industry rapidly evolving, advancements in technology, sustainability initiatives, and shifting audience preferences are shaping the future of motorsport. The market is experiencing a notable transition, driven by the increasing emphasis on sustainability and the adoption of electric and hybrid racing series. Major automotive manufacturers and racing organizations are investing heavily in green technologies, including electric drivetrains, alternative fuels, and renewable materials. This shift is fueled by mounting regulatory pressures, rising environmental awareness, and the growing demand for eco-friendly innovations. As sustainability becomes a priority, teams and sponsors are aligning their strategies to appeal to a new generation of environmentally conscious fans and stakeholders.

The motorsport industry is also witnessing a surge in global viewership, expanding revenue streams across digital platforms, broadcasting rights, ticket sales, and merchandising. The sponsorship segment remains a critical pillar of financial growth, with companies leveraging motorsport's extensive reach to gain visibility. In 2024, sponsorships accounted for 43% of the industry's total revenue, underscoring the lucrative nature of brand partnerships. Digital engagement continues to amplify brand exposure, with millions of fans tuning in to premier events, driving higher sponsorship values and audience engagement.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $20.1 Billion |

| CAGR | 8.1% |

Ownership structures within the motorsport market include privately owned teams, corporate-backed entities, and manufacturer-supported teams. In 2024, the manufacturer-supported segment generated USD 4 billion, solidifying its position as a dominant force in the industry. Manufacturers utilize motorsport as an innovation hub, testing groundbreaking advancements in aerodynamics, hybrid powertrains, and lightweight materials under extreme racing conditions. These developments are not only enhancing racing performance but also influencing the evolution of commercial automotive technology, bridging the gap between high-performance motorsport engineering and mainstream vehicle advancements.

Germany motorsport market generated USD 1.1 billion in 2024, cementing its status as a global motorsport hub. Home to renowned automotive giants and world-class racing circuits, Germany continues to attract significant investment, talent, and sponsorships. The country plays a pivotal role in the advancement of cutting-edge motorsport technologies, hosting prestigious racing events and fostering innovation within the industry. With a strong legacy in automotive engineering and motorsport excellence, Germany remains a key player in driving the future of the global motorsport market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturer

- 3.2.2 Service provider

- 3.2.3 Technology provider

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Advancements in electric and hybrid racing technology

- 3.7.1.2 Increasing global viewership and digital engagement

- 3.7.1.3 Growing investments from automakers and sponsors

- 3.7.1.4 Expansion of motorsports tourism and fan experiences

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High costs for teams and infrastructure

- 3.7.2.2 Stricter environmental regulations and sustainability concerns

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Racing Series, 2021 - 2034 ($Mn & Number of Visitor)

- 5.1 Key trends

- 5.2 One-Make Series

- 5.2.1 Porsche Supercup

- 5.2.2 Ferrari Challenge

- 5.2.3 Lamborghini Super Trofeo

- 5.3 Touring Car Racing

- 5.3.1 World Touring Car Championship

- 5.3.2 BTCC (British Touring Car Championship)

- 5.3.3 DTM (Deutsche Tourenwagen Masters)

- 5.4 Stock Car Racing

- 5.4.1 NASCAR (National Association for Stock Car Auto Racing)

- 5.4.2 ARCA Menards Series

- 5.5 GT Racing

- 5.5.1 GT Series World Challenge (Blacpain GT Series)

- 5.5.2 Super GT

- 5.5.3 Intercontinental GT Challenge

- 5.6 Endurance Racing

- 5.6.1 World Endurance Championship (WEC)

- 5.6.2 IMSA WeatherTech SportsCar Championship

- 5.6.3 24H Series

- 5.7 Rally and Off-Road Racing

- 5.7.1 World Rally Championship (WRC)

- 5.7.2 European Rally Championship (ERC)

- 5.7.3 Dakar Rally

- 5.7.4 SCORE International Off-Road Racing

- 5.7.5 Extreme E

- 5.7.6 NHRA Drag Racing Series

- 5.8 Formula Racing

- 5.8.1 Formula 1

- 5.8.2 Formula 2

- 5.8.3 Formula E

- 5.8.4 IndyCar

- 5.9 Motorbike Racing

- 5.9.1 MotoGP

- 5.9.2 WorldSBK (World Superbike Championship)

- 5.9.3 FIM EWC (Fédération Internationale de Motocyclisme Endurance World Championship)

- 5.9.4 SuperMotoCross Championship (MX)

- 5.9.5 British SuperBikes (BSB)

- 5.9.6 MotoCross World Championship (MXGP)

- 5.9.7 MotoAmerica Superbike Championship

Chapter 6 Market Estimates & Forecast, By Revenue Source, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Broadcasting

- 6.3 Ticket sales

- 6.4 Sponsorship

- 6.5 Merchandising

Chapter 7 Market Estimates & Forecast, By Ownership, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Privately-owned

- 7.3 Manufacturer-supported

- 7.4 Corporate & sponsored

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.5.3 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Ferrari

- 9.2 Red Bull Racing

- 9.3 Mercedes-Benz Grand Prix

- 9.4 Formula One Group

- 9.5 Team Penske

- 9.6 Hendrick Motorsports

- 9.7 Chip Ganassi Racing

- 9.8 McLaren Racing

- 9.9 Aston Martin Aramco Cognizant F1 Team

- 9.10 Williams Racing

- 9.11 Alpine F1 Team

- 9.12 Scuderia AlphaTauri

- 9.13 Haas F1 Team

- 9.14 Joe Gibbs Racing

- 9.15 Richard Childress Racing

- 9.16 Stewart-Haas Racing

- 9.17 Toyota Gazoo Racing

- 9.18 Andretti Autosport

- 9.19 Rahal Letterman Lanigan Racing

- 9.20 Arrow McLaren SP

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日