|

市場調査レポート

商品コード

1708147

自動車荷室フロア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Load Floor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車荷室フロア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月06日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

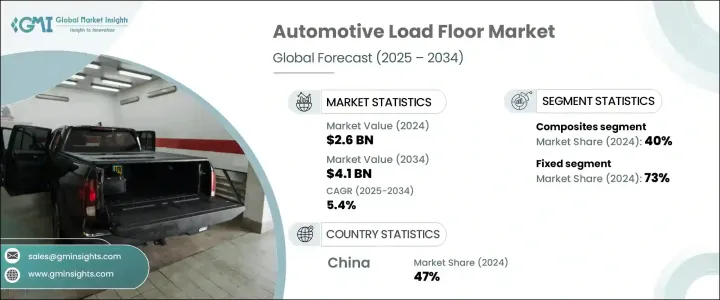

自動車荷室フロアの世界市場は2024年に26億米ドルに達し、2025年から2034年にかけてCAGR 5.4%で成長すると予測されています。

この拡大には、高度な設計と強化された機能を必要とする電気自動車と自律走行車(EVとAV)の需要増加が拍車をかけています。電気自動車のバッテリーパックは一般的に床下に配置されるため、自動車メーカーは超軽量でありながら耐久性のある荷室フロアにますます重点を置くようになっています。その結果、複合材料や熱可塑性プラスチックのような先端材料が、スペース効率の改善、荷室容量の最適化、構造的完全性の維持のために採用されるようになっています。

燃費と持続可能性が重視されるようになり、メーカーはカーボンフットプリントを削減するために軽量材料を優先しています。非強化ポリマー複合材料、熱可塑性プラスチック、ハニカム構造を荷室に組み込むことは、耐久性を犠牲にすることなく車両全体の重量を下げる上で重要な役割を果たします。この動向は、自動車メーカーが厳しい排ガス規制と燃費の改善に取り組む中で勢いを増しています。持続可能なソリューションへのシフトは、消費者の意識の高まりや、環境に優しい自動車部品に焦点を当てた規制の義務化によってさらに加速しています。高性能材料の需要は、機能性と快適性を高めるために軽量かつ堅牢な荷室フロアソリューションが不可欠であるプレミアム車や高級車の生産台数の増加にも後押しされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 5.4% |

市場は、ハードボード、ハニカムポリプロピレン、フルーテッドポリプロピレン、複合材など、素材タイプ別に区分されます。複合材料は、軽量、高強度、耐湿性に優れていることから、2024年のシェアは40%で市場を独占しています。炭素繊維強化プラスチック(CFRP)とガラス繊維複合材料は、車両重量を効果的に削減しながら優れた構造的支持を提供するため、人気を集めています。これらの材料は、燃費効率と二酸化炭素排出量の低減に大きく貢献するため、持続可能性の目標を達成しようとする自動車メーカーの間で好ましい選択となっています。

荷室フロアは、その運用特性により固定式とスライド式に分類されます。2024年には、固定式荷室フロアが市場シェアの73%を占め、今後も力強い成長が見込まれます。固定式荷室フロアは、卓越した構造安定性、耐久性、コスト効率を提供し、乗用車や商用車の標準的な選択肢となっています。これらのフロアは、最適な荷重分散と強化された安全性を確保するため、スライド式の代替品よりも有利です。

中国の自動車荷室フロア市場は2024年に5億2,000万米ドルを生み出し、同国の電気自動車部門の急成長により世界市場をリードしています。軽量で高性能な荷室フロアソリューションに対する需要の増加は、複合材料や環境に優しい材料の使用を促進する政府の奨励策によってさらに強化されています。支援政策、技術の進歩、国内自動車メーカーの拡大が相まって、中国は自動車荷室フロア業界の主要プレーヤーとしての地位を強化しています。世界市場がより大きな持続可能性と革新に向かう中、中国の役割は、自動車荷室フロアソリューションの将来の展望を形成する上で極めて重要であり続けると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品メーカー

- ティア1サプライヤー

- 相手先商標製品メーカー(OEM)

- アフターマーケット・サプライヤー

- 利益率分析

- 価格動向

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 軽量素材への需要の高まり

- 電気自動車と自律走行車の拡大

- 貨物管理ソリューションに対する消費者需要の増加

- 厳しい燃費・排ガス規制

- 製造技術の進歩

- 業界の潜在的リスク&課題

- 自動車生産の変動

- 材料コストの変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ハードボード

- フルートポリプロピレン

- ハニカムポリプロピレン

- 複合材料

第6章 市場推計・予測:操作別、2021年~2034年

- 主要動向

- 固定式

- スライド式

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- ABC Technologies

- Applied Component Technology

- Arlington Industries

- ASG Group

- Autoneum

- CIE Automotive

- Covestro

- DS Smith

- Gemini Group

- Grudem

- Huntsman

- IDEAL Automotive

- KRAIBURG TPE

- Nagase America

- Recticel

- SA Automotive

- Sonoco Products

- Tricel Honeycomb

- UFP Technologies

- Woodbridge

The Global Automotive Load Floor Market reached USD 2.6 billion in 2024 and is projected to grow at a CAGR of 5.4% during 2025-2034. This expansion is fueled by the rising demand for electric and autonomous vehicles (EVs and AVs), which require advanced designs and enhanced functionality. Automakers are increasingly focusing on ultra-lightweight yet durable load floors, as battery packs in electric vehicles are typically positioned beneath the floor. As a result, advanced materials like composites and thermoplastics are being adopted to improve space efficiency, optimize cargo capacity, and maintain structural integrity.

With a growing emphasis on fuel economy and sustainability, manufacturers are prioritizing lightweight materials to reduce carbon footprints. The integration of non-reinforced polymer composites, thermoplastics, and honeycomb structures into load floors plays a crucial role in lowering overall vehicle weight without sacrificing durability. This trend is gaining momentum as automakers work toward stringent emissions regulations and improved fuel efficiency. The shift toward sustainable solutions is further accelerated by increasing consumer awareness and regulatory mandates focusing on eco-friendly automotive components. The demand for high-performance materials is also driven by the rising production of premium and luxury vehicles, where lightweight yet robust load floor solutions are essential for enhanced functionality and comfort.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 billion |

| Forecast Value | $4.1 billion |

| CAGR | 5.4% |

The market is segmented by material type, including hardboard, honeycomb polypropylene, fluted polypropylene, and composites. Composites dominated the market in 2024 with a 40% share, driven by their lightweight, high-strength, and moisture-resistant properties. Carbon fiber reinforced plastic (CFRP) and glass fiber composite materials are gaining traction as they offer superior structural support while effectively reducing vehicle weight. These materials contribute significantly to fuel efficiency and lower carbon emissions, making them a preferred choice among automakers striving to meet sustainability goals.

Load floors are classified into fixed and sliding systems based on their operational characteristics. In 2024, fixed load floors accounted for 73% of the market share and are expected to continue experiencing robust growth. Fixed-load floors provide exceptional structural stability, durability, and cost-efficiency, making them the standard choice for passenger and commercial vehicles. These floors ensure optimal load distribution and enhanced security, making them more favorable than sliding alternatives.

China Automotive Load Floor Market generated USD 520 million in 2024, leading the global market due to the country's rapidly growing electric vehicle sector. Increasing demand for lightweight, high-performance load floor solutions is further reinforced by government incentives promoting the use of composites and environmentally friendly materials. The combination of supportive policies, technological advancements, and the expansion of domestic automakers strengthens China's position as a key player in the automotive load floor industry. As the global market moves toward greater sustainability and innovation, China's role is expected to remain pivotal in shaping the future landscape of automotive load floor solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Tier 1 suppliers

- 3.2.4 Original Equipment Manufacturers (OEMs)

- 3.2.5 Aftermarket suppliers

- 3.3 Profit margin analysis

- 3.4 Price trends

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for lightweight materials

- 3.9.1.2 Expansion of electric and autonomous vehicles

- 3.9.1.3 Increasing consumer demand for cargo management solutions

- 3.9.1.4 Stringent fuel efficiency and emission regulations

- 3.9.1.5 Advancements in manufacturing technologies

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Fluctuations in automotive production

- 3.9.2.2 Material cost volatility

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardboard

- 5.3 Fluted polypropylene

- 5.4 Honeycomb polypropylene

- 5.5 Composites

Chapter 6 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Fixed

- 6.3 Sliding

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicle (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ABC Technologies

- 10.2 Applied Component Technology

- 10.3 Arlington Industries

- 10.4 ASG Group

- 10.5 Autoneum

- 10.6 CIE Automotive

- 10.7 Covestro

- 10.8 DS Smith

- 10.9 Gemini Group

- 10.10 Grudem

- 10.11 Huntsman

- 10.12 IDEAL Automotive

- 10.13 KRAIBURG TPE

- 10.14 Nagase America

- 10.15 Recticel

- 10.16 SA Automotive

- 10.17 Sonoco Products

- 10.18 Tricel Honeycomb

- 10.19 UFP Technologies

- 10.20 Woodbridge