|

市場調査レポート

商品コード

1708144

自動車用タッチスクリーン制御システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Touch Screen Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用タッチスクリーン制御システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月05日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

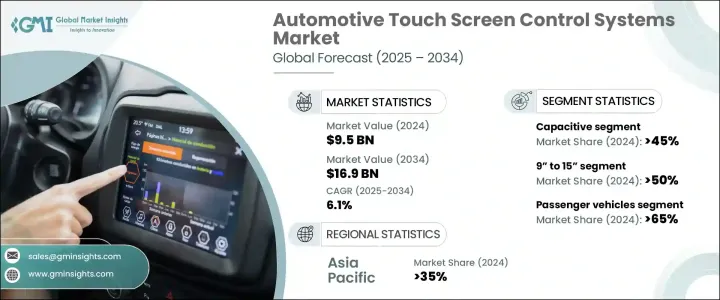

世界の自動車用タッチスクリーン制御システム市場は、2024年に95億米ドルとなり、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。

市場拡大の背景には、特に電気自動車(EV)やコネクテッドカー技術の急速な普及に伴い、最新の自動車における高度なタッチインターフェースに対する需要が高まっていることがあります。自動車メーカーは、運転体験を向上させ、車両機能を合理化するために、ユーザーフレンドリーで高性能なタッチスクリーンシステムを優先しています。

自動車業界がデジタル変革を遂げる中、タッチスクリーン制御システムは次世代自動車の中心的な要素となっています。EVの台頭は、バッテリー監視、回生ブレーキ、エネルギー効率の高い空調設定を容易にする特殊なタッチインターフェースの開発に大きな影響を与えています。また、自動車メーカーは人工知能(AI)とクラウドベースのテクノロジーを統合してタッチスクリーンの機能を強化し、シームレスな接続、パーソナライズされた設定、予測制御を可能にしています。デジタル・コックピットへのシフトは市場の成長をさらに後押ししており、メーカーは高解像度のタッチスクリーンを通じて、洗練されたインフォテインメント・システム、インタラクティブな車両制御、安全機能の強化を提供することに注力しています。直感的で多機能なインターフェースを好む消費者の増加により、優れた応答性、マルチタッチ機能、鮮明な表示品質を提供する静電容量式タッチパネルの需要が急増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 95億米ドル |

| 予測金額 | 169億米ドル |

| CAGR | 6.1% |

車載用タッチスクリーン市場はタッチパネル技術によって区分され、2024年の市場シェアは静電容量式タッチパネルが45%を占める。入力を登録するために物理的な圧力を必要とする抵抗膜方式タッチパネルとは異なり、静電容量式タッチスクリーンはスムーズでシームレスなインタラクションを提供するため、インフォテインメント・システム、ナビゲーション・コントロール、空調設定などに適しています。これらの先進的なタッチスクリーンは、ユーザーの利便性を向上させるだけでなく、ボタンのない洗練されたダッシュボードを可能にすることで、自動車の美観も向上させます。

スクリーンサイズも重要な市場セグメンテーションのひとつで、9インチから15インチのカテゴリーが2024年の市場シェア50%を占める。このサイズ範囲は、使いやすさと視認性の完璧なバランスを提供し、現代の自動車の標準となっています。中型タッチスクリーンは、車載ナビゲーション、メディアコントロール、システム設定に広く使用されており、没入感がありながら押し付けがましくないインターフェースを提供しています。自動車メーカーは、タッチスクリーンの機能を強化するために、AI主導の機能、カスタマイズ可能なディスプレイ、音声アシストコントロールを活用しており、高度にインタラクティブでパーソナライズされたユーザー体験を保証しています。

アジア太平洋地域は、2024年の自動車用タッチスクリーン制御システム市場で35%の大きなシェアを占め、中国が主要な成長促進要因として浮上しています。同国は、活況を呈する電気自動車部門とスマート自動車技術への投資の増加により、2034年までに30億米ドルを生み出すと予想されています。自動車メーカーがEVやコネクテッド・カーに高度なデジタル・インターフェースを統合する中、AIを搭載した大型タッチスクリーンの普及が加速しています。競合情勢が激化する中、市場各社はイノベーションに注力し、ジェスチャー認識、触覚フィードバック、AR(拡張現実)ディスプレイなどの最先端機能を取り入れて、進化する自動車情勢で優位に立とうとしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤー

- メーカー

- システムインテグレーター

- テクノロジープロバイダー

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- コスト分析

- 規制状況

- 影響要因

- 促進要因

- 車載インフォテインメントに対する需要の高まり

- 電気自動車とコネクテッドカーの採用増加

- タッチスクリーン技術の進歩

- 直感的なタッチコントロールと音声アシストインターフェースの採用増加

- 業界の潜在的リスク&課題

- 耐久性と信頼性への懸念

- 高度なタッチスクリーンシステムの高コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タッチパネル別、2021年~2034年

- 主要動向

- 抵抗膜方式

- 赤外線式

- 静電容量式

- 光学イメージング

第6章 市場推計・予測:スクリーンサイズ別、2021年~2034年

- 主要動向

- 9インチ以下

- 9インチ以上15インチ未満

- 15インチ以上

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- インフォテインメントシステム

- ナビゲーションシステム

- クライメートコントロール

- ドライバー支援機能

- 車両診断

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Analog

- AU Optronics

- Bosch

- Continental

- Denso

- Dingtouch

- Eaton

- Harman

- Infineon

- Kyocera

- LG Display

- Magneti Marelli

- Microchip

- Nippon Seiki

- Pioneer

- Sharp

- Synaptics

- TPK Holding

- Valeo

- Visteon

The Global Automotive Touch Screen Control Systems Market was valued at USD 9.5 billion in 2024 and is projected to grow at a CAGR of 6.1% between 2025 and 2034. The market expansion is driven by the increasing demand for advanced touch interfaces in modern vehicles, particularly with the rapid adoption of electric vehicles (EVs) and connected car technologies. Automakers are prioritizing user-friendly, high-performance touchscreen systems to enhance the driving experience and streamline vehicle functionalities.

As the automotive industry undergoes a digital transformation, touchscreen control systems have become a central component of next-generation vehicles. The rise of EVs has significantly influenced the development of specialized touch interfaces that facilitate battery monitoring, regenerative braking, and energy-efficient climate settings. Automakers are also integrating artificial intelligence (AI) and cloud-based technologies to enhance touchscreen capabilities, allowing for seamless connectivity, personalized settings, and predictive controls. The shift towards digital cockpits is further fueling market growth, with manufacturers focusing on delivering sophisticated infotainment systems, interactive vehicle controls, and enhanced safety features through high-resolution touchscreens. Increasing consumer preference for intuitive, multi-functional interfaces has led to a surge in demand for capacitive touch panels, which offer superior responsiveness, multi-touch capabilities, and crystal-clear display quality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 6.1% |

The automotive touch screen market is segmented based on touch panel technology, with capacitive touch panels holding a dominant 45% market share in 2024. Unlike resistive touch panels, which require physical pressure to register inputs, capacitive touch screens provide a smooth and seamless interaction, making them the preferred choice for infotainment systems, navigation controls, and climate settings. These advanced touchscreens not only improve user convenience but also enhance vehicle aesthetics by enabling sleek, button-free dashboards.

Screen size is another key market segmentation, with the 9" to 15" category accounting for a 50% market share in 2024. This size range has become the standard for modern vehicles, offering the perfect balance between usability and visibility. Mid-sized touchscreens are widely used for in-car navigation, media control, and system settings, providing an immersive yet non-intrusive interface. Automakers are leveraging AI-driven features, customizable displays, and voice-assisted controls to enhance touchscreen functionality, ensuring a highly interactive and personalized user experience.

Asia Pacific accounted for a significant 35% share of the Automotive Touch Screen Control Systems Market in 2024, with China emerging as a major growth driver. The country is expected to generate USD 3 billion by 2034, fueled by its booming electric vehicle sector and increasing investment in smart vehicle technologies. The push for AI-powered, large-format touchscreens is accelerating adoption rates as automakers integrate advanced digital interfaces into EVs and connected vehicles. As competition intensifies, market players are focusing on innovation, incorporating cutting-edge features such as gesture recognition, haptic feedback, and augmented reality (AR) displays to stay ahead in the evolving automotive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Suppliers

- 3.1.2 Manufacturers

- 3.1.3 System Integrators

- 3.1.4 Technology Providers

- 3.1.5 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Cost analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing demand for in-vehicle infotainment

- 3.9.1.2 Rising adoption of electric and connected vehicles

- 3.9.1.3 Increasing advancements in touchscreen technology

- 3.9.1.4 Rising adoption of intuitive touch controls and voice-assisted interfaces

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Durability and reliability concerns

- 3.9.2.2 High cost of advanced touchscreen systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Touch Panel, 2021 – 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Resistive

- 5.3 Infrared

- 5.4 Capacitive

- 5.5 Optical imaging

Chapter 6 Market Estimates & Forecast, By Screen Size, 2021 – 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Below 9”

- 6.3 9” to 15”

- 6.4 Above 15”

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 – 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Infotainment systems

- 8.3 Navigation systems

- 8.4 Climate control

- 8.5 Driver assistance features

- 8.6 Vehicle diagnostics

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Analog

- 10.2 AU Optronics

- 10.3 Bosch

- 10.4 Continental

- 10.5 Denso

- 10.6 Dingtouch

- 10.7 Eaton

- 10.8 Harman

- 10.9 Infineon

- 10.10 Kyocera

- 10.11 LG Display

- 10.12 Magneti Marelli

- 10.13 Microchip

- 10.14 Nippon Seiki

- 10.15 Pioneer

- 10.16 Sharp

- 10.17 Synaptics

- 10.18 TPK Holding

- 10.19 Valeo

- 10.20 Visteon