再製造自動車部品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Remanufactured Automotive Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708140

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

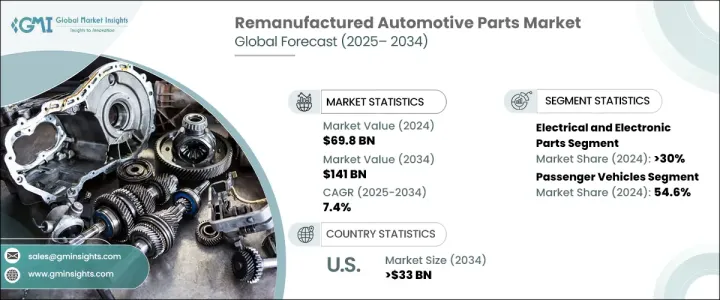

世界の再製造自動車部品市場は2024年に698億米ドルに達し、2025年から2034年にかけてCAGR 7.4%で成長すると予測されています。

再製造自動車部品の需要は、技術の進歩、環境面でのメリット、コスト効率の高さなどが相まって急増しています。持続可能性への関心と循環経済の原則が勢いを増すにつれ、再生部品は新品部品に代わる好ましい選択肢として浮上しています。これらの部品は、厳格な再生工程を経て、OEM(相手先商標製品製造)規格に適合するか、それを上回ることを保証すると同時に、材料廃棄とエネルギー消費を削減しています。その結果、自動車メーカーも消費者も再製造自動車部品の利点を認識し、市場の大幅な拡大を後押ししています。

自動化、デジタル化、材料科学の革新の急速な統合は、再製造プロセスに革命をもたらし、製品の品質と信頼性を向上させました。最新の技術により、再製造業者は中古部品を効率的に新品に近い状態に復元し、最適な性能と寿命を確保することができます。この動向は、電気自動車(EV)やハイブリッド車の普及が進み、より多くの高度な部品に依存するようになったことでさらに強まっています。さらに、排出ガスや持続可能性に関する政府の厳しい規制が、自動車メーカーに再製造ソリューションへの投資を促し、市場の成長を後押ししています。高品質な再生部品が競争力のある価格で入手できるようになったことで、新品の部品に代わる費用対効果が高く環境に優しい代替品を求める自動車所有者が増えており、消費者の購買意思決定に影響を与えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 698億米ドル |

| 予測金額 | 1,410億米ドル |

| CAGR | 7.4% |

再製造自動車部品市場は、電気・電子部品、エンジン、トランスミッション、ホイール、ブレーキなどの主要部品カテゴリーに区分されます。2024年には、電気・電子部品セグメントが最大の市場シェアを占め、30%を占める。センサー、電動ドライブトレイン、インフォテインメント・システムなど、先進的な自動車技術への依存の高まりが、電気・電子部品の再生産需要を高めています。これらの部品は、修理・交換コストを下げつつ、車両システムの寿命を延ばす持続可能な方法を提供します。再生電子部品の統合は、自動車の効率を高めるだけでなく、電子機器廃棄物を大幅に削減し、市場をさらに前進させる。

車種別では、再製造自動車部品市場には乗用車と商用車が含まれます。乗用車セグメントは2024年の市場を独占し、54.6%のシェアを確保しました。この成長は、自動車部品の寿命を延ばし、自動車生産における二酸化炭素排出量を削減しようとする取り組みが大きな原動力となっています。再製造スターター、オルタネーター、高電圧バッテリーの採用が増加していることは、部品の再利用と改修によって環境への影響を最小限に抑え、貴重な資源を節約するという、業界の循環経済への移行と一致しています。自動車メーカーが持続可能な生産と修理ソリューションを優先していることから、乗用車セクターにおける再生部品の需要は加速すると予想されます。

北米は2024年の再製造自動車部品市場で35%の大きなシェアを占め、米国が圧倒的な貢献国として浮上しています。予測によると、米国市場は2034年までに330億米ドルに達し、持続可能性、費用対効果、OEMが支援する再製造プログラムへの注目が高まっていることがその要因となっています。大手自動車メーカーは再製造イニシアチブを拡大し、需要の増加に対応するため、多様な再製造部品を提供しています。厳しい環境政策、強力なアフターマーケット産業、消費者の意識の高まりにより、北米は依然として自動車再製造部品市場の世界的拡大を牽引する主要地域となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 自動車メーカー

- 第三者再製造業者

- リバース・ロジスティクス・プロバイダー

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュースと取り組み

- コスト内訳

- 価格動向

- 規制状況

- 影響要因

- 促進要因

- 再製造プロセスの改善

- 環境政策の強化

- 廃棄物削減の重視

- 再生部品の使用によるコスト削減の増加

- 業界の潜在的リスク&課題

- 消費者のネガティブな認識

- サプライチェーンの複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 電気・電子部品

- エンジン

- トランスミッション

- ホイールとブレーキ

- その他

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:供給別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Andre Niermann

- BBB Industries

- BorgWarner

- Bosch

- Cardone

- Carwood

- Caterpillar

- Denso

- Detroit Diesel

- Eaton

- Jasper Engines &Transmissions

- Lucas Electrical

- Marelli

- Maval

- Motorcar Parts of America

- NAPA

- Stellantis

- Teamec

- Valeo

- ZF

目次

The Global Remanufactured Automotive Parts Market reached USD 69.8 billion in 2024 and is projected to grow at a CAGR of 7.4% between 2025 and 2034. The demand for remanufactured automotive parts is surging due to a combination of technological advancements, environmental benefits, and cost-efficiency. As sustainability concerns and circular economy principles gain momentum, remanufactured components are emerging as a preferred alternative to new parts. These components undergo rigorous refurbishment processes, ensuring they meet or exceed original equipment manufacturer (OEM) standards while reducing material waste and energy consumption. As a result, automakers and consumers alike are recognizing the advantages of remanufactured automotive parts, driving substantial market expansion.

The rapid integration of automation, digitalization, and material science innovations has revolutionized the remanufacturing process, enhancing product quality and reliability. With modern technology, remanufacturers can efficiently restore used parts to near-new condition, ensuring optimal performance and longevity. This trend is further bolstered by the rising adoption of electric vehicles (EVs) and hybrid models, which rely on a greater number of sophisticated components. Additionally, stringent government regulations on emissions and sustainability initiatives are pushing automakers to invest in remanufacturing solutions, reinforcing market growth. The increasing availability of high-quality remanufactured parts at competitive prices is influencing consumer purchasing decisions as more vehicle owners seek cost-effective and environmentally friendly alternatives to new components.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $69.8 Billion |

| Forecast Value | $141 Billion |

| CAGR | 7.4% |

The remanufactured automotive parts market is segmented into key component categories, including electrical and electronic parts, engines, transmissions, wheels, and brakes. In 2024, the electrical and electronic parts segment held the largest market share, accounting for 30%. The growing reliance on advanced vehicle technologies, such as sensors, electric drivetrains, and infotainment systems, has amplified the demand for remanufactured electrical and electronic components. These components offer a sustainable way to extend the lifespan of vehicle systems while lowering repair and replacement costs. The integration of remanufactured electronics not only enhances vehicle efficiency but also significantly reduces electronic waste, further driving the market forward.

By vehicle type, the remanufactured automotive parts market includes passenger and commercial vehicles. The passenger vehicle segment dominated the market in 2024, securing a 54.6% share. This growth is largely driven by efforts to extend the longevity of automotive components and reduce the carbon footprint of vehicle production. The increasing adoption of remanufactured starters, alternators, and high-voltage batteries aligns with the industry's transition toward a circular economy, where reusing and refurbishing parts minimizes environmental impact and conserves valuable resources. With automakers prioritizing sustainable production and repair solutions, the demand for remanufactured parts in the passenger vehicle sector is expected to accelerate.

North America held a significant 35% share of the remanufactured automotive parts market in 2024, with the U.S. emerging as the dominant contributor. Projections indicate that the U.S. market will reach USD 33 billion by 2034, fueled by an increasing focus on sustainability, cost-effectiveness, and OEM-backed remanufacturing programs. Major automotive manufacturers are expanding their remanufacturing initiatives, offering a diverse range of remanufactured components to cater to rising demand. With stringent environmental policies, a strong aftermarket industry, and growing consumer awareness, North America remains a key region driving the global expansion of the remanufactured automotive parts market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automakers

- 3.1.2 Third-party remanufacturers

- 3.1.3 Reverse logistics providers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Cost breakdown

- 3.8 Price trend

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Improving remanufacturing processes

- 3.10.1.2 Stricter environmental policies

- 3.10.1.3 Growing emphasis on reducing waste

- 3.10.1.4 Increasing cost savings by using remanufactured parts

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Negative consumer perception

- 3.10.2.2 Supply chain complexity

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 – 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electrical and electronic parts

- 5.3 Engine

- 5.4 Transmission

- 5.5 Wheels and brakes

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Supply, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Andre Niermann

- 9.2 BBB Industries

- 9.3 BorgWarner

- 9.4 Bosch

- 9.5 Cardone

- 9.6 Carwood

- 9.7 Caterpillar

- 9.8 Denso

- 9.9 Detroit Diesel

- 9.10 Eaton

- 9.11 Jasper Engines & Transmissions

- 9.12 Lucas Electrical

- 9.13 Marelli

- 9.14 Maval

- 9.15 Motorcar Parts of America

- 9.16 NAPA

- 9.17 Stellantis

- 9.18 Teamec

- 9.19 Valeo

- 9.20 ZF

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日