|

市場調査レポート

商品コード

1913435

車載Wi-Fi市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測In-car Wi-Fi Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 車載Wi-Fi市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

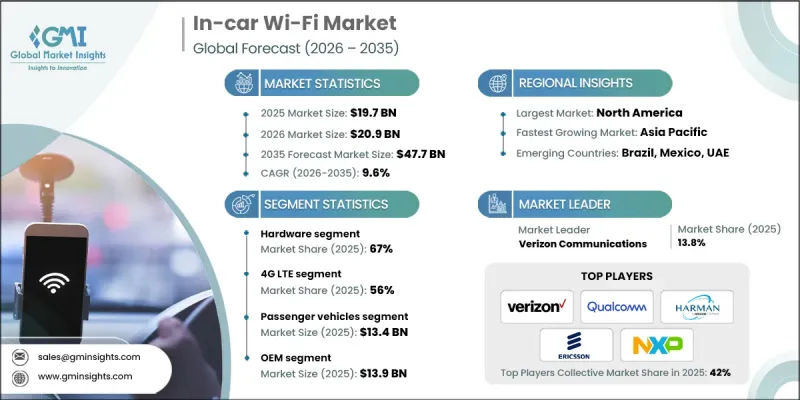

世界の車載Wi-Fi市場は、2025年に197億米ドルと評価され、2035年までにCAGR 9.6%で成長し、477億米ドルに達すると予測されています。

この成長は、コネクテッドカーの普及率上昇と、移動中も途切れないデジタルアクセスを求める消費者の期待の高まりによって支えられています。自動車メーカーやモビリティプロバイダーは、ユーザーの快適性、システムの知能化、運用パフォーマンスの向上を図るため、ワイヤレス接続を標準装備として組み込むケースが増加しています。モバイルネットワークインフラと車載電子機器の継続的な進歩により、車内接続は複数のユーザーを同時にサポートする高速・低遅延サービスへと変貌を遂げました。高度なデータ処理、クラウド統合、インテリジェントなネットワーク管理により信頼性が向上し、データ保護が強化されています。車両がソフトウェア主導型になるにつれ、車載Wi-Fiは通信、システム監視、リモート更新を支える中核プラットフォームへと進化し、現代の自動車設計における基幹要素としての役割を強化しています。市場成長は、拡大するコネクテッドモビリティエコシステムと先進車両技術の統合進展によりさらに後押しされています。共有モビリティモデルや次世代車両の普及拡大は、常時接続の必要性を高めています。車載Wi-Fiはリアルタイムデータ交換を可能にし、ナビゲーション精度、車両監視、乗客サービス、緊急対応能力を向上させ、個人輸送からフリートベース輸送まで、安全性と効率性の両方を支えます。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 197億米ドル |

| 予測金額 | 477億米ドル |

| CAGR | 9.6% |

ハードウェアセグメントは2025年に67%のシェアを占め、2026年から2035年にかけてCAGR9.9%で成長すると予測されています。この優位性は、車両生産時に組み込まれる内蔵型接続コンポーネントに対する強い需要を反映しています。高度な通信モジュールやネットワーク機器の普及が進んだことで、ハードウェアは車載Wi-Fiシステムの基盤となり、安定した接続性、高速データ転送、複数の接続ユーザーへの対応を実現しています。

4G LTEセグメントは2025年に56%のシェアを占め、2035年までCAGR 9.2%で成長すると予測されています。その主導的地位は、広範なネットワーク可用性、実績ある性能、コスト効率によって支えられています。インフラの普及と既存車両システムとの互換性により、この技術は幅広い車種カテゴリーで優先的に選択されています。

米国車載Wi-Fi市場は2025年に87%のシェアを占め、63億米ドルの市場規模を生み出しました。確立された自動車エコシステム、先進的なデジタルインフラ、インテリジェント接続ソリューションの早期導入が地域的な優位性を支え、北米が世界市場で強固な地位を確立する要因となっています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- コネクテッドカーへの需要の高まり

- 4G/5Gネットワークの拡張

- 電気自動車および自動運転車の成長

- フリートおよびモビリティサービスの採用拡大

- 業界の潜在的リスク&課題

- 導入およびサブスクリプション費用の高さ

- サイバーセキュリティとデータプライバシーに関する懸念事項

- 市場機会

- 5G、V2X、スマートモビリティエコシステムとの統合

- デジタルサービスとサブスクリプションによる収益化

- コネクテッドカーおよび自動運転車の導入

- IoTおよびスマートモビリティアプリケーション

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- NAIC車載Wi-Fi規制(米国)

- 米国各州保険局

- OSFI車載Wi-Fiガイドライン(カナダ)

- 欧州

- ドイツ金融監督庁(BaFin)車載Wi-Fi規制

- フランスACPR車載Wi-Fi規制

- 英国金融行動監視機構(PRA)及び金融行動監視機構(FCA)による車載Wi-Fiガイドライン

- イタリアIVASS車載Wi-Fi規格

- アジア太平洋地域

- 中国銀行保険監督管理委員会(CBIRC)車載Wi-Fiに関する規則

- 日本金融庁の車載Wi-Fi規制

- 韓国金融委員会(FSC)及び金融監督院(FSS)車載Wi-Fiガイドライン

- インドIRDAI車載Wi-Fi規格

- ラテンアメリカ

- ブラジルSUSEP車載Wi-Fi規制

- メキシコCNSF車載Wi-Fiガイドライン

- 中東・アフリカ

- アラブ首長国連邦中央銀行車両内Wi-Fiガイドライン

- サウジアラビア中央銀行(SAMA)車載Wi-Fi規制

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの展望

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境的側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例シナリオ

- 商用車向けフリート管理・テレマティクス

- 無線(OTA)アップデートと車両診断

- プレミアム車載インフォテインメント&乗員体験

- 自動運転車およびADASサポート

- 保険・リスク管理

- サイバーセキュリティ、データプライバシー及びコンプライアンスフレームワーク

- サイバーセキュリティアーキテクチャ

- データプライバシーコンプライアンス

- 脅威の現状

- セキュリティ・バイ・デザイン原則

- データガバナンス

- サードパーティリスク管理

- セキュリティインシデント管理

- コンプライアンス成熟度モデル

- 顧客の信頼とブランドへの影響

- Over-the-Air(OTA)アップデート:インフラストラクチャ、展開およびフリート管理

- OTA更新アーキテクチャ

- ゼロタッチプロビジョニング

- ソフトウェア展開戦略

- フリート固有の課題

- 接続性への依存

- 更新頻度とペース

- コスト構造

- コネクテッドサービスの実現

- 予知保全の統合

- OTAによる規制コンプライアンス

- フリート管理プラットフォームの統合

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- ハードウェア

- Wi-Fiルーター

- 組込みモジュール

- OBD-IIデバイス

- アンテナ及び受信機

- ソフトウェア及びサービス

- 接続性管理

- クラウドベースのソリューション

- インフォテインメントアプリケーション

第6章 市場推計・予測:技術別、2022-2035

- 4G LTE

- 5G NR

- Wi-Fi 6

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:流通チャネル別、2022-2035

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Global Player

- AT&T

- Berkshire Hathaway

- Broadcom

- Ericsson

- Harman International

- Munich Re

- NXP Semiconductors

- Qualcomm

- Swiss Re

- Verizon Communications

- Regional Player

- China Re

- Hannover Re

- Lloyd’s

- MTN

- PartnerRe

- Reliance Jio

- SCOR

- SoftBank

- Telefonica

- Telstra

- 新興企業

- Autotalks

- CalAmp

- Cohda Wireless

- Icomera

- Veniam