|

市場調査レポート

商品コード

1708134

MEP(機械・電気・配管)ソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Mechanical, Electrical, and Plumbing (MEP) Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| MEP(機械・電気・配管)ソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月05日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

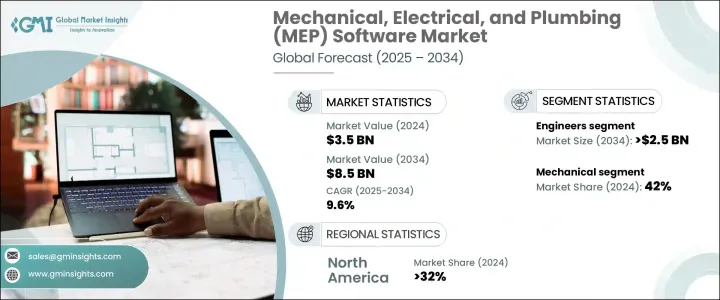

世界のMEP(機械・電気・配管)ソフトウェア市場は2024年に35億米ドルに達し、2025年から2034年にかけてCAGR 9.6%で成長すると予測されています。

同市場は、建設業界における最先端デジタルソリューションの採用拡大が原動力となり、大きく拡大しています。現代の建築物では、機械、電気、配管の各コンポーネント間のシームレスな統合に対する需要が高まっており、MEP(機械・電気・配管)ソフトウェアはエンジニア、請負業者、建築家にとって不可欠なツールとなっています。このソフトウェアは、設計を合理化し、コラボレーションを強化し、潜在的なシステムの競合を着工前に特定することで、プロジェクトのリスクを最小限に抑えます。

ビルディング・インフォメーション・モデリング(BIM)の急速な統合は、主要な成長促進要因です。BIMはデータリッチな3Dモデリングを容易にし、複数の利害関係者がリアルタイムで協力し、建築設計を最適化することを可能にします。エンジニアと請負業者は、非効率の検出、プロジェクト実行の改善、運用コストの削減のために、この技術を活用するようになってきています。デジタル建設手法へのシフトは、インフラ・プロジェクトの複雑性の高まりと相まって、さまざまな用途でMEP(機械・電気・配管)ソフトウェアの普及に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 35億米ドル |

| 予測金額 | 85億米ドル |

| CAGR | 9.6% |

スマートビルディング技術が市場の成長をさらに加速させています。商業ビルや住宅へのIoT、AI、自動化の導入が進み、照明、HVAC、セキュリティなどの重要な機能をサポートする効率的なMEPシステムが求められています。より多くのビルがインテリジェントで相互接続されたシステムに移行するにつれて、エネルギー効率と持続可能性の最適化を保証する高度なMEPソリューションの需要は高まり続けています。世界中の政府や規制機関もエネルギー効率の高い建物設計を推進しており、MEP(機械・電気・配管)ソフトウェア・プロバイダーに有利な機会を生み出しています。

市場はエンドユーザー別に区分され、2024年のシェアはエンジニアが30%を占める。エンジニアは、必要不可欠な建築システムの設計と実装を担当するため、MEP(機械・電気・配管)ソフトウェアの主要な採用者であり続けています。機械、電気、配管コンポーネントを建設プロジェクトに統合する専門知識は、引き続きソフトウェア需要を牽引しており、この分野が市場を独占しています。

用途別では、高度なHVACシステムに対するニーズの高まりにより、機械分野が2024年の市場シェアの42%を占めました。MEP(機械・電気・配管)ソフトウェアは、効率的な暖房、換気、空調ソリューションを設計し、最適な気流分布と室内の快適性を確保する上で極めて重要です。エネルギー効率の高い空調制御システムが重視されるようになり、機械的用途におけるMEPソリューションの需要は引き続き堅調です。

北米は2024年にMEP(機械・電気・配管)ソフトウェア市場の32%を占め、住宅、産業、商業建築の継続的な拡大に支えられています。同地域ではインフラプロジェクトが急増しているため、革新的なMEPソリューションへのニーズが高まっており、重要なビルシステムの精密設計、最適化、管理が可能になっています。同地域では、スマートシティとグリーンビルディングへの注目が高まっており、市場成長の主要な貢献者としての地位がさらに強化されています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ソフトウェアプロバイダー

- テクノロジープロバイダー

- コンサルティングおよび統合サービスプロバイダー

- 最終用途

- 利益率分析

- テクノロジー&イノベーション・情勢

- 特許分析

- 使用事例

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- スマートビルディング技術に対する需要の高まり

- 建設業界のデジタル化

- BIM(ビルディング・インフォメーション・モデリング)の採用増加

- 世界の都市化とインフラ開発

- エネルギー効率と持続可能性の重視

- 業界の潜在的リスク&課題

- 高い初期費用と投資

- ソフトウェア統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソフトウェア別、2021年~2034年

- 主要動向

- BIMベース

- CADベース

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 機械

- 電気

- 配管

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- エンジニア

- 請負業者

- 建築家

- 施設管理者

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- 4MCAD

- ACCA Software

- Access Technology

- Aptus Engineering

- Autodesk

- Bentley Systems

- Cadison

- CYPE

- Design Master Software

- ePROMIS

- eVolve MEP

- Graphisoft

- MagiCAD Group

- Nemetschek Group

- On Center Software

- Procore

- ProgeSOFT

- Renga Software

- SrinSoft

- Trimble

The Global MEP Software Market reached USD 3.5 billion in 2024 and is projected to grow at a CAGR of 9.6% between 2025 and 2034. The market is witnessing significant expansion, driven by the growing adoption of cutting-edge digital solutions in the construction industry. Increasing demand for seamless integration between mechanical, electrical, and plumbing components in modern buildings has made MEP software an essential tool for engineers, contractors, and architects. This software streamlines design, enhances collaboration, and minimizes project risks by identifying potential system conflicts before construction begins.

The rapid integration of Building Information Modeling (BIM) is a key growth driver. BIM facilitates data-rich 3D modeling, enabling multiple stakeholders to collaborate in real time and optimize building design. Engineers and contractors are increasingly leveraging this technology to detect inefficiencies, improve project execution, and reduce operational costs. The shift toward digital construction methodologies, coupled with the rising complexity of infrastructure projects, has fueled the widespread adoption of MEP software across various applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 9.6% |

Smart building technologies are further accelerating market growth. The rising incorporation of IoT, AI, and automation into commercial and residential buildings requires efficient MEP systems to support critical functions such as lighting, HVAC, and security. As more buildings transition to intelligent, interconnected systems, the demand for advanced MEP solutions continues to rise, ensuring optimized energy efficiency and sustainability. Governments and regulatory bodies worldwide are also pushing for energy-efficient building designs, creating lucrative opportunities for MEP software providers.

The market is segmented by end users, with engineers holding a 30% share in 2024. Engineers remain the primary adopters of MEP software due to their role in designing and implementing essential building systems. Their expertise in integrating mechanical, electrical, and plumbing components into construction projects continues to drive software demand, making this segment the dominant force in the market.

By application, the mechanical segment accounted for 42% of the market share in 2024, driven by the increasing need for advanced HVAC systems. MEP software is crucial in designing efficient heating, ventilation, and air conditioning solutions, ensuring optimal airflow distribution and indoor comfort. With the growing emphasis on energy-efficient climate control systems, the demand for MEP solutions in mechanical applications remains strong.

North America accounted for 32% of the MEP Software Market in 2024, supported by ongoing expansion in residential, industrial, and commercial construction. The surge in infrastructure projects across the region has intensified the need for innovative MEP solutions, enabling precise design, optimization, and management of critical building systems. The region's increasing focus on smart cities and green buildings further strengthens its position as a major contributor to market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software providers

- 3.2.2 Technology providers

- 3.2.3 Consulting and integration service providers

- 3.2.4 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for smart building technologies

- 3.9.1.2 Digitalization of the construction industry

- 3.9.1.3 Increased adoption of BIM (building information modeling)

- 3.9.1.4 Global urbanization and infrastructure development

- 3.9.1.5 Focus on energy efficiency and sustainability

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs and investment

- 3.9.2.2 Complexity of software integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Software, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 BIM-based

- 5.3 CAD-based

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Mechanical

- 7.3 Electrical

- 7.4 Plumbing

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Engineers

- 8.3 Contractors

- 8.4 Architects

- 8.5 Facility managers

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 4MCAD

- 10.2 ACCA Software

- 10.3 Access Technology

- 10.4 Aptus Engineering

- 10.5 Autodesk

- 10.6 Bentley Systems

- 10.7 Cadison

- 10.8 CYPE

- 10.9 Design Master Software

- 10.10 ePROMIS

- 10.11 eVolve MEP

- 10.12 Graphisoft

- 10.13 MagiCAD Group

- 10.14 Nemetschek Group

- 10.15 On Center Software

- 10.16 Procore

- 10.17 ProgeSOFT

- 10.18 Renga Software

- 10.19 SrinSoft

- 10.20 Trimble