|

市場調査レポート

商品コード

1708124

自動車用燃料移送ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Fuel Transfer Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用燃料移送ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月03日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

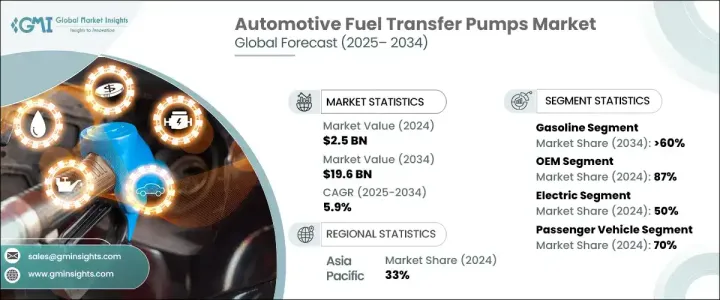

自動車用燃料移送ポンプの世界市場は、2024年には25億米ドルとなり、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

自動車生産台数の増加と燃費効率の高いソリューションに対する需要の高まりによって拡大する世界の自動車産業が、市場を推進しています。高性能車への嗜好が高まる中、メーカーはエンジン効率と耐久性を高める高度な燃料移送ポンプ技術に注力しています。新興経済圏、特にアジアとラテンアメリカでは、急速な都市化、可処分所得の増加、現地での自動車製造を奨励する政府の政策により、自動車販売が急増しています。これは、自動車メーカーが車両効率と規制遵守を重視するため、燃料移送ポンプの採用増加に直接寄与しています。さらに、世界的に厳しい燃費基準への移行が進み、燃料使用を最適化し排出ガスを削減する革新的な燃料移送ソリューションに対する需要が生じています。

自動車用燃料移送ポンプ市場は、ガソリンとディーゼル燃料のカテゴリーに区分されます。2024年の市場シェアはガソリンが60%を占め、乗用車分野での存在感の大きさを反映しています。ガソリン車の普及と燃費向上技術の進歩が、このセグメントの優位性を強めています。消費者は、多くの地域で、特に環境規制が自動車の嗜好に影響する市場では、その低排出ガスと手頃な燃料価格により、ガソリンエンジンを引き続き支持しています。燃費の向上とカーボンフットプリントの削減を目的に設計された次世代ガソリンエンジンの採用が、効率的な燃料移送ポンプの需要をさらに押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 25億米ドル |

| 予測金額 | 196億米ドル |

| CAGR | 5.9% |

自動車用燃料移送ポンプ市場では、相手先商標製品メーカー(OEM)が主導的地位を占めています。自動車メーカーは、その互換性、信頼性、優れた性能により、OEM部品に依存しています。OEMと主要自動車ブランドとの間に確立された関係により、一貫したサプライチェーンが確保され、長期契約が促進され、OEMサプライヤーの優位性が強化されています。OEM製造の燃料移送ポンプに対する信頼は、厳しい業界標準を満たし、最新の自動車に最適な性能を保証する能力に由来します。

アジア太平洋地域の自動車用燃料移送ポンプ市場は、2024年に33%のシェアを占め、自動車生産上位国で需要が急増しました。自動車産業が盛んな国々は、生産台数の増加により市場拡大を牽引しており、燃料移送ポンプの主要消費国であり続けています。国内での自動車製造を促進するための政府のインセンティブが、この地域の成長をさらに加速させています。アジア太平洋全域のインフラ整備は自動車サプライチェーンの効率化を促進し、さまざまな自動車セグメントにおける高度な燃料移送ポンプの需要を支えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 材料プロバイダー

- 製造業者

- 流通業者

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- コスト内訳

- 価格動向

- 規制状況

- 影響要因

- 促進要因

- 軽量で人間工学に基づいた座席への需要の高まり

- 厳しい安全・排ガス規制

- eコマースと物流の成長

- 持続可能な素材の進歩

- 業界の潜在的リスク&課題

- 高度なシーティング技術の高コスト

- サプライチェーンの混乱

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 機械

- 電気

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Airtex Pumps

- Aisin Seiki

- Carter Fuel Systems

- Continental Automotive

- Cummins Fuel

- Delphi Technologies

- Denso Corporation

- Edelbrock Group

- GMB

- Hitachi Astemo

- Holley Performance Products

- Mitsubishi Electric

- Pierburg

- Robert Bosch

- Spectra Premium

- Stanadyne

- TI Fluid Systems

- UFI Filters

- VDO Automotive

- Walbro

The Global Automotive Fuel Transfer Pumps Market was valued at USD 2.5 billion in 2024 and is projected to grow at a CAGR of 5.9% between 2025 and 2034. The expanding global automotive industry, driven by rising vehicle production and increasing demand for fuel-efficient solutions, is propelling the market forward. With the growing preference for high-performance vehicles, manufacturers are focusing on advanced fuel transfer pump technologies that enhance engine efficiency and durability. Emerging economies, particularly in Asia and Latin America, are witnessing a surge in automobile sales due to rapid urbanization, rising disposable incomes, and government policies favoring local vehicle manufacturing. This has directly contributed to the increasing adoption of fuel transfer pumps as automakers emphasize vehicle efficiency and regulatory compliance. Additionally, the shift toward stringent fuel efficiency standards worldwide has created a demand for innovative fuel transfer solutions that optimize fuel usage and reduce emissions.

The automotive fuel transfer pumps market is segmented into gasoline and diesel fuel categories. The gasoline segment accounted for a 60% market share in 2024, reflecting its strong presence in the passenger vehicle sector. The widespread use of gasoline-powered cars, coupled with advancements in fuel efficiency technology, has strengthened the segment's dominance. Consumers continue to favor gasoline engines due to their lower emissions and affordable fuel prices in many regions, particularly in markets where environmental regulations influence vehicle preferences. The adoption of next-generation gasoline engines, designed for improved mileage and reduced carbon footprints, is further driving demand for efficient fuel transfer pumps.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 billion |

| Forecast Value | $19.6 billion |

| CAGR | 5.9% |

Original Equipment Manufacturers (OEMs) hold a leading position in the automotive fuel transfer pumps market. Automakers rely on OEM components due to their compatibility, reliability, and superior performance. Established relationships between OEMs and major automotive brands ensure a consistent supply chain, fostering long-term contracts and reinforcing the dominance of OEM suppliers. The trust in OEM-manufactured fuel transfer pumps stems from their ability to meet stringent industry standards, guaranteeing optimal performance in modern vehicles.

The Asia Pacific automotive fuel transfer pumps market commanded a 33% share in 2024, with demand surging in top vehicle manufacturing nations. Countries with robust automotive industries continue to be major consumers of fuel transfer pumps as increased production volumes drive market expansion. Government-backed incentives to promote domestic vehicle manufacturing further accelerate regional growth. Infrastructure developments across the Asia Pacific are enhancing automotive supply chain efficiency, supporting the demand for advanced fuel transfer pumps across various vehicle segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Cost breakdown

- 3.5 Price trend

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for lightweight and ergonomic seating

- 3.7.1.2 Stringent safety and emission regulations

- 3.7.1.3 Growth in e-commerce and logistics

- 3.7.1.4 Advancements in sustainable materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High cost of advanced seating technologies

- 3.7.2.2 Supply chain disruptions

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Electrical

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airtex Pumps

- 10.2 Aisin Seiki

- 10.3 Carter Fuel Systems

- 10.4 Continental Automotive

- 10.5 Cummins Fuel

- 10.6 Delphi Technologies

- 10.7 Denso Corporation

- 10.8 Edelbrock Group

- 10.9 GMB

- 10.10 Hitachi Astemo

- 10.11 Holley Performance Products

- 10.12 Mitsubishi Electric

- 10.13 Pierburg

- 10.14 Robert Bosch

- 10.15 Spectra Premium

- 10.16 Stanadyne

- 10.17 TI Fluid Systems

- 10.18 UFI Filters

- 10.19 VDO Automotive

- 10.20 Walbro