|

|

市場調査レポート

商品コード

1773264

内視鏡検査の市場機会、成長促進要因、産業動向分析、2025~2034年予測Endoscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 内視鏡検査の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

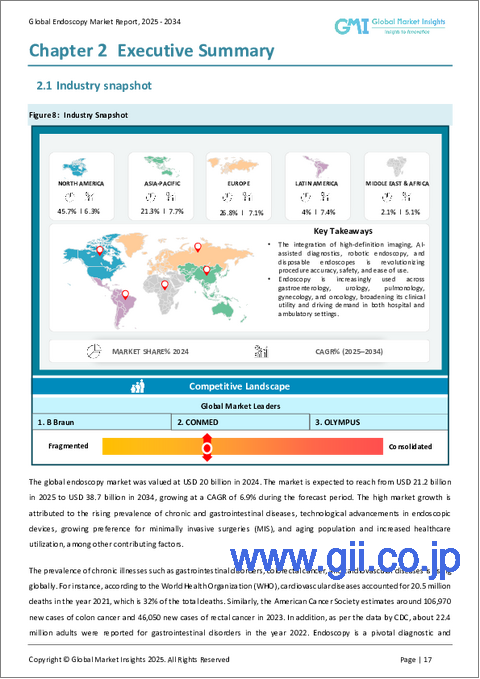

世界の内視鏡検査市場は、2024年には295億米ドルとなり、CAGR 6.9%で成長し、2034年には569億米ドルに達すると予測されています。

市場の成長は、医療の進歩、ヘルスケアの優先事項の変化、世界的な疾病罹患の増加などによって形成されています。侵襲性の低い治療オプションに対する需要の高まりと、診断と治療の両目的での内視鏡検査の利用増加が、市場拡大に大きく寄与しています。ヘルスケア支出の増加、人口の高齢化、慢性疾患や消化器疾患の世界的な罹患率の上昇により、市場は一貫した勢いを見せています。さらに、早期診断へのシフトと予防医療への注目の高まりが、公的・私的ヘルスケア環境での内視鏡処置の採用率上昇につながっています。世界中のヘルスケアシステムは、正確な診断、患者の早期回復、入院コストの削減をサポートする高度な内視鏡技術に投資しています。

2024年には、内視鏡セグメントが最も高い市場シェアを占め、145億米ドルの収益を上げました。高性能な画像診断・処置具の需要は加速し続けており、その原動力となっているのは、視覚的な鮮明さ、操作性の向上、ロボット工学やAIなどのスマート機能の統合です。これらの技術的進歩は、医師が内診を行う方法を変革し、より迅速で正確な診断を可能にしています。コンパクトで、柔軟性があり、軽量な内視鏡は、以前は到達できなかった解剖学的領域に到達できるため、現在では専門医に好まれています。使い勝手の向上、患者の不快感の軽減、優れた臨床結果により、日常診療における内視鏡の位置づけが強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 295億米ドル |

| 予測金額 | 569億米ドル |

| CAGR | 6.9% |

もう一つの要因は、外来患者や外来環境で普及しつつある使い捨て内視鏡器具への嗜好の高まりです。これらの器具は、感染リスクを抑え、複雑な滅菌プロセスを不要にするのに役立ちます。特に使い捨て内視鏡は、そのコスト効率の高さと、患者と医療従事者双方にとっての安全性を向上させる能力から、気管支鏡検査や泌尿器科で支持を集めています。

がん、特に消化器がんと大腸がんの世界的な発症率の増加は、検出、モニタリング、治療のための最前線のソリューションとしての内視鏡処置の必要性を促進しています。内視鏡技術は腫瘍摘出、生検採取、状態追跡に広く使用されています。早期がん診断の利点に対する認識が高まるにつれ、先進的な内視鏡検査ソリューションに対する需要が急増し続けています。

用途別では、腹腔鏡検査は2024年に54億米ドルの市場価値を持ち、2025~2034年にかけてCAGR 6.5%で成長すると予測されています。腹腔鏡検査のような低侵襲技術は、入院期間の短縮、外科的外傷の軽減、回復期間の短縮との関連から、より広く受け入れられています。患者も外科医も、胆嚢摘出から肥満手術に至るまで、こうしたアプローチを好む傾向が明確になってきています。世界の肥満率の上昇に伴い、減量手術の件数も増加しており、腹腔鏡機器の需要をさらに後押ししています。より多くの開業医がシミュレーションプログラムや機器メーカーとの提携を通じて腹腔鏡手術のトレーニングを受けているため、熟練した専門家の利用可能性は向上しており、これが世界規模での採用をさらに後押ししています。

エンドユーザー別では、2024年には病院が圧倒的な地位を占めており、2034年には348億米ドルに達すると予測されています。病院は、診断や外科手術の需要増に対応するため、最先端の内視鏡システムを備えるようになってきています。これらの機関は、特に胃腸やがんのスクリーニングの場合、病気の早期発見のために内視鏡検査の採用を促進する政策的インセンティブや保険適用から利益を得ています。病院は、運営コストを最適化しながら、患者の予後を向上させるために、継続的にインフラをアップグレードしています。長期入院の必要性を減らす内視鏡検査は、この目的に合致しています。スタッフのトレーニングや技術のアップデートに投資することで、病院は内視鏡手技の最新開発に適応しながら、高水準の医療を維持することができます。

米国の内視鏡検査市場は一貫した成長を示しており、2021年の92億米ドルから2024年には104億米ドルに増加しました。2025~2034年までのCAGRは6.1%で成長すると予想されています。慢性疾患の有病率の高さと正確な診断ツールの必要性が、この成長の主な原動力となっています。消化管疾患と診断される患者が増加しており、より高度で侵襲性の低いソリューションの必要性が高まっています。米国市場は、ヘルスケアプロバイダーがコスト効率を維持しながら手技の成果を向上させようとしているため、進化を続けています。

競合情勢は、技術革新、提携、製品の多様化によって定義されます。Stryker Corporation、Olympus Corporation、Boston Scientific、Karl Storz、Medtronicなどの企業が市場シェアの約42~45%を占めています。これらの業界大手は、AI、ロボット工学、高度な画像処理を統合した次世代内視鏡プラットフォームに積極的に投資し、臨床性能を高めています。戦略的提携と買収は、世界的なリーチを広げ、進化する医療機器の展望における地位を強化するための重要な戦術であり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的な高齢化の進展

- 技術的に進歩した内視鏡の導入

- 胃腸障害、がん、その他の慢性疾患の発生率の上昇

- 低侵襲手術の需要増加

- 業界の潜在的リスク・課題

- 新興諸国における熟練した医師と内視鏡医の不足

- 市場機会

- 使い捨て内視鏡の需要増加

- 統合AIとデータ分析の急増

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 償還シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

- バリューチェーン分析

- 将来の市場動向

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 消費者行動分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021~2034年

- 主要動向

- 内視鏡

- 硬性内視鏡

- 軟性内視鏡

- カプセル内視鏡

- 可視化システム

- 超音波内視鏡検査

- 吸入器

- その他

第6章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 腹腔鏡検査

- 消化管内視鏡検査

- 胃内視鏡検査

- 大腸内視鏡検査

- S状結腸鏡検査

- 十二指腸鏡検査

- その他

- 関節鏡検査

- 耳鼻咽喉科内視鏡検査

- 肺内視鏡検査

- 産婦人科

- その他

第7章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- B Braun

- Boston Scientific

- CONMED

- COOK MEDICAL

- FUJIFILM

- HOYA

- INTUITIVE

- Johnson &Johnson

- KARL STORZ

- Medtronic

- OLYMPUS

- RICHARD WOLF

- Smith &Nephew

- Stryker

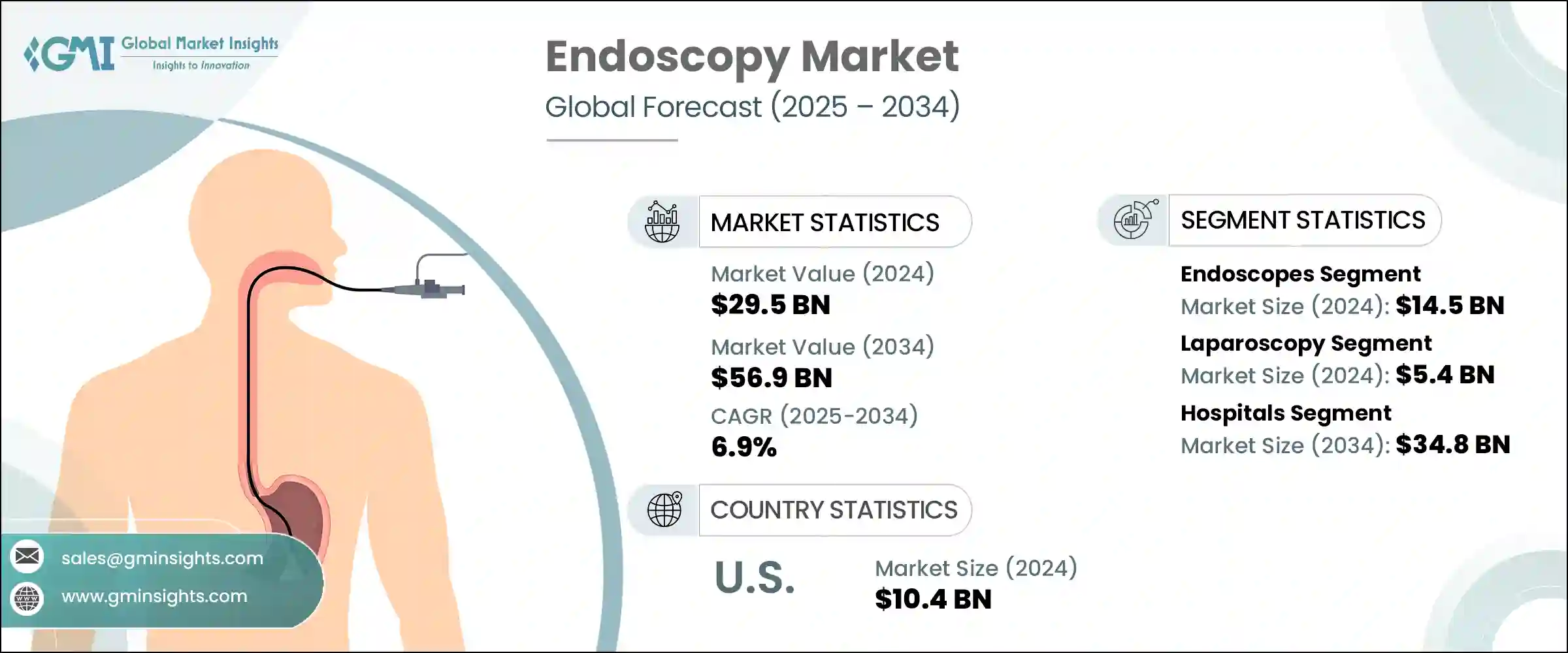

The Global Endoscopy Market was valued at USD 29.5 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 56.9 billion by 2034. Market growth is being shaped by a combination of medical advancements, changing healthcare priorities, and rising disease burdens across the globe. The rising demand for less invasive treatment options and increased utilization of endoscopy for both diagnostic and therapeutic purposes are contributing significantly to market expansion. The market is witnessing consistent momentum due to growing healthcare spending, aging populations, and the rising incidence of chronic and gastrointestinal illnesses worldwide. Moreover, a shift toward early diagnosis and the growing focus on preventive care have led to higher adoption of endoscopic procedures in both public and private healthcare settings. Healthcare systems across the globe are investing in advanced endoscopic technologies that support accurate diagnostics, faster patient recovery, and lower hospitalization costs.

In 2024, the endoscopes segment accounted for the highest market share, generating USD 14.5 billion in revenue. The demand for high-performance imaging and procedural tools continues to accelerate, driven by improvements in visual clarity, maneuverability, and integration of smart features like robotics and AI. These technological advancements are transforming how physicians perform internal examinations, enabling quicker and more precise diagnoses. Compact, flexible, and lightweight endoscopes are now preferred by specialists for reaching anatomical areas that were previously inaccessible. Enhanced usability, reduced patient discomfort, and superior clinical outcomes are strengthening the position of endoscopes in routine practice.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.5 Billion |

| Forecast Value | $56.9 Billion |

| CAGR | 6.9% |

Another contributing factor is the growing preference for single-use and disposable endoscopic tools, which are becoming popular in outpatient and ambulatory settings. These devices help limit the risk of infection and eliminate the need for complex sterilization processes. Single-use endoscopes, in particular, are gaining traction in bronchoscopy and urology due to their cost-efficiency and ability to improve safety for both patients and practitioners.

The rising global burden of cancer, particularly gastrointestinal and colorectal cancers, is driving the need for endoscopic procedures as a frontline solution for detection, monitoring, and treatment. Endoscopic techniques are widely used for tumor removal, biopsy collection, and condition tracking. As awareness about the benefits of early cancer diagnosis grows, the demand for advanced endoscopy solutions continues to surge.

Among the various applications, laparoscopy held a market value of USD 5.4 billion in 2024 and is projected to grow at a CAGR of 6.5% between 2025 and 2034. Minimally invasive techniques like laparoscopy are gaining broader acceptance due to their association with shorter hospital stays, lower surgical trauma, and faster recovery periods. Patients and surgeons alike are showing a clear preference for these approaches in procedures ranging from gallbladder removal to bariatric surgeries. With the increasing rate of obesity worldwide, the number of weight-loss surgeries is rising, further supporting the demand for laparoscopic instruments. As more practitioners receive training in laparoscopy through simulation programs and partnerships with device manufacturers, the availability of skilled professionals is improving, which further drives adoption on a global scale.

In terms of end users, hospitals held the dominant position in 2024 and are projected to reach USD 34.8 billion by 2034. Hospitals are increasingly equipped with state-of-the-art endoscopic systems to meet the rising demand for diagnostics and surgical procedures. These institutions benefit from policy incentives and insurance coverage that promote the adoption of endoscopy for early disease detection, especially in cases of gastrointestinal and cancer screenings. Hospitals are continuously upgrading their infrastructure to enhance patient outcomes while optimizing operational costs. Endoscopy procedures, which reduce the need for extended hospital stays, align well with this objective. Investments in staff training and technology updates ensure that hospitals maintain high standards of care while adapting to the latest developments in endoscopic procedures.

The endoscopy market in the United States has shown consistent growth, rising from USD 9.2 billion in 2021 to USD 10.4 billion in 2024. It is expected to grow at a CAGR of 6.1% from 2025 to 2034. The high prevalence of chronic diseases and the need for precise diagnostic tools are major drivers behind this growth. An increasing number of patients are being diagnosed with gastrointestinal disorders, prompting the need for more advanced and less invasive solutions. The U.S. market continues to evolve as healthcare providers seek to improve procedural outcomes while maintaining cost efficiency.

The competitive landscape is defined by innovation, partnerships, and product diversification. Companies like Stryker Corporation, Olympus Corporation, Boston Scientific, Karl Storz, and Medtronic command approximately 42%-45% of the market share. These industry leaders are actively investing in next-gen endoscopic platforms that integrate AI, robotics, and advanced imaging to elevate clinical performance. Strategic collaborations and acquisitions remain key tactics for broadening global reach and strengthening their position in the evolving medical device landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population globally

- 3.2.1.2 Introduction of technologically advanced endoscopes

- 3.2.1.3 Rising incidences of gastrointestinal disorders, cancer and other chronic conditions

- 3.2.1.4 Increasing demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled physicians and endoscopists in developing countries

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for disposable or single-use endoscopes

- 3.2.3.2 Surge in integrated AI and data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Reimbursement scenario

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Gap analysis

- 3.9 Value chain analysis

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Patent Landscape

- 3.13 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By Region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Endoscopes

- 5.2.1 Rigid endoscopes

- 5.2.2 Flexible endoscopes

- 5.2.3 Capsule endoscopes

- 5.3 Visualization systems

- 5.4 Endoscopic ultrasound

- 5.5 Insufflator

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Laparoscopy

- 6.3 GI endoscopy

- 6.3.1 Gastroscopy

- 6.3.2 Colonoscopy

- 6.3.3 Sigmoidoscopy

- 6.3.4 Duodenoscopy

- 6.3.5 Other GI endoscopies

- 6.4 Arthroscopy

- 6.5 ENT endoscopy

- 6.6 Pulmonary endoscopy

- 6.7 Obstetrics/Gynecology

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Boston Scientific

- 9.3 CONMED

- 9.4 COOK MEDICAL

- 9.5 FUJIFILM

- 9.6 HOYA

- 9.7 INTUITIVE

- 9.8 Johnson & Johnson

- 9.9 KARL STORZ

- 9.10 Medtronic

- 9.11 OLYMPUS

- 9.12 RICHARD WOLF

- 9.13 Smith & Nephew

- 9.14 Stryker