|

市場調査レポート

商品コード

1699411

キッチン家電市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Kitchen Appliances Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| キッチン家電市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

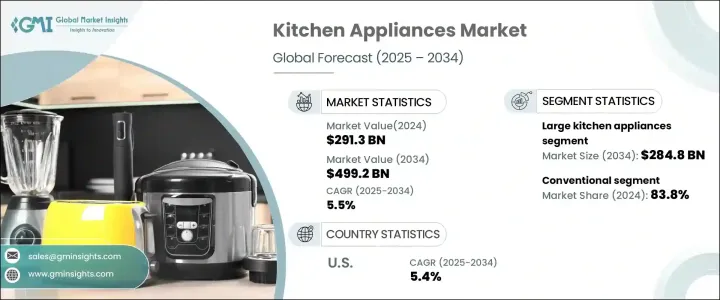

世界のキッチン家電市場は2024年に2,913億米ドルに達し、2025年から2034年にかけてCAGR 5.5%で成長すると予測されています。

より効率的で、技術的に高度で、使い勝手の良い家電製品に対する需要の急増が、この成長を後押ししています。消費者はキッチンでの利便性、スピード、優れた性能をますます求めるようになっており、これがよりスマートで接続性の高いソリューションへのシフトに拍車をかけています。大型家電と小型家電の両方における技術革新は、家庭の機能を一変させ、増大する持続可能性の動向に沿ったエネルギー効率の高い直感的な選択肢を提供しています。環境問題に対する意識が高まるにつれ、消費者は電力消費を抑え、二酸化炭素排出量を削減するエネルギー効率の高い製品への投資を意識的に選択するようになっています。さらに、中間所得層の拡大、可処分所得の増加、新興経済諸国における急速な都市化が、最新型キッチン機器の採用拡大に寄与しています。これらの要因は、現在進行中の技術的進歩と相まって、厨房機器市場を世界経済の主要プレーヤーにしています。

市場は大型キッチン家電と小型キッチン家電に区分され、大型キッチン家電品セグメントは2024年に1,557億米ドルを生み出し、2034年には2,848億米ドルに達すると予想されます。冷蔵庫、オーブン、食器洗い機を含む大型キッチン家電は、耐久性と高度な機能性を提供する必要不可欠な長期投資と考えられています。消費者は、利便性を高め、調理効率を向上させ、エネルギー消費を削減できるこれらの高額商品を優先的に購入します。最近の大型家電には、スマートセンサー、タッチコントロール、省エネ技術などの機能が組み込まれており、性能と持続可能性を求める技術に精通した購買層にアピールしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2,913億米ドル |

| 予測金額 | 4,992億米ドル |

| CAGR | 5.5% |

キッチン家電も従来型とスマート型に分類されます。2024年には従来型家電が83.8%のシェアを占め、2034年まで5.2%の安定した成長が見込まれます。スマートキッチン技術への関心が高まっているにもかかわらず、コンロ、オーブン、従来型冷蔵庫などの従来型家電は、その信頼性、実証済みの性能、使いやすさから、依然として広く普及しています。これらの電化製品は、特に使い慣れた、時間の経過したソリューションを好む消費者の間で、強い魅力を保持し続けています。メーカー各社は、従来の設計にスマート機能を統合し、高度な機能と従来モデルの信頼性を組み合わせたハイブリッド・オプションを提供しています。

米国のキッチン家電市場は、全体的なユーザー体験を向上させるスマート技術の採用拡大により、年率5.4%で拡大しています。消費者が利便性と時間節約機能を求める中、メーカーは調理、掃除、食品保存を合理化するイノベーションで対応しています。音声制御、遠隔監視、AIベースの機能性の統合は、キッチン家電の未来を再形成し、より直感的でユーザーの好みに反応するものにしています。消費者の嗜好が変化し、スマートで持続可能なソリューションが重視されるようになったことで、厨房機器市場は今後10年間で大きく成長する見通しです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- 小売業者

- 影響要因

- 促進要因

- 可処分所得の増加

- 家電製品の技術進歩

- 消費者のライフスタイルの変化

- 業界の潜在的リスク&課題

- 景気低迷

- 競争の激しい市場

- 促進要因

- 消費者の購買行動分析

- 人口動向

- 購買決定に影響を与える要因

- 消費者の製品採用

- 好みの流通チャネル

- 希望価格帯

- 成長可能性分析

- 規制状況

- 価格分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 大型キッチン家電

- 調理家電

- 冷蔵庫

- 食器洗い機

- オーブンレンジ

- その他(レンジフードなど)

- 小型キッチン家電

- コーヒーメーカー

- ミキサー

- フードプロセッサー

- トースター

- ジューサー

- 電気ケトル

- 電気フライヤー

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- スマート

- 従来型

第7章 市場推計・予測:価格別、2021年~2034年

- 主要動向

- 低価格

- 中価格

- 高価格

第8章 市場推計・予測:設置別、2021年~2034年

- 主要動向

- 屋内

- 屋外

第9章 市場推計・予測:最終用途別2021年~2034年

- 主要動向

- 住宅

- 商業施設

- レストラン

- ホテル

- カフェテリア

- ケータリングサービス

- 小売

- その他(施設厨房など)

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- eコマースサイト

- 企業ウェブサイト

- オフライン

- 専門店

- 個人商店

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- BSH Home Appliances Group

- Electrolux AB

- Groupe SEB

- Haier Group Corporation

- HISENSE Group

- Hitachi Appliances Inc.

- LG Electronics

- Midea Group Co., Ltd.

- Panasonic Corporation

- Robert Bosch Gmbh

- Samsung electronics

- Sharp Corporation

- Toshiba Corporation

- Voltas

- Whirlpool corporation

The Global Kitchen Appliances Market reached USD 291.3 billion in 2024 and is projected to grow at a CAGR of 5.5% between 2025 and 2034. The surge in demand for more efficient, technologically advanced, and user-friendly appliances is driving this growth. Consumers are increasingly seeking convenience, speed, and superior performance in the kitchen, which has fueled the shift toward smarter, more connected solutions. Innovations in both large and small appliances are transforming the way households function, providing energy-efficient and intuitive options that align with growing sustainability trends. As awareness around environmental concerns increases, consumers are making conscious choices to invest in energy-efficient products that reduce electricity consumption and lower carbon footprints. Furthermore, the expanding middle-class population, rising disposable incomes, and rapid urbanization across developing economies are contributing to the increased adoption of modern kitchen appliances. These factors, combined with ongoing technological advancements, are making the kitchen appliances market a key player in the global economy.

The market is segmented into large and small kitchen appliances, with the large appliances segment generating USD 155.7 billion in 2024 and expected to reach USD 284.8 billion by 2034. Large kitchen appliances, including refrigerators, ovens, and dishwashers, are considered essential, long-term investments that offer durability and advanced functionality. Consumers prioritize these high-ticket items due to their ability to enhance convenience, improve cooking efficiency, and reduce energy consumption. Modern large appliances incorporate features such as smart sensors, touch controls, and energy-saving technologies that appeal to tech-savvy buyers seeking performance and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $291.3 Billion |

| Forecast Value | $499.2 Billion |

| CAGR | 5.5% |

Kitchen appliances are also categorized into conventional and smart segments. In 2024, conventional appliances dominated the market with an 83.8% share and are expected to grow at a steady rate of 5.2% through 2034. Despite the rising interest in smart kitchen technology, conventional appliances such as stoves, ovens, and traditional refrigerators remain widely popular due to their reliability, proven performance, and ease of use. These appliances continue to hold strong appeal, especially among consumers who prefer familiar, time-tested solutions. Manufacturers are integrating smart capabilities into conventional designs, offering hybrid options that combine advanced functionality with the reliability of traditional models.

The US kitchen appliances market is expanding at an annual rate of 5.4%, driven by the growing adoption of smart technologies that enhance the overall user experience. As consumers seek convenience and time-saving features, manufacturers are responding with innovations that streamline cooking, cleaning, and food storage. The integration of voice control, remote monitoring, and AI-based functionalities is reshaping the future of kitchen appliances, making them more intuitive and responsive to user preferences. With changing consumer preferences and an increasing emphasis on smart, sustainable solutions, the kitchen appliances market is poised for significant growth over the next decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.5 Secondary

- 1.5.1.1 Paid sources

- 1.5.1.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising disposable income

- 3.2.1.2 Technological advancement in appliances

- 3.2.1.3 Changing consumers lifestyles

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Economic downturn

- 3.2.2.2 Highly competitive market

- 3.2.1 Growth drivers

- 3.3 Consumer buying behavior analysis

- 3.3.1 Demographic trends

- 3.3.2 Factors Affecting Buying Decision

- 3.3.3 Consumer Product Adoption

- 3.3.4 Preferred Distribution Channel

- 3.3.5 Preferred Price Range

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Large kitchen appliances

- 5.2.1 Cooking appliances

- 5.2.2 Refrigerator

- 5.2.3 Dishwasher

- 5.2.4 Ovens

- 5.2.5 Others (Range hood, etc.)

- 5.3 Small kitchen appliances

- 5.3.1 Coffee makers

- 5.3.2 Blenders

- 5.3.3 Food processors

- 5.3.4 Toasters

- 5.3.5 Juicers

- 5.3.6 Electric kettles

- 5.3.7 Electric deep fryers

- 5.3.8 Others

Chapter 6 Market Estimates & Forecast, By Type, 2021 – 2034, (USD Billion) (Million units)

- 6.1 Key trends

- 6.2 Smart

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Price, 2021 – 2034, (USD Billion) (Million units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Installation 2021 – 2034, (USD Billion) (Million units)

- 8.1 Key trends

- 8.2 Indoor

- 8.3 Outdoor

Chapter 9 Market Estimates & Forecast, By End Use 2021 – 2034, (USD Billion) (Million units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Restaurants

- 9.3.2 Hotels

- 9.3.3 Cafeterias

- 9.3.4 Catering services

- 9.3.5 Retail

- 9.3.6 Others (Institutional kitchens, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution channel, 2021 – 2034, (USD Billion) (Million units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce Site

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Individual stores

- 10.3.3 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 12.1 BSH Home Appliances Group

- 12.2 Electrolux AB

- 12.3 Groupe SEB

- 12.4 Haier Group Corporation

- 12.5 HISENSE Group

- 12.6 Hitachi Appliances Inc.

- 12.7 LG Electronics

- 12.8 Midea Group Co., Ltd.

- 12.9 Panasonic Corporation

- 12.10 Robert Bosch Gmbh

- 12.11 Samsung electronics

- 12.12 Sharp Corporation

- 12.13 Toshiba Corporation

- 12.14 Voltas

- 12.15 Whirlpool corporation