|

市場調査レポート

商品コード

1699380

ガス遮断器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Gas Circuit Breaker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ガス遮断器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 131 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

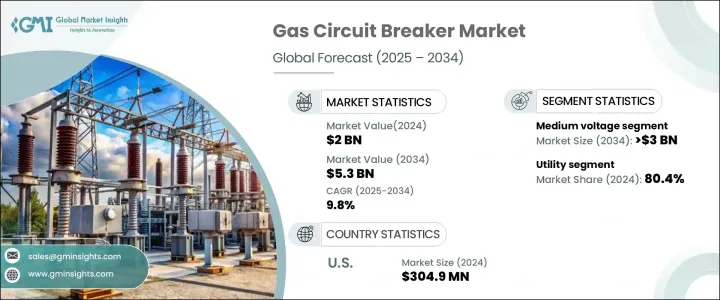

世界のガス遮断器市場は2024年に20億米ドルと評価され、2025年から2034年にかけてCAGR 9.8%で拡大すると予想されています。

ガス遮断器は、六フッ化硫黄などのガスを利用して電気アークを消火し、電流の流れを遮断することで、現代の電力システムにおいて重要な役割を果たしています。これらのシステムは、送電網の安定性を確保し、過負荷から送電網を保護し、全体的な運用効率を高める上で不可欠です。信頼性が高く効率的な電力インフラに対する需要の高まりは、送電網近代化への継続的な投資と相まって、市場の成長を大きく後押ししています。

世界の電力網の老朽化により、政府や民間企業は送電網のアップグレードに多額の投資を行うようになり、ガス遮断器の採用を後押ししています。再生可能エネルギー源の統合、スマートグリッドの拡大、電気自動車の普及が、高度な回路保護ソリューションの必要性を高めています。これらの要因によって、配電ネットワークにおいてガス・サーキット・ブレーカが不可欠なコンポーネントになりつつあります。さらに、電力損失の削減とエネルギー効率の向上を目的とした政府の厳しい規制が、業界の拡大に拍車をかけています。絶縁技術の進歩と、従来の絶縁ガスに代わる環境に優しい代替品へのシフトの高まりも、市場の軌道を形成しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 20億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 9.8% |

市場は電圧別に中電圧と高電圧に区分されます。中電圧セグメントは、配電網や産業用アプリケーションで広く採用されていることから、2034年までに30億米ドルに達すると予測されています。中電圧ガス遮断器は、シンプルな設計、迅速なエラー検出、高い故障隔離効率で支持されています。電気自動車の充電インフラ、地下鉄網、産業用オートメーション・システムの普及が進むにつれ、信頼性の高い保護ソリューションに対する需要が急増し続けています。分散型発電ネットワークにおける安定したエネルギー伝送を保証する能力により、さまざまな用途で選ばれています。

最終用途別では、産業部門と公益事業部門に分けられます。ユーティリティ部門は、積極的な送電網近代化の取り組みに支えられ、2024年のシェア80.4%で市場を独占しています。世界各国の政府はエネルギー効率を高めるための奨励プログラムを実施しており、公益事業用途でのガス遮断器の展開をさらに加速させています。エネルギー消費の増加と送電障害の頻発により、電力途絶を防ぐための高度な保護システムの使用が必要になっています。送電網が複雑化するにつれて、故障を隔離してシームレスなエネルギーフローを維持するための堅牢なサーキットブレーカの必要性がますます高まっています。

北米のガス遮断器市場は、有利な政府政策、スマートグリッドインフラへの投資、電気自動車の普及拡大が原動力となり、2024年に3億490万米ドルを創出しました。EV充電ステーションの急速な展開により、安定した配電を確保し、システムの混乱を緩和するための高度な回路保護ソリューションに対する需要が高まっています。さらに、再生可能エネルギー・プロジェクトと持続可能性への取り組みへの注目の高まりが、この地域全体の市場見通しをさらに押し上げています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 中電圧

- 高電圧

第6章 市場規模・予測:設置別、2021年~2034年

- 主要動向

- 屋内

- 屋外

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 配電

- 送電

第8章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 産業

- ユーティリティ

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- ABB

- Al-Amin Enterprises

- Casey Equipment Corporation

- Crompton Greaves

- DILO Company

- GE

- Hitachi

- Megger

- MEIDENSHA CORPORATION

- Mitsubishi Electric Corporation

- Pfiffner Group

- Rockwill

- Schneider Electric

- Siemens Energy

- Toshiba International Corporation

- Wenzhou Wolun Electric Technology

- Zhejiang Volcano Electrical Technology

The Global Gas Circuit Breaker Market was valued at USD 2 billion in 2024 and is expected to expand at a CAGR of 9.8% from 2025 to 2034. Gas circuit breakers play a crucial role in modern electrical power systems by utilizing gases such as sulfur hexafluoride to extinguish electrical arcs and interrupt current flow. These systems are indispensable in ensuring grid stability, protecting electrical networks from overloads, and enhancing overall operational efficiency. The increasing demand for reliable and efficient power infrastructure, coupled with ongoing investments in grid modernization, is significantly propelling market growth.

Aging electrical networks worldwide are pushing governments and private entities to invest heavily in grid upgrades, driving the adoption of gas circuit breakers. The integration of renewable energy sources, the expansion of smart grids, and the growing prevalence of electric vehicles are amplifying the need for advanced circuit protection solutions. These factors are fostering an environment where gas circuit breakers are becoming essential components in electrical distribution networks. Furthermore, stringent government regulations aimed at reducing power losses and enhancing energy efficiency are fueling industry expansion. Advancements in insulation technology and the rising shift toward eco-friendly alternatives to traditional insulating gases are also shaping the market's trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 9.8% |

The market is segmented by voltage into medium and high-voltage categories. The medium-voltage segment is projected to reach USD 3 billion by 2034, driven by its widespread adoption in distribution networks and industrial applications. Medium-voltage gas circuit breakers are favored for their simple design, quick error detection, and high efficiency in fault isolation. With increasing penetration of electric vehicle charging infrastructure, metro rail networks, and industrial automation systems, the demand for reliable protection solutions continues to surge. Their ability to ensure stable energy transmission in distributed generation networks makes them a preferred choice for various applications.

By end use, the industry is divided into industrial and utility sectors. The utility segment dominated the market with an 80.4% share in 2024, supported by aggressive grid modernization efforts. Governments worldwide are implementing incentive programs to enhance energy efficiency, further accelerating the deployment of gas circuit breakers in utility applications. Rising energy consumption and the frequent occurrence of transmission faults necessitate the use of advanced protection systems to prevent power disruptions. As power grids become more complex, the need for robust circuit breakers to isolate faults and maintain seamless energy flow is becoming increasingly critical.

North America Gas Circuit Breaker Market generated USD 304.9 million in 2024, driven by favorable government policies, investments in smart grid infrastructure, and expanding electric vehicle adoption. The rapid deployment of EV charging stations is amplifying the demand for advanced circuit protection solutions to ensure stable power distribution and mitigate system disruptions. Additionally, increased focus on renewable energy projects and sustainability initiatives is further boosting market prospects across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 – 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Medium

- 5.3 High

Chapter 6 Market Size and Forecast, By Installation, 2021 – 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Indoor

- 6.3 Outdoor

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Power distribution

- 7.3 Power transmission

Chapter 8 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Utility

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & ‘000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Russia

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Turkey

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Al-Amin Enterprises

- 10.3 Casey Equipment Corporation

- 10.4 Crompton Greaves

- 10.5 DILO Company

- 10.6 GE

- 10.7 Hitachi

- 10.8 Megger

- 10.9 MEIDENSHA CORPORATION

- 10.10 Mitsubishi Electric Corporation

- 10.11 Pfiffner Group

- 10.12 Rockwill

- 10.13 Schneider Electric

- 10.14 Siemens Energy

- 10.15 Toshiba International Corporation

- 10.16 Wenzhou Wolun Electric Technology

- 10.17 Zhejiang Volcano Electrical Technology