|

市場調査レポート

商品コード

1699379

軟部組織修復市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Soft Tissue Repair Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 軟部組織修復市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

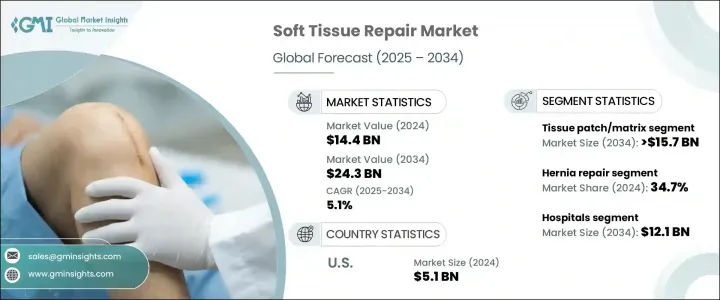

世界の軟部組織修復市場は、2024年に144億米ドルに達し、2025年から2034年にかけてCAGR 5.1%で拡大すると予測されています。

スポーツ外傷、外傷症例の増加、加齢に伴う軟部組織の損傷が、外科的ソリューションの需要を促進しています。高齢者人口の増加と肥満率の増加は、ヘルニアや軟部組織の修復を必要とするその他の疾患の発生率の上昇に寄与しています。生体適合製品や合成メッシュ・ソリューションの進歩により、患者の転帰が改善され、外科的介入がより効果的になっています。画像診断技術や低侵襲手術の進歩は、回復時間を延ばし、術後の合併症を減少させています。

革新的な修復技術に対する認識が高まり、患者の転帰が改善されたことが市場成長の燃料となっています。スポーツ医学の拡大と青少年のスポーツ参加の増加は、傷害率の上昇をもたらし、需要をさらに促進します。さらに、新興市場におけるヘルスケアへの政府投資が新たな成長機会を生み出しています。多血小板血漿(PRP)療法や幹細胞治療を含む再生医療の今後の開発は、この分野に革命をもたらすと期待されています。複雑な手術に対するヘルスケア支出と保険適用の増加により、高度な修復方法へのアクセスが向上します。外来手術センターにおける外来患者向けサービスへのシフトは、費用対効果が高く利便性の高い治療の動向を浮き彫りにし、市場拡大を後押しします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 144億米ドル |

| 予測金額 | 243億米ドル |

| CAGR | 5.1% |

軟部組織の修復には、筋肉の修復、筋膜の縫合、靭帯、腱、皮膚組織の損傷の治療が含まれます。これには、疼痛緩和や動作回復を目的とした非外科的縫合、生物学的ソリューション、再生幹細胞治療などの周術期および術後介入が含まれます。市場は組織パッチ/マトリックスと組織固定器具に分けられます。組織パッチ/マトリックス分野は、手術における効果的な足場ソリューションの必要性によって牽引され、CAGR 4.9%で成長し、2034年には157億米ドル以上に達すると予想されています。外傷、ヘルニア、加齢に伴う組織変性などの症例の増加が需要を押し上げています。材料科学の進歩、特に生体工学や合成パッチは、優れた生体適合性と低い拒絶反応リスクにより、患者の転帰を向上させる。

腹腔鏡手術のような最新の外科技術は、合併症や回復期間を短縮することで組織パッチの採用をサポートしています。スポーツ傷害の発生率の上昇と高齢化人口の増加により、効率的な組織修復ソリューションがさらに必要とされています。生来の組織とシームレスに統合する生物工学的足場を含む再生医療における革新は、その用途を拡大しています。ヘルスケアへの投資が増加し、外科手術に対する保険適用が改善されたことで、高度な組織修復ソリューションの普及が促進されます。外来手術センターにおける外来手術への注目は、費用対効果が高く回復の早い材料への需要を加速させ、組織マトリックスとパッチを外科医の間で好ましい選択肢として位置づけています。

市場は用途別にヘルニア修復、整形外科手術、皮膚修復、硬膜修復、その他の治療に区分されます。ヘルニア修復は2024年に市場の34.7%を占めたが、これは肥満率の上昇、高齢化、座りがちなライフスタイルなどが背景にあります。腹腔鏡手術や開腹手術の採用が増加し、再発を減らし回復時間を改善する合成繊維や生物学的メッシュを含む高度な修復材料への需要が高まっています。ヘルニア修復ソリューションに対する患者や外科医の信頼性の向上が、引き続き市場拡大の原動力となっています。

用途別セグメントには、病院、外来手術センター、診療所が含まれます。2024年には病院が市場をリードし、48.3%のシェアを占め、2034年には121億米ドルに達すると予測されています。複雑な手術症例の多さ、高度な医療インフラ、専門的な術後ケアにより、病院が主要な治療センターとなっています。高齢化や生活習慣病による手術件数の増加が、軟部組織修復における病院の優位性をさらに強めています。

米国の軟部組織修復市場は、2023年には47億米ドル、2024年には51億米ドルと評価され、力強い成長が予測されています。慢性疾患、スポーツ外傷、加齢に伴う組織変性などの増加により、高度な修復ソリューションへの需要が高まっています。生物学的製剤や合成メッシュの採用拡大が治療効果を高めています。回復時間を短縮し合併症を減らす低侵襲の腹腔鏡技術が人気を集めています。好意的な償還政策と高いヘルスケア支出により、革新的な修復法を患者がより多く利用できるようになっています。新興国市場には大手メーカーが存在するため、継続的な製品開発が行われ、市場開拓が強化されています。外来手術センターへのシフトと高度な病院インフラが、より広範な普及を支えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 肥満人口の増加

- スポーツ傷害の増加

- 軟部組織修復手技の最近の進歩

- 整形外科疾患の有病率の増加

- 業界の潜在的リスク&課題

- 軟部組織修復手技の過剰なコスト

- 厳しい規制の枠組み

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 組織パッチ/マトリックス

- 合成メッシュ

- 生物学的メッシュ

- 同種移植片

- 異種移植片

- 組織固定器具

- 縫合糸アンカー

- 縫合糸

- 干渉スクリュー

- その他の組織固定器具

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ヘルニア修復

- 整形外科

- 皮膚修復

- 硬膜修復

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 診療所

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Anika Therapeutics

- Arthrex

- Baxter

- Becton, Dickinson and Company

- Collagen Matrix

- CONMED

- CryoLife

- Depuy Synthes(Johnson &Johnson)

- Integra LifeSciences

- Medprin

- Medtronic

- Smith &Nephew

- Stryker Corporation

- Zimmer Biomet

The Global Soft Tissue Repair Market reached USD 14.4 billion in 2024 and is projected to expand at a CAGR of 5.1% from 2025 to 2034. Rising sports injuries, trauma cases, and age-related soft tissue damage are driving demand for surgical solutions. A growing elderly population and increasing obesity rates contribute to higher incidences of hernias and other conditions requiring soft tissue repair. Advances in biocompatible products and synthetic mesh solutions are improving patient outcomes, making surgical interventions more effective. Progress in imaging techniques and minimally invasive procedures enhances recovery times and reduces post-operative complications.

Greater awareness of innovative repair techniques and improved patient outcomes fuel market growth. The expansion of sports medicine and increased youth participation in sports result in higher injury rates, further driving demand. Additionally, government investments in healthcare in emerging markets are creating new growth opportunities. Future developments in regenerative medicine, including platelet-rich plasma (PRP) therapy and stem cell treatments, are expected to revolutionize the field. Increased healthcare spending and insurance coverage for complex surgeries improve access to advanced repair methods. A shift towards outpatient services in ambulatory surgical centers highlights the trend of cost-effective, convenient care, reinforcing market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $24.3 Billion |

| CAGR | 5.1% |

Soft tissue repair encompasses muscle restoration, fascia suturing, and treatment of ligaments, tendons, and skin tissue damage. This includes perioperative and post-operative interventions such as non-surgical sutures, biological solutions, and regenerative stem cell therapies aimed at pain relief and motion recovery. The market is divided into tissue patch/matrix and tissue fixation devices. The tissue patch/matrix segment, driven by the need for effective scaffolding solutions in surgeries, is expected to grow at a CAGR of 4.9%, reaching over USD 15.7 billion by 2034. Increased cases of traumatic injuries, hernias, and age-related tissue degeneration are boosting demand. Advances in materials science, particularly bioengineered and synthetic patches, enhance patient outcomes due to superior biocompatibility and lower rejection risks.

Modern surgical techniques, such as laparoscopic procedures, support the adoption of tissue patches by reducing complications and recovery periods. The rising incidence of sports injuries and a growing aging population further necessitate efficient tissue repair solutions. Innovations in regenerative medicine, including bioengineered scaffolds that integrate seamlessly with native tissues, expand their applications. Increased healthcare investments and improved insurance coverage for surgical procedures facilitate wider adoption of advanced tissue repair solutions. The focus on outpatient procedures in ambulatory surgical centers accelerates the demand for cost-effective and rapid recovery materials, positioning tissue matrices and patches as preferred options among surgeons.

The market is segmented by application into hernia repair, orthopedic procedures, skin repair, dural repair, and other treatments. Hernia repair accounted for 34.7% of the market in 2024, driven by rising obesity rates, an aging population, and sedentary lifestyles. Increased adoption of laparoscopic and open surgical procedures boosts demand for advanced repair materials, including synthetic and biological meshes that reduce recurrence and improve recovery times. Enhanced patient and surgeon confidence in hernia repair solutions continues to drive market expansion.

End-use segmentation includes hospitals, ambulatory surgical centers, and clinics. Hospitals led the market in 2024, holding a 48.3% share and projected to reach USD 12.1 billion by 2034. The high volume of complex surgical cases, advanced medical infrastructure, and specialized post-operative care make hospitals the primary treatment centers. Rising surgical volumes due to aging populations and lifestyle-related conditions further reinforce hospital dominance in soft tissue repair.

The U.S. soft tissue repair market was valued at USD 4.7 billion in 2023 and USD 5.1 billion in 2024, with strong growth projections. Increased cases of chronic diseases, sports injuries, and age-related tissue degeneration drive demand for advanced repair solutions. The growing adoption of biologics and synthetic meshes enhances the effectiveness of treatments. Minimally invasive laparoscopic techniques, which shorten recovery times and reduce complications, are gaining traction. Favorable reimbursement policies and high healthcare spending enable greater patient access to innovative repair methods. The presence of leading manufacturers fosters continuous product development, strengthening market growth. The shift toward outpatient surgical centers and advanced hospital infrastructure supports broader ado

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising obese population

- 3.2.1.2 Increasing incidence of sports injuries

- 3.2.1.3 Recent advancements in soft tissue repair procedures

- 3.2.1.4 Increasing prevalence of orthopedic conditions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Excessive cost of soft tissue repair procedures

- 3.2.2.2 Stringent regulatory framework

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tissue patch/Matrix

- 5.2.1 Synthetic mesh

- 5.2.2 Biologic mesh

- 5.2.2.1 Allograft

- 5.2.2.2 Xenograft

- 5.3 Tissue fixation devices

- 5.3.1 Suture anchors

- 5.3.2 Sutures

- 5.3.3 Interference screws

- 5.3.4 Other tissue fixation devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hernia repair

- 6.3 Orthopedic

- 6.4 Skin repair

- 6.5 Dural repair

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anika Therapeutics

- 9.2 Arthrex

- 9.3 Baxter

- 9.4 Becton, Dickinson and Company

- 9.5 Collagen Matrix

- 9.6 CONMED

- 9.7 CryoLife

- 9.8 Depuy Synthes (Johnson & Johnson)

- 9.9 Integra LifeSciences

- 9.10 Medprin

- 9.11 Medtronic

- 9.12 Smith & Nephew

- 9.13 Stryker Corporation

- 9.14 Zimmer Biomet