|

市場調査レポート

商品コード

1699373

建設用予備発電機セット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Standby Construction Generator Sets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 建設用予備発電機セット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月25日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

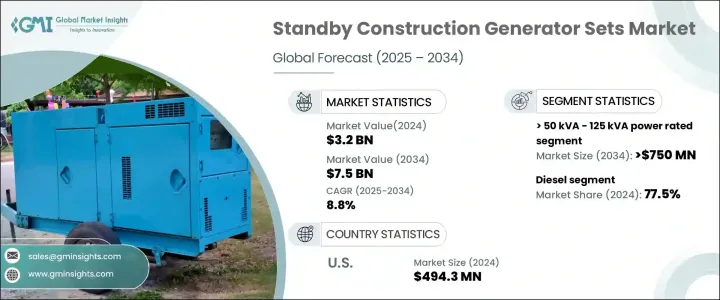

建設用予備発電機セットの世界市場は、2024年に32億米ドルと評価され、2025年から2034年にかけてCAGR 8.8%で成長すると予測されています。

この急拡大の背景には、インフラ開発の加速、都市化、待機発電機システムへの人工知能(AI)および自動化技術の統合の増加があります。建設プロジェクトが複雑化し、電力の信頼性が最優先事項であり続ける中、高度な発電機ソリューションへの需要が高まっています。建設業界では、特に新興経済諸国において新規開発が急増しており、電化の課題により信頼性の高いバックアップ電源が必要とされています。発電機のニーズは、極端な気象条件、送電網の不安定性、さまざまな地域での停電の増加によってさらに高まっています。さらに、再生可能エネルギー発電とハイブリッド電源ソリューションへの投資が市場動向に影響を与えており、メーカー各社はよりクリーンで効率的な予備発電機モデルの技術革新を推進しています。

二酸化炭素排出量の削減を目的とした環境規制の強化は、低排出発電機技術の採用を加速させています。自動負荷管理やスマート燃料最適化などの機能が人気を集めており、企業は厳しい持続可能性基準を満たしながら燃料効率を向上させることができます。世界各国の政府が建設活動からの排出を抑制する政策を実施する中、企業はコンプライアンスに準拠した高効率のバックアップ電源ソリューションに積極的に投資しています。さらに、運用コストへの懸念の高まりが、出力を犠牲にすることなく燃料消費を削減する、よりスマートな発電機システムへのシフトを後押ししています。従来の燃料源をバッテリー貯蔵や再生可能エネルギーと組み合わせたハイブリッド発電システムの革新は、持続可能性の目標に応えて勢いを増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 32億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 8.8% |

定格出力50kVA未満のセグメントは、2034年までのCAGRが9%と予測され、大幅な成長が見込まれています。この成長は、中小規模の建設プロジェクトに対応するコンパクトで燃料効率の高い発電機への好みが高まっていることに起因しています。これらの発電機は、信頼性の高い電力を低運用コストで供給できることから人気を集めており、費用対効果と効率性を重視する建設業者にとって魅力的な選択肢となっています。小規模な建設プロジェクト、遠隔地、緊急時のバックアップ要件が、こうしたポータブルでスケーラブルな電源ソリューションの需要を後押ししています。

待機型建設用発電機セット市場は、燃料タイプ別にディーゼル、ガス、その他に区分され、ディーゼル発電機が圧倒的な地位を維持しています。ディーゼル発電機は、その優れた燃料効率、耐久性、大規模かつ重要な建設環境で信頼性の高い電力を供給する能力により、2024年の市場シェアは77.5%を占めました。より環境に優しい選択肢を求める動きが強まっているにもかかわらず、ディーゼルは、無停電電源供給が重要な大型用途に依然として好まれています。燃料効率と排出ガス規制の継続的な進歩により、ディーゼル発電セットの魅力はさらに高まっています。

北米の待機型建設用発電機セット市場は、ハイブリッド電源ソリューション、燃料効率の改善、遠隔監視機能の強化などの継続的な技術進歩により、2034年までCAGR 8%で拡大すると予想されます。こうした技術革新は、建設会社がコストを最適化しながら中断のない操業を維持するのに役立っており、地域全体で信頼性の高いバックアップ電源ソリューションへの需要が高まっています。都市化が進み、建設プロジェクトが大規模化するにつれて、次世代予備発電機への投資は引き続き堅調に推移し、市場の成長をさらに促進すると予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模と予測:電力定格別

- 主要動向

- 50 kVA以下

- 50 kVA-125 kVA

- 125 kVA-200 kVA

- 200 kVA-330 kVA

- 330 kVA-750 kVA

- 750 kVA超

第6章 市場規模・予測:燃料別

- 主要動向

- ディーゼル

- ガス

- その他

第7章 市場規模・予測:地域別

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- フィリピン

- ミャンマー

- バングラデシュ

- 中東

- サウジアラビア

- UAE

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- アンゴラ

- ケニア

- モザンビーク

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

第8章 企業プロファイル

- Aggreko

- Ashok Leyland

- Atlas Copco AB

- Caterpillar

- Cummins, Inc.

- Deere &Company

- Generac Power Systems, Inc.

- Greaves Cotton Limited

- HIMOINSA

- J C Bamford Excavators Ltd.

- Kirloskar

- Kohler Co.

- Mahindra Powerol

- Mitsubishi Heavy Industries Ltd.

- Powerica Limited

- Sterling and Wilson Pvt. Ltd.

- Wärtsilä

- Yamaha Motor Co., Ltd.

The Global Standby Construction Generator Sets Market was valued at USD 3.2 billion in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. This rapid expansion is fueled by accelerating infrastructure development, urbanization, and the increasing integration of artificial intelligence (AI) and automation technologies into standby generator systems. As construction projects become more complex and power reliability remains a top priority, demand for advanced generator solutions is rising. The construction industry is experiencing a surge in new developments, particularly in emerging economies, where electrification challenges necessitate dependable backup power sources. The need for generators is further amplified by extreme weather conditions, grid instability, and the rising incidence of power outages in various regions. Furthermore, investments in renewable energy and hybrid power solutions are influencing market trends, pushing manufacturers to innovate with cleaner and more efficient standby generator models.

Tighter environmental regulations aimed at reducing carbon emissions are accelerating the adoption of low-emission generator technologies. Features such as automatic load management and smart fuel optimization are gaining traction, enabling companies to improve fuel efficiency while meeting stringent sustainability standards. With governments worldwide enforcing policies to curb emissions from construction activities, businesses are actively investing in compliant, high-efficiency backup power solutions. Additionally, increasing operational cost concerns are driving the shift toward smarter generator systems that reduce fuel consumption without compromising power output. Innovations in hybrid generator systems, which combine traditional fuel sources with battery storage and renewable energy, are gaining momentum in response to sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 8.8% |

The <= 50 kVA power rating segment is poised for substantial growth, with a forecasted CAGR of 9% through 2034. This growth is attributed to the rising preference for compact, fuel-efficient generators that cater to small- and medium-scale construction projects. These generators are gaining popularity due to their ability to provide reliable power at a lower operational cost, making them an attractive choice for builders focused on cost-effectiveness and efficiency. Smaller construction projects, remote sites, and emergency backup requirements are fueling demand for these portable and scalable power solutions.

The standby construction generator sets market is segmented by fuel type into diesel, gas, and others, with diesel-powered generators maintaining a dominant position. Diesel generators held a 77.5% market share in 2024, owing to their superior fuel efficiency, durability, and capacity to provide reliable power in large-scale and critical construction environments. Despite the increasing push for greener alternatives, diesel remains the preferred choice for heavy-duty applications where uninterrupted power supply is crucial. Continuous advancements in fuel efficiency and emissions control are further enhancing the appeal of diesel-powered generator sets.

North America standby construction generator sets market is expected to expand at a CAGR of 8% through 2034, driven by ongoing technological advancements, including hybrid power solutions, improved fuel efficiency, and enhanced remote monitoring capabilities. These innovations are helping construction companies maintain uninterrupted operations while optimizing costs, reinforcing the demand for reliable backup power solutions across the region. As urbanization continues and construction projects scale up, investments in next-generation standby generators are expected to remain strong, further propelling market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic outlook

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel (USD Million & Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.4.11 Myanmar

- 7.4.12 Bangladesh

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.6.6 Kenya

- 7.6.7 Mozambique

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Ashok Leyland

- 8.3 Atlas Copco AB

- 8.4 Caterpillar

- 8.5 Cummins, Inc.

- 8.6 Deere & Company

- 8.7 Generac Power Systems, Inc.

- 8.8 Greaves Cotton Limited

- 8.9 HIMOINSA

- 8.10 J C Bamford Excavators Ltd.

- 8.11 Kirloskar

- 8.12 Kohler Co.

- 8.13 Mahindra Powerol

- 8.14 Mitsubishi Heavy Industries Ltd.

- 8.15 Powerica Limited

- 8.16 Sterling and Wilson Pvt. Ltd.

- 8.17 Wärtsilä

- 8.18 Yamaha Motor Co., Ltd.