|

市場調査レポート

商品コード

1699348

リニューアブルディーゼル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Renewable Diesel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| リニューアブルディーゼル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 128 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

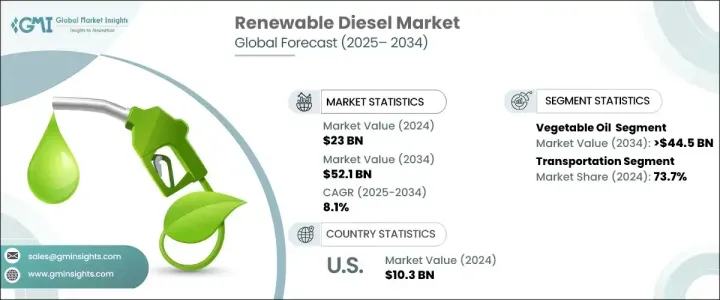

世界のリニューアブルディーゼル市場は2024年に230億米ドルとなり、2025年から2034年にかけてCAGR 8.1%で成長すると予測されています。

世界中の産業界や政府が従来の石油ベースのディーゼルに代わるものを求めており、よりクリーンなエネルギーソリューションの推進がこの市場を牽引し続けています。リニューアブルディーゼルは、温室効果ガス排出量の削減やカーボンフットプリントの削減など、環境面で大きなメリットがあり、持続可能な燃料源への移行において好ましい選択肢となっています。混合が必要なバイオディーゼルとは異なり、リニューアブルディーゼルは石油ディーゼルの直接代替品であり、既存のエンジンやインフラを改造することなく使用できます。この利点により、特に輸送、ロジスティクス、大型用途など、さまざまな分野で採用が加速しています。

気候変動に対する懸念の高まりと、炭素排出を対象とする厳しい規制が、市場情勢をさらに強化しています。米国、カナダ、欧州の各国政府は、税額控除、補助金、低炭素燃料の義務化を通じて、リニューアブルディーゼルの生産と使用を奨励する政策を実施しています。さらに、運輸、建設、農業の各分野で事業を展開する企業は、持続可能性の目標に合わせてリニューアブルディーゼルを事業に組み込んでいます。企業の車両と自治体の交通機関の両方からカーボンニュートラルな代替燃料に対する需要が高まっていることから、今後10年間の市場成長が強化されると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 230億米ドル |

| 予測金額 | 521億米ドル |

| CAGR | 8.1% |

この拡大を後押ししている主な要因の一つは、リニューアブルディーゼル生産における植物油の利用拡大であり、2034年までに445億米ドルを生み出すと予測されています。大豆油、キャノーラ油、パーム油などの植物油は、再生可能で生分解性のある原料の選択肢を提供し、排出を大幅に削減しながら燃料効率を高める。これらの原料はエネルギー密度が高く、リニューアブルディーゼルはエンジン出力、燃焼効率、信頼性において従来のディーゼルの性能を再現することができます。産業界が運転性能に妥協することなく、よりクリーンな燃料の選択肢を求める中、主要原料としての植物油の使用は勢いを増しています。

運輸部門は、2024年の市場シェア全体の73.7%を占め、依然として支配的な用途分野です。物流業者、公共交通機関、大型車両によるリニューアブルディーゼルの採用が増加しているのは、排出量を削減しながら車両性能を維持できることが背景にあります。商業輸送における低炭素燃料の需要は、企業が持続可能性へのコミットメントと規制要件に対応するにつれて急増しています。ESG(環境、社会、ガバナンス)政策が重視されるようになるにつれ、フリートオペレーターは、将来を見据えてリニューアブルディーゼルへの投資を増やしています。

北米のリニューアブルディーゼル市場は、2024年に103億米ドルと評価され、世界市場の47.5%のシェアを獲得しました。このシェアは、再生可能燃料基準(RFS)や低炭素燃料基準(LCFS)のような政府の先進的な取り組みに支えられて、2034年までに上昇すると予想されています。これらの政策は、運輸、農業から建設、製造に至るまで、様々な産業でより高い導入を促進しています。また、大手エネルギー企業や燃料メーカーからの投資に支えられたこの地域の生産能力の拡大は、リニューアブルディーゼルの強固なサプライチェーンを育み、よりクリーンな代替燃料としての長期的な生存可能性を確実なものにしています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- 1次調査と検証

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:原料別、2021年~2034年

- 主要動向

- 動物性脂肪

- 植物油

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 輸送

- 発電

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- アジア太平洋

- 中国

- インド

- インドネシア

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- BP

- Chevron

- Diamond Green Diesel

- Eni

- Gevo

- Marathon Petroleum

- Neste

- PBF Energy

- Repsol

- Shell

- Valero

- World Energy

The Global Renewable Diesel Market was valued at USD 23 billion in 2024 and is projected to grow at a CAGR of 8.1% between 2025 and 2034. The push for cleaner energy solutions continues to drive this market as industries and governments worldwide seek alternatives to conventional petroleum-based diesel. Renewable diesel offers significant environmental benefits, including lower greenhouse gas emissions and reduced carbon footprints, making it a preferred choice in the transition toward sustainable fuel sources. Unlike biodiesel, which requires blending, renewable diesel is a direct substitute for petroleum diesel and can be used without modifying existing engines or infrastructure. This advantage is accelerating its adoption across multiple sectors, particularly in transportation, logistics, and heavy-duty applications.

Growing concerns over climate change and stringent regulations targeting carbon emissions are further strengthening the market landscape. Governments across the United States, Canada, and Europe are implementing policies that incentivize the production and use of renewable diesel through tax credits, subsidies, and low-carbon fuel mandates. Additionally, companies operating in transportation, construction, and agriculture are integrating renewable diesel into their operations to align with sustainability goals. The rising demand for carbon-neutral alternatives from both corporate fleets and municipal transit agencies is expected to reinforce market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23 Billion |

| Forecast Value | $52.1 Billion |

| CAGR | 8.1% |

One of the primary factors propelling this expansion is the increasing utilization of vegetable oils in renewable diesel production, which is projected to generate USD 44.5 billion by 2034. Vegetable oils, including soybean oil, canola oil, and palm oil, offer a renewable and biodegradable feedstock option that enhances fuel efficiency while significantly cutting down emissions. These feedstocks have high energy density, allowing renewable diesel to replicate the performance of traditional diesel in terms of engine power, combustion efficiency, and reliability. As industries strive for cleaner fuel options that do not compromise on operational performance, the use of vegetable oils as key feedstocks is gaining momentum.

The transportation sector remains the dominant application segment, accounting for 73.7% of the total market share in 2024. The rising adoption of renewable diesel by logistics providers, public transit systems, and heavy-duty fleets is driven by its ability to maintain vehicle performance while reducing emissions. The demand for low-carbon fuels in commercial transport is surging as companies respond to sustainability commitments and regulatory requirements. With growing emphasis on ESG (Environmental, Social, and Governance) policies, fleet operators are increasingly investing in renewable diesel to future-proof their operations.

North America renewable diesel market was valued at USD 10.3 billion in 2024, capturing a 47.5% share of the global market. This share is expected to rise by 2034, supported by progressive government initiatives like the Renewable Fuel Standard (RFS) and the Low Carbon Fuel Standard (LCFS). These policies are driving higher adoption across multiple industries, from transportation and agriculture to construction and manufacturing. The region's expanding production capacity, backed by investments from major energy companies and fuel producers, is also fostering a robust supply chain for renewable diesel, ensuring its long-term viability as a cleaner fuel alternative.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Feedstock, 2021 – 2034 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Animal fat

- 5.3 Vegetable oil

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Transportation

- 6.3 Power generation

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 BP

- 8.2 Chevron

- 8.3 Diamond Green Diesel

- 8.4 Eni

- 8.5 Gevo

- 8.6 Marathon Petroleum

- 8.7 Neste

- 8.8 PBF Energy

- 8.9 Repsol

- 8.10 Shell

- 8.11 Valero

- 8.12 World Energy