|

市場調査レポート

商品コード

1699347

アルミニウム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Aluminum Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| アルミニウム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

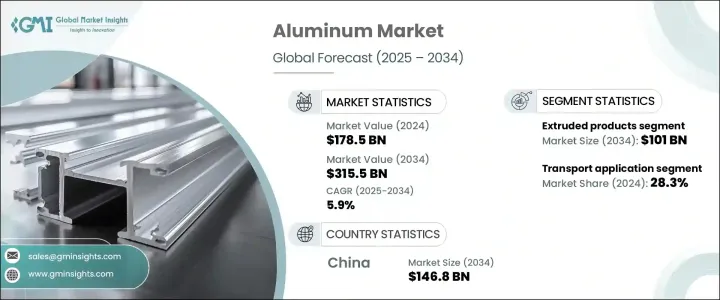

世界のアルミニウム市場は2024年に1,785億米ドルと評価され、2025年から2034年にかけて5.9%のCAGRで成長すると予測されています。

最も顕著な商品の一つとして、アルミニウムは特に工業用途で強い需要を見ています。一次アルミニウムの世界生産量は2023年に7,230万トンに達し、着実な拡大を示しています。同市場は、様々な産業における消費の増加から恩恵を受け、軽量素材、リサイクル可能性、製造工程の効率化によって大きな成長を遂げています。

製品タイプ別に見ると、アルミニウム市場は平板製品、鍛造製品、押出製品、長尺製品、鋳造製品、その他に分類されます。押出製品セグメントが最も高い成長を記録し、2024年には564億米ドルに達します。平板製品が僅差で続き、自動車産業と包装産業で重要な役割を果たすため、2024年には491億米ドルに達します。これらの製品は市場を独占し、総売上高の40%以上を占めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,785億米ドル |

| 予測金額 | 3,155億米ドル |

| CAGR | 5.9% |

押出製品は、特に建設・運輸部門で高い需要を維持しました。一方、平板製品は、自動車の軽量化の推進により、自動車産業で広く使用されるようになったため、脚光を浴びるようになりました。自動車部門だけでアルミニウム総消費量の約30%を占めています。さらに、航空宇宙、建築・建設、電気産業が市場拡大の主要な貢献者として浮上しました。アルミニウムは送電網、トランスミッション、大規模インフラプロジェクトで重要な役割を果たしています。

市場はさらに、圧延、押出、引抜、鋳造、鍛造などの加工方法によって区分されます。伸線加工は、主に高強度ワイヤー製造と航空宇宙部品への応用により、今後数年間は優位を占めると予想されます。アルミニウム鋳造は加工アルミニウムの20%を占め、特に自動車と産業機械に使用されています。先進加工技術は、排出物の削減とエネルギー効率の向上に重点を置き、業界の持続可能性への取り組みをさらに強化しました。

新技術は、生産コストと環境負荷の低減に貢献しました。競争企業間の敵対関係は緩やかであったが、新規参入企業にとっては高い設備投資が参入障壁となりました。軽量アルミニウム合金の需要は新たな機会を生み出したが、原料価格の変動が課題となっており、特にパンデミック後にコストが大幅に高騰しました。

市場は用途別に輸送、建設、電気・電子、包装、設備・機械、耐久消費財、箔材、その他に区分されます。2024年の市場シェアは輸送セクターが28.3%でリードしており、2034年までのCAGRは4.5%と予想されています。電気・電子分野が大きなシェアを占め、アルミニウムはトランスミッション、回路基板、熱交換器などに広く使用されています。包装分野は、アルミニウムのリサイクル性の高さから飲食品容器の材料として好まれ、市場の15.2%を占めました。産業用オートメーション部品を含む設備・機械も大きな伸びを示しました。

市場の見通しでは、特に包装と輸送において持続可能なアルミニウムの使用を促進する規制が進展していることが強調されました。サプライチェーンの混乱は課題となったが、ホイル在庫と耐久消費財需要の増加はアルミニウム市場の存在感を高めました。

中国のアルミニウム市場は2024年に809億米ドルを生み出し、2034年には1,468億米ドルに達すると予測されます。産業の多様性と強力な製造能力により、アジア太平洋地域が優位を占めています。中国は2024年にアルミニウム生産量の55%、世界消費量の50%近くを占め、一次アルミニウム生産量は4,200万トンと、2023年の生産量を上回りました。政府の政策、豊富なボーキサイト埋蔵量、エネルギー補助金がこの優位性に貢献しました。都市化とインフラの拡大がこの地域のアルミニウム需要をさらに押し上げました。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次調査と検証

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 自動車業界における軽量素材の需要増加

- 低炭素アルミニウム生産への取り組みの拡大

- アルミニウムのリサイクルと循環経済への注目の高まり

- 建設・インフラプロジェクトの成長

- 包装業界からの旺盛な需要

- アルミニウム加工技術の進歩

- 持続可能な金属生産を支援する政府の政策

- 業界の潜在的リスク&課題

- エネルギー制限と環境規制

- 原料価格の変動

- 世界・サプライチェーンに影響を及ぼす貿易摩擦

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- フラット製品

- 押出製品

- 鍛造製品

- 長尺製品

- 鋳造製品

- その他

第6章 市場推計・予測:加工方法別、2021年~2034年

- 主要動向

- 圧延

- 押出

- 引抜

- 鋳造

- 鍛造

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 輸送

- 建設

- 電気・電子

- 包装

- 設備・機械

- 耐久消費財

- 箔地

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alcoa

- Aleris Rolled Products

- Arconic

- Emirates Global Aluminum

- Hangzhou Century Aluminium

- Hindalco

- Hongqiao Group

- JW Aluminium

- Logan Aluminium

- Norsk Hydro

- Novelis

- Rio Tinto

- Rusal

- Shandong Xinfa Aluminium Group

- South32

- SPIC

- Vedanta Limited

The Global Aluminum Market was valued at USD 178.5 billion in 2024 and is projected to grow at a 5.9% CAGR from 2025 to 2034. As one of the most prominent commodities, aluminum has seen strong demand, particularly in industrial applications. The global production of primary aluminum reached 72.3 million tons in 2023, demonstrating steady expansion. The market benefits from increasing consumption in various industries, with significant growth driven by lightweight materials, recyclability, and efficiency in manufacturing processes.

Based on product type, the aluminum market is categorized into flat products, forged products, extruded products, long products, cast products, and others. The extruded products segment recorded the highest growth, reaching USD 56.4 billion in 2024. Flat products followed closely, reaching USD 49.1 billion in 2024 due to their significant role in the automotive and packaging industries. These products dominated the market, contributing to over 40% of total sales.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $178.5 Billion |

| Forecast Value | $315.5 Billion |

| CAGR | 5.9% |

Extruded products remained in high demand, especially within the construction and transportation sectors. Meanwhile, flat products gained prominence due to their widespread use in the automotive industry, driven by the push for lightweight vehicles. The automotive sector alone accounted for approximately 30% of total aluminum consumption. Additionally, aerospace, building & construction, and the electrical industry emerged as key contributors to market expansion. Aluminum played a crucial role in power grids, transmission lines, and large-scale infrastructure projects.

The market is further segmented based on processing methods, including rolling, extruding, drawing, casting, and forging. The drawing process is expected to dominate in the coming years, mainly due to its application in high-strength wire manufacturing and aerospace components. Aluminum casting accounted for 20% of processed aluminum, particularly within automotive and industrial machinery. Advanced processing technologies focused on reducing emissions and enhancing energy efficiency, further strengthening the industry's sustainability initiatives.

New technologies helped lower production costs and environmental impact. Despite moderate competitive rivalry, high capital investments acted as entry barriers for new players. The demand for lightweight aluminum alloys created new opportunities, although raw material price fluctuations presented challenges, especially as costs surged significantly post-pandemic.

The market is segmented by application into transport, construction, electrical & electronics, packaging, equipment & machinery, consumer durables, foil stock, and others. The transportation sector led with a 28.3% market share in 2024 and is anticipated to grow at a 4.5% CAGR through 2034. The electrical & electronics segment held a substantial share, with aluminum widely used in power transmission, circuit boards, and heat exchangers. Packaging contributed 15.2% of the market, as aluminum's recyclability made it a preferred material for food and beverage containers. Equipment & machinery, including industrial automation components, also saw significant growth.

The market outlook highlighted evolving regulations promoting sustainable aluminum usage, particularly in packaging and transportation. Supply chain disruptions posed challenges, while the rise in foil stock and consumer durables demand reinforced aluminum's market presence.

The aluminum market in China generated USD 80.9 billion in 2024 and is projected to reach USD 146.8 billion by 2034. The Asia Pacific region dominated due to industrial diversity and strong manufacturing capabilities. China accounted for 55% of aluminum production and nearly 50% of global consumption in 2024, producing 42 million tons of primary aluminum, surpassing its 2023 output. Government policies, abundant bauxite reserves, and energy subsidies contributed to this dominance. Urbanization and infrastructure expansion further fueled aluminum demand in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for lightweight materials in automotive

- 3.6.1.2 Expanding low-carbon aluminium production initiatives

- 3.6.1.3 Increasing aluminium recycling and circular economy focus

- 3.6.1.4 Growth in construction and infrastructure projects

- 3.6.1.5 Strong demand from the packaging industry

- 3.6.1.6 Advancements in aluminium processing technologies

- 3.6.1.7 Government policies supporting sustainable metal production

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Energy restrictions and environmental regulations

- 3.6.2.2 Volatility in raw material prices

- 3.6.2.3 Trade tensions affecting global supply chains

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Carats)

- 5.1 Key trends

- 5.2 Flat products

- 5.3 Extruded products

- 5.4 Forged products

- 5.5 Long products

- 5.6 Cast products

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Processing Method, 2021 – 2034 (USD Billion) (Carats)

- 6.1 Key trends

- 6.2 Rolling

- 6.3 Extruding

- 6.4 Drawn

- 6.5 Casting

- 6.6 Forging

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Carats)

- 7.1 Key trends

- 7.2 Transport

- 7.3 Construction

- 7.4 Electrical & electronics

- 7.5 Packaging

- 7.6 Equipment & machinery

- 7.7 Consumer durables

- 7.8 Foil stock

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Carats)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alcoa

- 9.2 Aleris Rolled Products

- 9.3 Arconic

- 9.4 Emirates Global Aluminum

- 9.5 Hangzhou Century Aluminium

- 9.6 Hindalco

- 9.7 Hongqiao Group

- 9.8 JW Aluminium

- 9.9 Logan Aluminium

- 9.10 Norsk Hydro

- 9.11 Novelis

- 9.12 Rio Tinto

- 9.13 Rusal

- 9.14 Shandong Xinfa Aluminium Group

- 9.15 South32

- 9.16 SPIC

- 9.17 Vedanta Limited