|

市場調査レポート

商品コード

1699343

ロボットソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Robotic Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ロボットソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

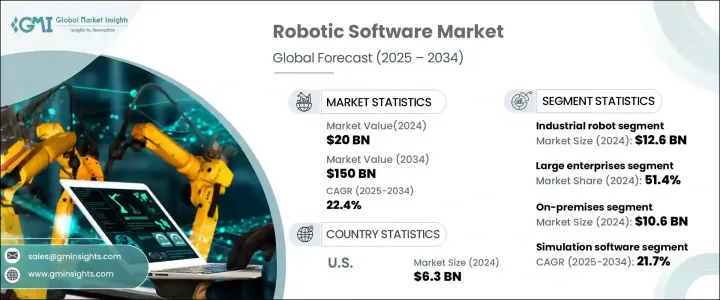

世界のロボットソフトウェア市場は、2024年に200億米ドルと評価され、2025年から2034年にかけてCAGR 22.4%で拡大すると予想されています。

この成長の原動力となっているのは、ロボットソフトウェアへの人工知能や機械学習の統合が進んでいることと、協働ロボットの需要が各業界で高まっていることです。企業は、業務の合理化、コスト削減、生産性向上のため、インテリジェントな自動化ソリューションに多額の投資を行っています。AIとMLは、データ主導の意思決定、ダイナミックな環境への適応、複雑なタスクの高精度な実行を可能にすることで、ロボットシステムに変革をもたらしつつあります。

こうした進歩は、製造、ヘルスケア、物流、農業などの分野で特に顕著であり、自動化によって効率が最適化され、全体的な生産高が向上しています。労働集約的で反復的なプロセスにおけるロボット工学への依存の高まりは、ロボットのパフォーマンスを管理、分析、強化できる高度なソフトウェア・ソリューションの需要を促進しています。さらに、世界中の政府や企業がスマートロボットへの投資を強化しており、市場の拡大をさらに加速させています。クラウドベースのロボット工学、強化された接続性、シームレスなソフトウェア統合の台頭により、ロボット・アプリケーションはよりスケーラブルで利用しやすくなり、あらゆる規模の企業が自動化を活用して競争優位に立つための新たな機会が開かれています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 200億米ドル |

| 予測金額 | 1,500億米ドル |

| CAGR | 22.4% |

市場はロボットタイプによって区分され、産業用ロボットとサービスロボットが2大カテゴリーです。2024年には、産業用ロボットソフトウェアが126億米ドルを占め、市場を席巻します。これらのシステムは、製造・組立プロセスの自動化、エラーの削減、業務効率の向上に不可欠です。産業用ロボット・ソフトウェアには、ロボット操作に関するリアルタイムの洞察を提供する強力なデータ分析ツールが組み込まれており、企業はパフォーマンスを最適化し、ダウンタイムを最小限に抑え、製品品質を高めることができます。さらに、シミュレーションや可視化ツールなどの機能により、ユーザーは導入前に潜在的な問題を予測・軽減し、生産環境へのシームレスな統合を実現することができます。産業界では、増大する需要に対応し競争力を維持するために自動化を優先する傾向が強まっており、産業用ロボットソフトウェアの採用は大幅に増加する見込みです。

企業規模は、ロボットソフトウェア市場を形成するもう一つの重要なセグメントであり、大企業と中小企業(SME)の両方を包含します。2024年の市場シェアは大企業が51.4%を占め、ロボットソリューションの採用において大企業が支配的な役割を担っていることを浮き彫りにしています。これらの組織は、複数の生産ライン、倉庫、物流センターを運営しており、シームレスな調整、タスク管理、プロセス最適化のための高度なソフトウェアが必要とされています。ロボットソフトウェアは、大企業がパフォーマンスを監視し、反復作業を自動化し、スケーラビリティを強化することを可能にし、最終的に効率向上とコスト削減につながります。一方、中小企業もオペレーションの俊敏性を向上させ、人件費を最小限に抑え、進化するビジネス環境でより効果的に競争するために、ロボットによる自動化への投資を増やしています。

米国のロボット・ソフトウェア市場の2024年の市場規模は63億米ドルで、自動化と高度なロボット工学の導入における同国のリーダーシップを反映しています。製造、ヘルスケア、ロジスティクスなどの業界がインテリジェントオートメーションを採用する中、ロボットソフトウェア・ソリューションの需要は急増し続けています。コスト効率に優れ、効率的で正確な製造プロセスを求める動きは、AIを搭載したロボット工学を導入して生産品質を向上させ、人的介入を減らすよう企業を駆り立てています。米国企業がインテリジェント・オートメーションによるオペレーションの最適化を模索する中、米国は世界のロボット・ソフトウェアの展望を形成する重要なプレーヤーであり続けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- ロボットソフトウェアへのAIとMLの統合の拡大

- 協働ロボットの需要の高まり

- 各業界における自動化の進展

- 様々な分野でのロボット導入の増加

- 業界の潜在的リスク&課題

- 高額な初期投資

- 既存システムとの統合が複雑

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソフトウェアタイプ別、2021年~2034年

- 主要動向

- シミュレーションソフトウェア

- ナビゲーション・地図作成ソフトウェア

- データ分析・管理ソフトウェア

- ビジョン・ソフトウェア

- 予知保全ソフトウェア

- その他

第6章 市場推計・予測:ロボットタイプ別、2021年~2034年

- 主要動向

- 産業用ロボット

- サービスロボット

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第8章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 大企業

- 中小企業(SME)

第9章 市場推計・予測:エンドユーザー産業別、2021年~2034年

- 主要動向

- 製造業

- 自動車

- ヘルスケア

- 運輸・物流

- BFSI

- 小売・eコマース

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ABB Ltd

- Amazon Robotics(Amazon.com, Inc.)

- Autodesk, Inc.

- Blue Prism Group plc

- Boston Dynamics

- Clearpath Robotics

- Cognex Corporation

- Denso Corporation

- FANUC Corporation

- Hanson Robotics

- iRobot Corporation

- KUKA AG

- Mitsubishi Electric Corporation

- NVIDIA Corporation

- Omron Corporation

- Open Robotics(OSRF)

- Rockwell Automation, Inc.

- Siemens AG

- SoftBank Robotics

- Teradyne Inc.

- UiPath Inc.

- Universal Robots A/S

- Vecna Robotics

- Yaskawa Electric Corporation

The Global Robotic Software Market was valued at USD 20 billion in 2024 and is expected to expand at a CAGR of 22.4% from 2025 to 2034. This growth is being driven by the increasing integration of artificial intelligence and machine learning into robotic software, as well as the rising demand for collaborative robots across industries. Businesses are investing heavily in intelligent automation solutions to streamline operations, reduce costs, and enhance productivity. AI and ML are transforming robotic systems by enabling them to make data-driven decisions, adapt to dynamic environments, and perform complex tasks with greater precision.

These advancements are particularly evident in sectors such as manufacturing, healthcare, logistics, and agriculture, where automation is optimizing efficiency and improving overall output. The growing reliance on robotics for labor-intensive and repetitive processes is fueling the demand for advanced software solutions capable of managing, analyzing, and enhancing robot performance. Additionally, governments and enterprises worldwide are ramping up investments in smart robotics, further accelerating market expansion. The rise of cloud-based robotics, enhanced connectivity, and seamless software integration is making robotic applications more scalable and accessible, opening new opportunities for businesses of all sizes to leverage automation for competitive advantage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20 Billion |

| Forecast Value | $150 Billion |

| CAGR | 22.4% |

The market is segmented based on the type of robot, with industrial robots and service robots being the two primary categories. In 2024, industrial robot software dominated the market, accounting for USD 12.6 billion. These systems are essential for automating manufacturing and assembly processes, reducing errors, and improving operational efficiency. Industrial robot software incorporates powerful data analytics tools that provide real-time insights into robotic operations, allowing businesses to optimize performance, minimize downtime, and enhance product quality. Additionally, features such as simulation and visualization tools enable users to anticipate and mitigate potential issues before deployment, ensuring seamless integration into production environments. As industries increasingly prioritize automation to meet growing demands and maintain a competitive edge, the adoption of industrial robot software is set to rise significantly.

Enterprise size is another crucial segment shaping the robotic software market, encompassing both large enterprises and small and medium-sized enterprises (SMEs). Large enterprises accounted for a 51.4% market share in 2024, highlighting their dominant role in adopting robotic solutions. These organizations operate multiple production lines, warehouses, and logistics centers, necessitating advanced software for seamless coordination, task management, and process optimization. Robotic software enables large companies to monitor performance, automate repetitive tasks, and enhance scalability, ultimately leading to higher efficiency and cost savings. Meanwhile, SMEs are also increasingly investing in robotic automation to improve operational agility, minimize labor costs, and compete more effectively in an evolving business landscape.

The U.S. robotic software market was valued at USD 6.3 billion in 2024, reflecting the country's leadership in automation and advanced robotics adoption. With industries such as manufacturing, healthcare, and logistics embracing intelligent automation, demand for robotic software solutions continues to surge. The push for cost-effective, efficient, and precise manufacturing processes is driving businesses to implement AI-powered robotics to enhance production quality and reduce human intervention. As American companies seek to optimize operations through intelligent automation, the U.S. remains a key player in shaping the global robotic software landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing integration of AI and ML into robotic software

- 3.6.1.2 Rising demand for collaborative robots

- 3.6.1.3 Increased automation across industries

- 3.6.1.4 Raising the adoption of robots across various sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investments

- 3.6.2.2 Complexes in integration with existing systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Software Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Simulation software

- 5.3 Navigation and mapping software

- 5.4 Data analytics and management software

- 5.5 Vision software

- 5.6 Predictive maintenance software

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Industrial robot

- 6.3 Service robot

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Large enterprise

- 8.3 Small and Medium Enterprises (SME)

Chapter 9 Market Estimates & Forecast, By End-use Industry, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Manufacturing

- 9.3 Automotive

- 9.4 Healthcare

- 9.5 Transportation and logistics

- 9.6 BFSI

- 9.7 Retail & e-commerce

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB Ltd

- 11.2 Amazon Robotics (Amazon.com, Inc.)

- 11.3 Autodesk, Inc.

- 11.4 Blue Prism Group plc

- 11.5 Boston Dynamics

- 11.6 Clearpath Robotics

- 11.7 Cognex Corporation

- 11.8 Denso Corporation

- 11.9 FANUC Corporation

- 11.10 Hanson Robotics

- 11.11 iRobot Corporation

- 11.12 KUKA AG

- 11.13 Mitsubishi Electric Corporation

- 11.14 NVIDIA Corporation

- 11.15 Omron Corporation

- 11.16 Open Robotics (OSRF)

- 11.17 Rockwell Automation, Inc.

- 11.18 Siemens AG

- 11.19 SoftBank Robotics

- 11.20 Teradyne Inc.

- 11.21 UiPath Inc.

- 11.22 Universal Robots A/S

- 11.23 Vecna Robotics

- 11.24 Yaskawa Electric Corporation