|

市場調査レポート

商品コード

1699323

石油・ガスインフラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Oil and Gas Infrastructure Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 石油・ガスインフラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月21日

発行: Global Market Insights Inc.

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

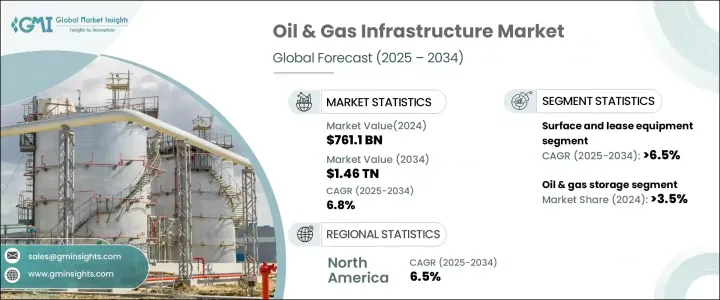

世界の石油・ガスインフラ市場は、2024年に7,611億米ドルに達し、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。

新興国を中心とした石油・ガス需要の増加と、大規模インフラ・プロジェクトへの投資の急増が、業界拡大の原動力となっています。エネルギー部門が急速な変革を遂げる中、各国はインフラ強化と経営効率強化に多大な資源を投入しています。エネルギー消費の増加と技術の進歩が相まって、効率的な輸送・貯蔵・処理施設の開発が加速しています。

同産業は、地上設備・リース設備、収集・加工、パイプライン、貯蔵、精製・輸送、輸出ターミナルなど、いくつかのセグメントに分類されます。地上設備とリース設備は、探査と生産活動の拡大に牽引され、2034年までにCAGR 6.5%で成長すると予想されます。タイトガスやシェールガスの採掘など、非従来型の掘削技術の導入が増加していることが、操業をサポートする高度な機器への需要をさらに高めています。エネルギー生産者が効率性の向上と生産の最適化を目指す中、地表インフラへの投資は引き続き重要です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7,611億米ドル |

| 予測金額 | 1兆4,600億米ドル |

| CAGR | 6.8% |

石油・ガス貯蔵セクターの2024年のシェアは3.5%で、天然ガスをベースとする経済へのシフトと世界貿易の拡大により需要が増加しています。大規模な貯蔵ソリューションに対するニーズが高まっているのは、石油化学および製油所の活動が活発化していることに起因しており、そこでは原油、原料、ジェット燃料、ディーゼル、ガソリンなどの石油精製品を収容するために大きな容量が必要とされています。供給の柔軟化と貯蔵インフラの強化が市場の成長を後押しし、変動する需要に対応する安定したエネルギー供給が確保されています。

米国の石油・ガスインフラ市場は、2024年に804億米ドルと評価され、2034年には1,500億米ドルになると予測されています。エネルギーインフラへの戦略的投資は、国家のエネルギー安全保障を強化し、サプライ・チェーンの脆弱性を最小化し、途切れない燃料供給を保証します。同国は、液化プラントと精製ターミナルの近代化と拡張に注力しており、先端技術の業界導入を加速させています。パイプライン・ネットワーク、貯蔵施設の拡張、高度な精製施設への資本支出の増加は、セクターの成長を促進し、米国が石油・ガスインフラにおける支配的プレイヤーとしての地位を維持することを可能にしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:カテゴリー別、2021年~2034年

- 主要動向

- 地上設備とリース設備

- 採掘・加工

- 石油・ガス・NGLパイプライン

- 石油・ガス貯蔵

- 精製・石油製品輸送

- 輸出ターミナル

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ノルウェー

- 英国

- フランス

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- カタール

- ナイジェリア

- UAE

- オマーン

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

第7章 企業プロファイル

- Baker Hughes Company

- BP

- Centrica

- Chevron Corporation

- ConocoPhillips

- Energy Transfer

- Enterprise Products Partners

- Exxon Mobil Corporation

- Hatch

- Halliburton

- Kinder Morgan

- Marathon Oil Company

- NGL Energy Partners

- Occidental Petroleum Corporation

- ONEOK

- Royal Vopak

- SLB

- Shell

- TotalEnergies

- WILLIAMS

The Global Oil and Gas Infrastructure Market reached USD 761.1 billion in 2024 and is projected to grow at a CAGR of 6.8% from 2025 to 2034. The increasing demand for oil and gas, especially in emerging economies, combined with surging investments in large-scale infrastructure projects, is set to drive industry expansion. With the energy sector undergoing rapid transformation, nations are allocating significant resources to strengthen their infrastructure and enhance operational efficiency. Rising energy consumption, coupled with advancements in technology, is accelerating the development of efficient transportation, storage, and processing facilities.

The industry is classified into several segments, including surface and lease equipment, gathering and processing, pipelines, storage, refining and transportation, and export terminals. Surface and lease equipment is expected to grow at a CAGR of 6.5% by 2034, driven by the expansion of exploration and production activities. The rising implementation of unconventional drilling techniques, such as tight gas and shale gas extraction, is further fueling demand for advanced equipment to support operations. As energy producers seek to enhance efficiency and optimize production, investment in surface infrastructure remains critical.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $761.1 Billion |

| Forecast Value | $1.46 Trillion |

| CAGR | 6.8% |

The oil & gas storage sector held a 3.5% share in 2024, with demand increasing due to a shift toward a natural gas-based economy and expanding global trade. The growing need for large-scale storage solutions stems from heightened petrochemical and refinery activities, where significant capacities are required to accommodate crude oil, feedstocks, and refined petroleum products, including jet fuel, diesel, and gasoline. The push for supply flexibility and enhanced storage infrastructure is reinforcing market growth, ensuring a stable energy supply to meet fluctuating demand.

United States oil & gas infrastructure market was valued at USD 80.4 billion in 2024, with projections expected to generate USD 150 billion by 2034. Strategic investments in energy infrastructure are reinforcing national energy security, minimizing supply chain vulnerabilities, and ensuring uninterrupted fuel distribution. The country is focusing on modernizing and expanding liquefaction plants and refining terminals, accelerating industry adoption of cutting-edge technologies. Increased capital expenditure in pipeline networks, storage expansions, and advanced refining facilities is fostering sectoral growth, allowing the US to maintain its position as a dominant player in the oil and gas infrastructure landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Category, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Surface and lease equipment

- 5.3 Gathering & processing

- 5.4 Oil, gas & NGL pipelines

- 5.5 Oil & gas storage

- 5.6 Refining & oil products transport

- 5.7 Export terminals

Chapter 6 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Norway

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 Qatar

- 6.5.3 Nigeria

- 6.5.4 UAE

- 6.5.5 Oman

- 6.5.6 Egypt

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

- 6.6.3 Mexico

Chapter 7 Company Profiles

- 7.1 Baker Hughes Company

- 7.2 BP

- 7.3 Centrica

- 7.4 Chevron Corporation

- 7.5 ConocoPhillips

- 7.6 Energy Transfer

- 7.7 Enterprise Products Partners

- 7.8 Exxon Mobil Corporation

- 7.9 Hatch

- 7.10 Halliburton

- 7.11 Kinder Morgan

- 7.12 Marathon Oil Company

- 7.13 NGL Energy Partners

- 7.14 Occidental Petroleum Corporation

- 7.15 ONEOK

- 7.16 Royal Vopak

- 7.17 SLB

- 7.18 Shell

- 7.19 TotalEnergies

- 7.20 WILLIAMS