|

市場調査レポート

商品コード

1699320

検査ロボットの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Inspection Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 検査ロボットの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月21日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

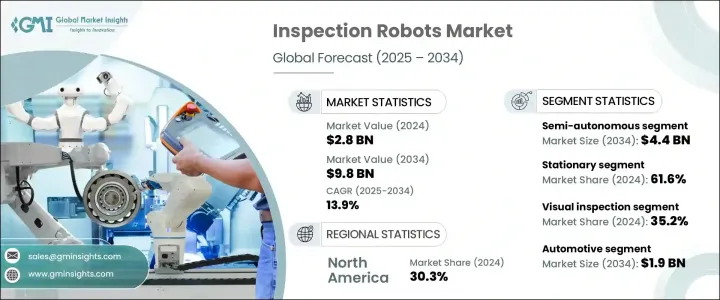

検査ロボットの世界市場は、2024年に28億米ドルと評価され、2025年から2034年にかけてCAGR13.9%で拡大する見通しです。

成長の原動力となっているのは、効率性の向上、運用リスクの低減、進化する安全規制への準拠を目指す業界全体における採用の増加です。製造、エネルギー、インフラの各分野の企業は、ワークフローを合理化し、ダウンタイムを最小限に抑え、厳しい業界基準へのコンプライアンスを確保するために、検査ロボットを業務に組み込んでいます。

自動化と高精度が優先される中、検査ロボットはメンテナンスと品質管理において重要な役割を果たしています。これらの先進的なシステムは、精度と信頼性を高め、手作業による検査に伴う制約を解消します。組織は、非破壊検査、リアルタイム分析、予知保全に対する需要の高まりに対応するため、ロボットを活用しています。人工知能(AI)と機械学習(ML)技術への投資の増加は、ロボット検査システムの技術革新をさらに促進し、自律的な意思決定と適応学習を可能にしています。危険で手が届きにくい環境での継続的なモニタリングの必要性は、企業が業務パフォーマンスを最適化しながら職場の安全性を向上させることを目指しているため、需要が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 28億米ドル |

| 予測金額 | 98億米ドル |

| CAGR | 13.9% |

市場セグメンテーションには、非自律型ロボット、半自律型ロボット、完全自律型ロボットが含まれます。半自律型セグメントは2034年までに44億米ドルに達すると予想され、自動化と人間の監視のバランスを取る能力により、大幅な導入が見込まれています。これらのシステムはリスクの高い産業において特に価値が高く、AIが支援する意思決定により、人間のオペレーターは必要な場合にのみ介入することができます。複雑な環境でも常時監視することなく機能するAIは、重要な業務の管理を維持しながら効率性を高めようとする企業にとって魅力的な選択肢となります。

技術別に見ると、市場は据置型検査ロボットと移動型検査ロボットに区分されます。2024年には、据置型が市場シェアの61.6%を占め、その高精度と自動化された製造環境へのシームレスな統合により、人気を集めています。これらのロボットは、綿密な品質管理が要求される産業において、高精度の欠陥検出とリアルタイムでの性能監視を提供し、不可欠な役割を果たしています。非破壊検査や高速評価技術が重視されるようになったことも、導入に拍車をかけています。メーカー各社はエラーの削減と作業効率を優先しており、据置型検査ロボットは最新の生産ラインに不可欠なものとなっています。

米国の検査ロボット市場は大幅な成長が見込まれており、2034年には28億米ドルに達すると予測されています。製造業における自動化への依存の高まりと、欠陥検出や品質保証への強いこだわりが、ロボット検査システムの導入を加速させています。企業は、生産性の向上、ダウンタイムの最小化、業務効率の最適化を目的として、先進的なロボット技術に投資しています。オートメーションが産業ワークフローを変革し続ける中、ロボット検査システムは、一貫した品質と卓越したオペレーションを確保するために不可欠なコンポーネントとして台頭してきています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- サービスロボットの販売と導入の増加

- ドローンやモバイルロボットの遠隔検査への利用の増加

- スマートマニュファクチャリングとインダストリー4.0イニシアティブの成長

- 石油・ガス、エネルギー分野の拡大

- 各業界における厳しい安全・品質規制

- 業界の潜在的リスク・課題

- 中小企業にとっては高い導入コスト

- 複雑さと統合の難しさ

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 非自律型

- 半自律型

- 完全自律型

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 据置型

- 移動型

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 目視検査

- 超音波検査

- レーザースキャン検査

- 熱検査

- 品質検査

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- 建設

- 飲食品

- 製造業

- 石油・ガス

- 電力

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- ABB

- Cognex

- Denso Wave

- DSI Robotics

- Energy Robotics

- Fanuc

- Honeybee Robotics

- Innok Robotics

- JH Robotics

- Kuka

- Mitsubishi Heavy Industries

- Nexxis

- Robotnik Automation

- Staubli

- Superdroid Robotics

- Universal Robots

The Global Inspection Robots Market, valued at USD 2.8 billion in 2024, is set to expand at a CAGR of 13.9% from 2025 to 2034. The growth is driven by increasing adoption across industries seeking to enhance efficiency, reduce operational risks, and comply with evolving safety regulations. Businesses across manufacturing, energy, and infrastructure sectors are integrating inspection robots into their operations to streamline workflows, minimize downtime, and ensure compliance with stringent industry standards.

With industries prioritizing automation and precision, inspection robots are playing a critical role in maintenance and quality control. These advanced systems offer enhanced accuracy and reliability, eliminating the limitations associated with manual inspections. Organizations are leveraging robotics to meet growing demands for non-destructive testing, real-time analytics, and predictive maintenance. Increasing investments in artificial intelligence (AI) and machine learning (ML) technologies are further driving innovation in robotic inspection systems, enabling autonomous decision-making and adaptive learning. The need for continuous monitoring in hazardous and hard-to-reach environments is accelerating demand as companies aim to improve workplace safety while optimizing operational performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 13.9% |

Market segmentation by type includes non-autonomous, semi-autonomous, and fully autonomous robots. The semi-autonomous segment is expected to reach USD 4.4 billion by 2034, witnessing significant adoption due to its ability to strike a balance between automation and human oversight. These systems are particularly valuable in high-risk industries, where AI-assisted decision-making allows human operators to intervene only when necessary. Their ability to function in complex environments without constant supervision makes them an attractive choice for businesses seeking to enhance efficiency while maintaining control over critical operations.

Based on technology, the market is segmented into stationary and mobile inspection robots. In 2024, stationary systems accounted for 61.6% of the market share, gaining traction due to their high precision and seamless integration into automated manufacturing environments. These robots play an essential role in industries that demand meticulous quality control, offering high-accuracy defect detection and real-time performance monitoring. The growing emphasis on non-destructive testing and high-speed evaluation techniques is further fueling adoption. Manufacturers are prioritizing error reduction and operational efficiency, making stationary inspection robots indispensable across modern production lines.

The US inspection robots market is poised for substantial growth, projected to reach USD 2.8 billion by 2034. Increasing reliance on automation in manufacturing, coupled with a strong focus on defect detection and quality assurance, is accelerating the deployment of robotic inspection systems. Companies are investing in advanced robotic technologies to enhance productivity, minimize downtime, and optimize operational efficiency. As automation continues to transform industrial workflows, robotic inspection systems are emerging as an essential component in ensuring consistent quality and operational excellence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased sales and adoption of service robots

- 3.2.1.2 Increasing use of drones and mobile robots for remote inspections

- 3.2.1.3 Growth in smart manufacturing and industry 4.0 initiatives

- 3.2.1.4 Expansion of the oil & gas and energy sectors

- 3.2.1.5 Stringent safety and quality regulations across industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High deployment cost for SME

- 3.2.2.2 Complexity & integration difficulties

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Bn)

- 5.1 Key trends

- 5.2 Non-autonomous

- 5.3 Semi-autonomous

- 5.4 Fully autonomous

Chapter 6 Market Estimates and Forecast, By Technology , 2021 – 2034 (USD Bn)

- 6.1 Key trends

- 6.2 Stationary

- 6.3 Mobile

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Visual inspection

- 7.3 Ultrasonic inspection

- 7.4 Laser scanning inspection

- 7.5 Thermal inspection

- 7.6 Quality inspection

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Bn)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Construction

- 8.4 Food & beverages

- 8.5 Manufacturing

- 8.6 Oil & gas

- 8.7 Power

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Cognex

- 10.3 Denso Wave

- 10.4 DSI Robotics

- 10.5 Energy Robotics

- 10.6 Fanuc

- 10.7 Honeybee Robotics

- 10.8 Innok Robotics

- 10.9 JH Robotics

- 10.10 Kuka

- 10.11 Mitsubishi Heavy Industries

- 10.12 Nexxis

- 10.13 Robotnik Automation

- 10.14 Staubli

- 10.15 Superdroid Robotics

- 10.16 Universal Robots