ダイレクトチップ液体冷却市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Direct-to-chip Liquid Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699319

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

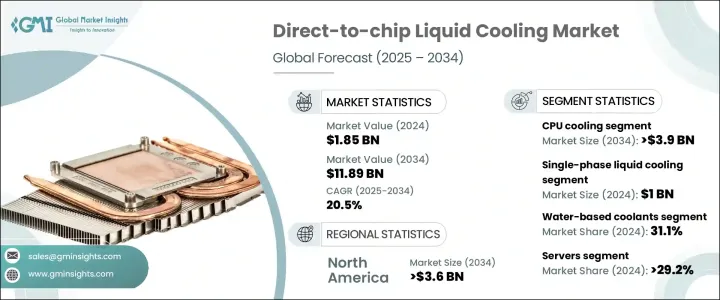

世界のダイレクトチップ液体冷却市場は2024年に18億5,000万米ドルと評価され、企業が高性能コンピューティング、エネルギー効率、持続可能なデータセンターソリューションを優先する傾向が強まる中、2025年から2034年にかけてCAGR 20.5%で拡大する見通しです。

人工知能(AI)、機械学習(ML)、クラウド・コンピューティングの急速な普及により、データ処理需要がかつてないほど急増しており、従来の冷却方法では高度なプロセッサの熱負荷の上昇を管理することが難しくなっています。世界中の組織は、システムの信頼性を高め、サーマルスロットリングを防止し、消費電力を最適化するために、チップに直接接続する液冷ソリューションに移行しています。グリーンデータセンターとカーボンフットプリントの削減が重視されるようになり、液冷は次世代コンピューティング・インフラに不可欠な技術革新として位置づけられ、採用がさらに加速しています。

ハイパフォーマンス・コンピューティング(HPC)環境が処理能力の限界を押し広げる中、従来の空冷方式ではCPU、GPU、メモリモジュールの放熱ニーズに対応するのに苦労しています。チップから液体クーラントに直接熱を移動させることで正確な熱管理を可能にするダイレクトチップ液体冷却は、データセンターの最適化におけるゲームチェンジャーとして台頭しています。クラウドサービスプロバイダー、ハイパースケールデータセンター、AI主導のワークロードを展開する企業は、液冷技術を統合して効率を最大化し、運用コストを最小限に抑えています。リアルタイムデータ分析、高密度コンピューティングクラスター、5Gインフラの展開に対する需要は、市場の拡大をさらに後押ししています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億5,000万米ドル |

| 予測金額 | 118億9,000万米ドル |

| CAGR | 20.5% |

同市場は、GPU冷却、CPU冷却、メモリ冷却、ASIC冷却、その他のコンポーネント別ソリューションで区分されます。CPU冷却分野は、プロセッサの消費電力を大幅に増加させるAIやクラウドベースのアプリケーションの普及により、2034年までに39億米ドルに達すると予測されています。先進的なCPUはかなりの熱負荷を発生させるため、システムの安定性を維持し性能低下を防ぐための最先端の熱管理ソリューションが必要となります。ダイレクトチップ液体冷却は優れた熱放散を実現し、極端な計算作業負荷の下でも持続的な性能を保証します。

市場はまた、水性クーラント、誘電流体、鉱物油、人工流体など、液体クーラントの種類によっても分類されます。2024年に31.1%の市場シェアを占めた水系クーラントは、その卓越した熱伝導性と費用対効果により人気を集めています。企業が持続可能性を重視する中、これらのクーラントは、高性能基準を維持しながらエネルギー消費を削減するための好ましい選択肢となりつつあります。優れた熱伝導特性により、効率と環境責任のバランスを追求する最新のデータセンターにとって理想的なソリューションとなっています。

北米は、ダイレクトチップ液体冷却市場を席巻し、2034年までに36億米ドルの市場規模になると予測されています。この地域では、データセンターの急速な拡大、クラウド・コンピューティング・エコシステムの成長、HPCソリューションに対する需要の高まりが、普及を後押ししています。2024年に78.4%という圧倒的な市場シェアを占める米国では、データインフラへの投資が急増しており、高度な冷却システムの必要性が高まっています。AI主導のアプリケーションとハイパースケールクラウドサービスがコンピューティングパワーの限界を押し上げる中、高効率熱管理ソリューションの需要は急増を続けており、進化するデータセンターの展望における米国市場のリーダーシップが強化されています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ハイパフォーマンス・コンピューティング(HPC)需要の高まり

- データセンターの高密度化

- 持続可能性への注目の高まり

- ハイパフォーマンス・コンピューティング需要の増加

- データセンターにおけるエネルギー効率と持続可能性への注目の高まり

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- 保守・運用の複雑さ

- 促進要因

- 成長可能性の分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:冷却ソリューションタイプ別、2021年~2034年

- 主要動向

- 単相液冷

- 二相液冷

第6章 市場推計・予測:コンポーネント冷却別、2021年~2034年

- 主要動向

- CPU冷却

- GPU冷却

- ASIC冷却

- メモリー冷却

- その他のコンポーネントの冷却

第7章 市場推計・予測:液体クーラントタイプ別、2021年~2034年

- 主要動向

- 水系クーラント

- 誘電性流体

- 鉱物油

- エンジニアードフルード

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- サーバー

- ワークステーション

- エッジコンピューティングデバイス

- スーパーコンピュータ

- ゲーミングPC

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- データセンター

- ハイパフォーマンス・コンピューティング(HPC)

- 人工知能/機械学習システム

- ゲームおよびeスポーツ

- 通信

- 金融サービス

- ヘルスケアおよびライフサイエンス

- 石油・ガス

- 自動車(電気自動車用バッテリー)

- 航空宇宙・防衛

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Asetek

- Alfa Laval

- Castrol

- Cisco Systems, Inc.

- CoolIT Systems

- DCX The Liquid Cooling Company

- Danfoss A/S

- DUG Technology

- Equinix, Inc.

- Fujitsu Limited

- Green Revolution Cooling(GRC)

- Huawei Technologies Co., Ltd.

- Iceotope Technologies Ltd.

- Inspur Systems

- LiquidCool Solutions

- LiquidStack

- Rittal GmbH &Co. KG

- Schneider Electric

- STULZ GmbH

- Submer Technologies

- Super Micro Computer, Inc.

- Vertiv Group Corp.

- ZutaCore

目次

The Global Direct-To-Chip Liquid Cooling Market, valued at USD 1.85 billion in 2024, is on track to expand at a CAGR of 20.5% from 2025 to 2034 as enterprises increasingly prioritize high-performance computing, energy efficiency, and sustainable data center solutions. The rapid proliferation of artificial intelligence (AI), machine learning (ML), and cloud computing is driving an unprecedented surge in data processing demands, making conventional cooling methods less effective in managing the rising thermal loads of advanced processors. Organizations worldwide are shifting toward direct-to-chip liquid cooling solutions to enhance system reliability, prevent thermal throttling, and optimize power consumption. The growing emphasis on green data centers and carbon footprint reduction further accelerates adoption, positioning liquid cooling as an essential innovation in next-generation computing infrastructure.

As high-performance computing (HPC) environments push the boundaries of processing power, traditional air-based cooling struggles to keep pace with the heat dissipation needs of CPUs, GPUs, and memory modules. Direct-to-chip liquid cooling, which enables precise thermal management by transferring heat directly from the chip to a liquid coolant, is emerging as a game-changer in data center optimization. Cloud service providers, hyperscale data centers, and enterprises deploying AI-driven workloads are integrating liquid cooling technologies to maximize efficiency and minimize operational costs. The demand for real-time data analytics, high-density computing clusters, and 5G infrastructure deployment is further reinforcing the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.85 Billion |

| Forecast Value | $11.89 Billion |

| CAGR | 20.5% |

Segmented by component cooling, the market encompasses GPU cooling, CPU cooling, memory cooling, ASIC cooling, and other component-specific solutions. The CPU cooling segment is projected to reach USD 3.9 billion by 2034, driven by the widespread adoption of AI and cloud-based applications that significantly increase processor power consumption. Advanced CPUs generate substantial heat loads, requiring cutting-edge thermal management solutions to maintain system stability and prevent performance degradation. Direct-to-chip liquid cooling delivers superior heat dissipation, ensuring sustained performance even under extreme computational workloads.

The market is also categorized by liquid coolant type, including water-based coolants, dielectric fluids, mineral oils, and engineered fluids. Water-based coolants, which held a 31.1% market share in 2024, are gaining traction due to their exceptional thermal conductivity and cost-effectiveness. As enterprises focus on sustainability, these coolants are becoming a preferred choice for reducing energy consumption while maintaining high-performance standards. Their superior heat transfer properties make them an ideal solution for modern data centers striving to balance efficiency and environmental responsibility.

North America is set to dominate the direct-to-chip liquid cooling market, with projections indicating a valuation of USD 3.6 billion by 2034. The region's rapid data center expansion, growing cloud computing ecosystem, and escalating demand for HPC solutions are driving widespread adoption. The United States, which held a commanding 78.4% market share in 2024, is witnessing soaring investments in data infrastructure, fueling the need for advanced cooling systems. With AI-driven applications and hyperscale cloud services pushing the limits of computing power, the demand for high-efficiency thermal management solutions continues to surge, reinforcing the U.S. market's leadership in the evolving data center landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-performance computing (HPC)

- 3.2.1.2 Increasing data center density

- 3.2.1.3 Increased focus on sustainability

- 3.2.1.4 Rising demand for high-performance computing

- 3.2.1.5 Growing focus on energy efficiency and sustainability in data centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Complexity of maintenance and operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Cooling Solution Type, 2021 – 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Single-phase liquid cooling

- 5.3 Two-phase liquid cooling

Chapter 6 Market Estimates and Forecast, By Component Cooling, 2021 – 2034 (USD Mn)

- 6.1 Key trends

- 6.2 CPU cooling

- 6.3 GPU cooling

- 6.4 ASIC cooling

- 6.5 Memory cooling

- 6.6 Other component cooling

Chapter 7 Market Estimates and Forecast, By Liquid Coolant Type, 2021 – 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Water-based coolants

- 7.3 Dielectric fluids

- 7.4 Mineral oils

- 7.5 Engineered fluids

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Bn)

- 8.1 Key trends

- 8.2 Servers

- 8.3 Workstations

- 8.4 Edge computing devices

- 8.5 Supercomputers

- 8.6 Gaming PCs

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Bn)

- 9.1 Key trends

- 9.2 Data centers

- 9.3 High-performance computing (HPC)

- 9.4 Artificial intelligence/machine learning systems

- 9.5 Gaming and eSports

- 9.6 Telecommunications

- 9.7 Financial services

- 9.8 Healthcare and life sciences

- 9.9 Oil and gas

- 9.10 Automotive (for electric vehicle batteries)

- 9.11 Aerospace and defense

- 9.12 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 ANZ

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Asetek

- 11.2 Alfa Laval

- 11.3 Castrol

- 11.4 Cisco Systems, Inc.

- 11.5 CoolIT Systems

- 11.6 DCX The Liquid Cooling Company

- 11.7 Danfoss A/S

- 11.8 DUG Technology

- 11.9 Equinix, Inc.

- 11.10 Fujitsu Limited

- 11.11 Green Revolution Cooling (GRC)

- 11.12 Huawei Technologies Co., Ltd.

- 11.13 Iceotope Technologies Ltd.

- 11.14 Inspur Systems

- 11.15 LiquidCool Solutions

- 11.16 LiquidStack

- 11.17 Rittal GmbH & Co. KG

- 11.18 Schneider Electric

- 11.19 STULZ GmbH

- 11.20 Submer Technologies

- 11.21 Super Micro Computer, Inc.

- 11.22 Vertiv Group Corp.

- 11.23 ZutaCore

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日