|

市場調査レポート

商品コード

1699306

健康診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Health Check-up Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 健康診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月20日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

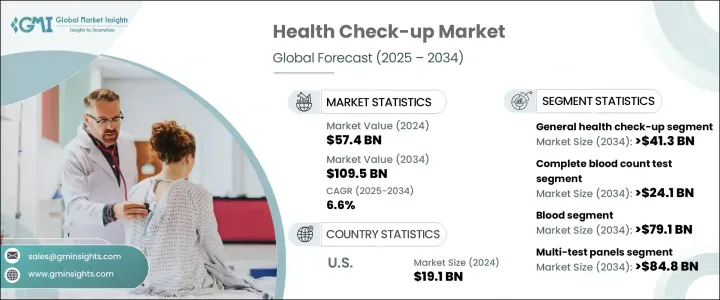

世界の健康診断市場は、2024年に574億米ドルと評価され、がん、糖尿病、心血管障害などの慢性疾患の有病率の増加により、2025年から2034年にかけてCAGR 6.6%で拡大すると予測されています。

予防医療を優先する個人が増えるにつれて、定期的な医療検診の需要は増加の一途をたどり、早期発見と治療成績の向上を確実なものにしています。診断技術の進歩により検診がより身近になったことで、ヘルスケアプロバイダーや保険会社は早期診断の重要性を強調し、市場の拡大をさらに後押ししています。

先を見越した健康管理への意識が高まるにつれ、定期検診は世界的にヘルスケア戦略の不可欠な一部となりつつあります。保険会社は保険プランに予防検診を組み込む傾向を強めており、個人に定期的な医療診断を受けるよう促しています。政府や民間ヘルスケア・プロバイダーも、予防検診を推進するための意識向上キャンペーンや健康プログラムを開始しています。在宅診断サービスの利便性、テレヘルスの普及拡大、AI主導の診断ツールの開発は、健康診断の状況を一変させ、検診をより効率的で広く利用できるものにしています。さらに、従業員の健康とウェルネス・プログラムを支援する雇用主の取り組みが増加し、定期的な健康診断への参加を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 574億米ドル |

| 予測金額 | 1,095億米ドル |

| CAGR | 6.6% |

市場はタイプ別に、一般健診、専門健診、予防健診、定期健診・ウェルネス健診に区分されます。このうち、一般健診分野は依然として市場成長の支配的な力を持っています。この分野はCAGR 6.5%で拡大し、2034年には413億米ドルに達すると予想されます。定期的な検診は病気の早期発見を可能にし、深刻な健康合併症のリスクを低減し、タイムリーな医療介入を促進します。現在、多くの健康保険プランに定期検診が含まれており、個人が総合的な健康を維持するために不可欠な評価を受けられるようになっています。

検査の種類別に見ると、健康診断市場は、全血球数検査、血糖値検査、腎機能検査、骨プロファイル検査、電解質検査、肝機能検査、脂質プロファイル検査、心臓バイオマーカー、ホルモン・ビタミン評価、腫瘍マーカー、その他の診断から構成されます。完全血球計数検査分野は市場拡大の主要因であり、CAGR 6.2%で成長し、2034年には241億米ドルに達すると予測されています。これらの検査は、赤血球数、白血球数、血小板レベルなどの血球組成に関する重要な洞察を提供し、ヘルスケア提供者が貧血、感染症、血液疾患などの状態を診断することを可能にします。ヘモグロビンとヘマトクリットの測定は栄養状態の評価にも役立ち、鉄欠乏症やその他の健康上の懸念の特定に役立ちます。

米国の健康診断市場は、2024年に191億米ドルと評価され、2025年から2034年にかけてCAGR 5.7%で成長すると予想されています。糖尿病、高血圧、心血管疾患などの慢性疾患の有病率の上昇が、頻繁な検診の必要性を高めています。さらに、高齢化により一貫した包括的な医学的評価が必要となり、予防ヘルスケア・サービスの需要がさらに高まっています。ヘルスケアプロバイダーや保険会社が早期介入を積極的に推進する中、米国では定期的な医療評価がますます一般的になりつつあります。先を見越した健康管理をめぐる意識が高まり続けていることから、健康診断市場は今後10年間にわたって持続的に拡大する見通しです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 人口スクリーニングへの投資の急増

- 有病率の増加

- 高齢人口の増加

- デジタル技術の採用増加

- 業界の潜在的リスク&課題

- 検診に伴う高コスト

- 低開発地域における認識と適切なインフラの欠如

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

- 健康診断パッケージの概要

- スタートアップのシナリオ

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場企業の競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 一般健康診断

- 定期健康診断

- 専門的健康診断

- 予防健診

第6章 市場推計・予測:検査タイプ別、2021年~2034年

- 主要動向

- 全血球数検査

- 血糖値検査

- 電解質検査

- 脂質プロファイル検査

- ホルモンとビタミン

- 腫瘍マーカー

- 肝機能検査

- 心臓バイオマーカー

- 腎機能検査

- 骨プロファイル検査

- その他の検査

第7章 市場推計・予測:サンプルタイプ別、2021年~2034年

- 主要動向

- 血液

- 尿

- 唾液

- その他のサンプルタイプ

第8章 市場推計・予測:パネルタイプ別、2021年~2034年

- 主要動向

- マルチ検査パネル

- 単一検査パネル

第9章 市場推計・予測:サービスプロバイダー別、2021年~2034年

- 主要動向

- 病院ベースの検査室

- 独立型検査室

- 外来診療センター

- 中央検査室

- その他のサービスプロバイダー

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ARUP Laboratories

- Cerba Healthcare

- eurofins

- Exact Sciences

- GRAIL

- INNOVA

- labcorp

- natera

- OPKO

- Q2 Solutions

- Quest Diagnostics

- Sonic Healthcare

- SYNLAB

- Trinity Biotech

- UNILABS

The Global Health Check-Up Market was valued at USD 57.4 billion in 2024 and is projected to expand at a CAGR of 6.6% from 2025 to 2034, driven by the increasing prevalence of chronic illnesses such as cancer, diabetes, and cardiovascular disorders. As more individuals prioritize preventive care, the demand for routine medical screenings continues to rise, ensuring early detection and improved treatment outcomes. With advancements in diagnostic technologies making screenings more accessible, healthcare providers and insurers are emphasizing the importance of early diagnosis, further propelling market expansion.

As the awareness of proactive health management gains traction, routine check-ups are becoming an integral part of healthcare strategies worldwide. Insurers are increasingly incorporating preventive screenings into coverage plans, encouraging individuals to undergo regular medical evaluations. Governments and private healthcare providers are also launching awareness campaigns and health programs to promote preventive screenings. The convenience of home-based diagnostic services, the growing penetration of telehealth, and the development of AI-driven diagnostic tools are transforming the health check-up landscape, making screenings more efficient and widely available. Additionally, increased employer initiatives supporting employee health and wellness programs are boosting participation in regular health assessments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $57.4 Billion |

| Forecast Value | $ 109.5 Billion |

| CAGR | 6.6% |

The market is segmented by type into general health check-ups, specialized health check-ups, preventive health check-ups, and routine and wellness health check-ups. Among these, the general health check-up segment remains a dominant force in market growth. This segment is expected to expand at a CAGR of 6.5%, reaching USD 41.3 billion by 2034. Routine medical screenings enable early disease detection, reducing the risk of severe health complications and facilitating timely medical interventions. Many health insurance plans now include regular check-ups, ensuring individuals receive essential evaluations to maintain their overall well-being.

Based on test type, the health check-up market comprises complete blood count tests, blood glucose tests, kidney function tests, bone profile tests, electrolyte tests, liver function tests, lipid profile tests, cardiac biomarkers, hormone and vitamin assessments, tumor markers, and other diagnostics. The complete blood count test segment is a key contributor to market expansion, projected to grow at a CAGR of 6.2% and reach USD 24.1 billion by 2034. These tests offer vital insights into blood cell composition, including red and white blood cell counts and platelet levels, enabling healthcare providers to diagnose conditions such as anemia, infections, and blood disorders. Hemoglobin and hematocrit measurements also help assess nutritional status, aiding in the identification of iron deficiency and other health concerns.

The US health check-up market, valued at USD 19.1 billion in 2024, is expected to grow at a CAGR of 5.7% between 2025 and 2034. The rising prevalence of chronic diseases such as diabetes, hypertension, and cardiovascular conditions is driving the need for frequent screenings. Additionally, the aging population requires consistent and comprehensive medical assessments, further fueling the demand for preventive healthcare services. With healthcare providers and insurers actively promoting early intervention, routine medical evaluations in the US are becoming increasingly common. As awareness surrounding proactive health management continues to grow, the health check-up market is poised for sustained expansion over the next decade.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging investments in population screening

- 3.2.1.2 Increasing prevalence of diseases

- 3.2.1.3 Rise in geriatric population

- 3.2.1.4 Increasing adoption of digital technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with screening

- 3.2.2.2 Lack of awareness and proper infrastructure in under-developed regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

- 3.12 Health check-up packages outline

- 3.13 Start-up scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 General health check-up

- 5.3 Routine and wellness health check-up

- 5.4 Specialized health check-up

- 5.5 Preventive health check-up

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Complete blood count test

- 6.3 Blood glucose test

- 6.4 Electrolyte test

- 6.5 Lipid profile test

- 6.6 Hormones & vitamins

- 6.7 Tumor markers

- 6.8 Liver function test

- 6.9 Cardiac biomarkers

- 6.10 Kidney function test

- 6.11 Bone profile test

- 6.12 Other test types

Chapter 7 Market Estimates and Forecast, By Sample Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood

- 7.3 Urine

- 7.4 Saliva

- 7.5 Other sample types

Chapter 8 Market Estimates and Forecast, By Panel Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Multi-test panels

- 8.3 Single-test panels

Chapter 9 Market Estimates and Forecast, By Service Provider, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital-based laboratories

- 9.3 Standalone laboratories

- 9.4 Ambulatory care centers

- 9.5 Central laboratories

- 9.6 Other service providers

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ARUP Laboratories

- 11.2 Cerba Healthcare

- 11.3 eurofins

- 11.4 Exact Sciences

- 11.5 GRAIL

- 11.6 INNOVA

- 11.7 labcorp

- 11.8 natera

- 11.9 OPKO

- 11.10 Q2 Solutions

- 11.11 Quest Diagnostics

- 11.12 Sonic Healthcare

- 11.13 SYNLAB

- 11.14 Trinity Biotech

- 11.15 UNILABS