据置型蓄電池の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

Stationary Battery Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 166 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699290

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

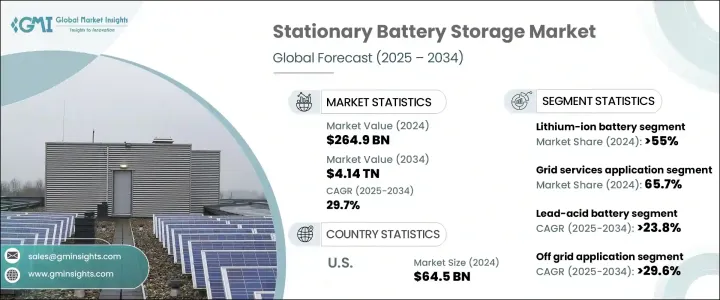

据置型蓄電池の世界市場は2024年に2,649億米ドルとなり、2025年から2034年にかけてCAGR29.7%で成長すると予測されています。

市場の急成長は、信頼性の高いグリッドサービスに対する需要の増加、リチウムイオン電池の普及、クリーンエネルギーソリューションと持続可能なインフラに対する世界の後押しが主な要因となっています。再生可能エネルギーの普及拡大に伴い、効率的なエネルギー貯蔵システムの必要性が高まる中、据置型蓄電池ソリューションは現代の送電網に不可欠な要素になりつつあります。政府と民間企業は、再生可能エネルギーインフラとエネルギー貯蔵技術に多額の投資を行っており、これが高度なバッテリー貯蔵ソリューションの採用を後押ししています。据置型バッテリーシステムは、安定したエネルギー供給を確保し、全体的な送電網の安定性を向上させるため、太陽光発電や風力発電設備と統合されつつあります。さらに、電気自動車(EV)の普及がバッテリー技術の進歩を加速させ、コストを下げ、エネルギー貯蔵を住宅用と商業用の両方でより身近なものにしています。

グリッドサービス分野は2024年に市場シェアの65.7%を占め、グリッドの安定性を維持し、エネルギー配給を最適化する上で重要な役割を担っていることが明らかになりました。再生可能エネルギーの導入が急増するにつれ、効果的なグリッドバランシングソリューションの必要性が高まり、据置型蓄電池システムは、生産量の多い時期に余剰エネルギーを貯蔵し、需要のピーク時に放電するために不可欠なものとなっています。アジア太平洋地域、特に中国とインドでは、よりクリーンなエネルギーミックスへのシフトが顕著であり、グリッド安定化技術の必要性がさらに高まっています。グリッドサービスは信頼性の高いエネルギー供給を確保する上で重要な役割を果たしており、据置型蓄電池の需要は大幅に増加すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2,649億米ドル |

| 予測金額 | 4兆1,400億米ドル |

| CAGR | 29.7% |

リチウムイオン電池分野は、エネルギー密度が高く、サイクル寿命が長く、コストが低下していることから、2034年までに1兆7,100億米ドルを生み出すと予測されています。リチウムイオン電池は、エネルギー貯蔵と放電の効率が高いため、据置型エネルギー貯蔵システムに適した選択肢になりつつあります。リチウムイオン電池は、系統安定化、エネルギー管理、再生可能エネルギー統合などの用途に広く導入されています。エネルギー容量とコスト削減の進歩が続く中、リチウムイオン電池は持続可能なエネルギーソリューションへの移行を促進する上で極めて重要な役割を果たしています。アジア太平洋は依然としてリチウムイオン電池製造の中心地であり、再生可能エネルギーとスマートグリッド技術への大規模な投資により、この地域はエネルギー貯蔵需要の増大に対応するための主要なプレーヤーとして位置づけられています。

米国の据置型蓄電池市場は2024年に645億米ドルとなり、予測期間中に最も高い成長率が見込まれています。この成長の原動力は、電気自動車需要の急増、再生可能エネルギーシステムの導入拡大、クリーンエネルギーへの取り組みを促進する政府の支援政策です。米国がクリーンエネルギーソリューションを採用し続ける中、据置型蓄電池市場は大幅に拡大する態勢にあり、信頼性が高く持続可能なエネルギーの未来が保証されます。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:バッテリー別、2021年~2034年

- 主要動向

- リチウムイオン

- LFP

- NMC

- その他

- 硫黄ナトリウム

- 鉛酸

- フロー電池

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- グリッドサービス

- BTM(Behind the meter)

- オフグリッド

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- BYD

- CATL

- Exide

- GS Yuasa

- Hitachi

- Johnson Controls

- Leclanche

- LG

- Panasonic

- Samsung

- Siemens

- SK Innovation

- Tesla

- Toshiba

- Varta

目次

The Global Stationary Battery Storage Market was valued at USD 264.9 billion in 2024 and is projected to grow at a CAGR of 29.7% from 2025 to 2034. The rapid growth in the market is primarily fueled by increasing demand for reliable grid services, the widespread adoption of lithium-ion batteries, and a global push toward clean energy solutions and sustainable infrastructure. As the need for efficient energy storage systems rises to support the growing penetration of renewable energy, stationary battery storage solutions are becoming an indispensable component of modern power grids. Governments and private sector players are making substantial investments in renewable energy infrastructure and energy storage technologies, which is propelling the adoption of advanced battery storage solutions. Stationary battery systems are being integrated with solar and wind energy installations to ensure a consistent energy supply and improve overall grid stability. Moreover, the growing prevalence of electric vehicles (EVs) is accelerating advancements in battery technologies, driving down costs and making energy storage more accessible for both residential and commercial applications.

The grid services segment accounted for 65.7% of the market share in 2024, underscoring its crucial role in maintaining grid stability and optimizing energy distribution. As the adoption of renewable energy surges, the need for effective grid balancing solutions has increased, making stationary battery storage systems essential for storing excess energy during high production periods and discharging it during peak demand. Countries in the Asia Pacific region, particularly China and India, are witnessing a significant shift toward a cleaner energy mix, further amplifying the need for grid stabilization technologies. With grid services playing a critical role in ensuring a reliable energy supply, the demand for stationary battery storage is expected to increase substantially.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $264.9 Billion |

| Forecast Value | $4.14 Trillion |

| CAGR | 29.7% |

The lithium-ion battery segment is projected to generate USD 1710 billion by 2034 due to its high energy density, long cycle life, and declining costs. Lithium-ion batteries are becoming the preferred choice for stationary energy storage systems, owing to their efficiency in energy storage and discharge. They are widely deployed in applications such as grid stabilization, energy management, and renewable energy integration. As advancements in energy capacity and cost reduction continue, lithium-ion batteries are playing a pivotal role in facilitating the transition toward sustainable energy solutions. Asia Pacific remains the hub for lithium-ion battery manufacturing, with extensive investments in renewable energy and smart grid technologies positioning the region as a key player in meeting the growing energy storage demands.

The U.S. stationary battery storage market was valued at USD 64.5 billion in 2024 and is expected to experience the highest growth rates during the forecast period. This growth is driven by surging demand for electric vehicles, increased adoption of renewable energy systems, and supportive government policies that promote clean energy initiatives. As the U.S. continues to embrace clean energy solutions, the stationary battery storage market is poised for substantial expansion, ensuring a reliable and sustainable energy future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Battery, 2021 – 2034 (USD Million, MW)

- 5.1 Key trends

- 5.2 Lithium ion

- 5.2.1 LFP

- 5.2.2 NMC

- 5.2.3 Others

- 5.3 Sodium sulphur

- 5.4 Lead acid

- 5.5 Flow battery

- 5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million, MW)

- 6.1 Key trends

- 6.2 Grid services

- 6.3 Behind the meter

- 6.4 Off grid

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 BYD

- 8.2 CATL

- 8.3 Exide

- 8.4 GS Yuasa

- 8.5 Hitachi

- 8.6 Johnson Controls

- 8.7 Leclanche

- 8.8 LG

- 8.9 Panasonic

- 8.10 Samsung

- 8.11 Siemens

- 8.12 SK Innovation

- 8.13 Tesla

- 8.14 Toshiba

- 8.15 Varta

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 166 Pages

- 納期

- 2~3営業日