|

市場調査レポート

商品コード

1699281

関節内補充療法市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Viscosupplementation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 関節内補充療法市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月19日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

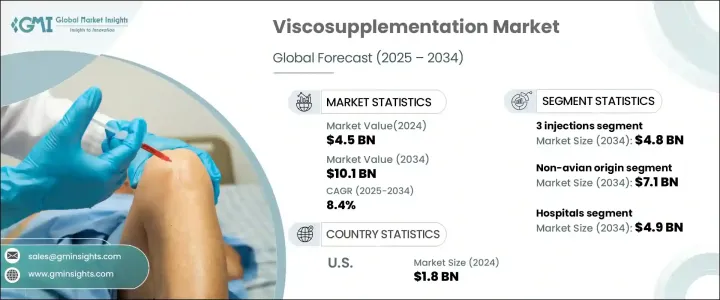

関節内補充療法の世界市場は、2024年に45億米ドルに達し、2025年から2034年にかけてCAGR 8.4%で成長すると予測されています。

変形性関節症、特に変形性膝関節症の有病率の上昇は、高度な治療ソリューションに対する需要を引き続き促進しています。非外科的介入として、関節内補充療法は関節の可動性を改善し、痛みを和らげ、侵襲的処置の必要性を遅らせる能力があるとして、広く認知されるようになっています。高齢者は関節の変性や変形性関節症関連の合併症にかかりやすいため、高齢化により市場は急速に拡大しています。

変形性関節症の症例が世界的に急増する中、ヘルスケア提供者も患者も同様に、長期的な症状管理のために関節内補充療法を利用するようになってきています。この治療法では、患部の関節にヒアルロン酸を注入し、潤滑性を回復させ、こわばりを軽減し、可動性を高める。この治療法は、回復に要する時間が短く、鎮痛剤への依存度が低いため、患者に好まれています。一方、製剤技術や製品純度の進歩が続いており、多様な患者グループでの採用が拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 45億米ドル |

| 予測金額 | 101億米ドル |

| CAGR | 8.4% |

効能が拡大し、生体適合性が向上した次世代ビスコサプリメントの導入が、市場の成長をさらに後押ししています。メーカー各社は、製品の性能を高めるために継続的に技術革新を行っており、関節内補充療法が変形性関節症管理に望ましい選択肢であり続けることを確実にしています。さらに、政府の支援策、ヘルスケア支出の増加、非外科的治療の選択肢に対する意識の高まりが、市場の軌道を加速させています。

関節内補充療法市場は、製品タイプ別に単回注射、3回注射、5回注射に区分されます。このうち、3回注射のセグメントは2024年の売上高が21億米ドルで市場を独占し、2034年にはCAGR 8.5%を記録して48億米ドルに達すると予測されています。変形性関節症の症状管理や関節機能の回復に有効なことから、標準的な治療法となっています。この治療法は、構造化された投与スケジュールにより、頻繁な受診の必要性を最小限に抑えながら持続的な症状緩和をもたらすため、医師から支持されています。投与の簡便さ、バランスのとれた治療期間、一貫した臨床成績により、この分野の人気は高まり続けています。

供給源別では、市場は鳥類由来と非鳥類由来の粘液サプリメントに分類され、非鳥類由来製品が2024年の市場シェアの71.6%を占める。この分野は、アレルギー反応に対する懸念の高まり、倫理的配慮、製品の一貫性向上などを背景に、2034年には71億米ドルに達すると予測されています。原生生物由来でないビスコサプリメントは純度が高く、免疫反応のリスクが低いため、患者にもヘルスケアプロバイダーにもますます好まれるようになっています。メーカーがアレルゲンフリーの高純度製剤の開発に注力しているため、合成および生物工学的な代替品への移行が市場をさらに形成しています。

北米の関節内補充療法市場は、2024年に18億米ドルに達しました。研究によると、関節炎は依然として最も一般的な関節障害であり、数百万人が罹患しています。調査によると、65歳以上の43%が変形性関節症に罹患しており、その主な原因は軟骨の変性、関節の劣化、回復力の低下です。効果的で低侵襲な解決策への需要が高まる中、関節内補充療法は変形性関節症治療における重要な治療選択肢としての地位を固め続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 変形性関節症に罹患しやすい高齢者人口の増加

- 低侵襲治療に対する需要の高まり

- 技術の進歩

- スポーツ関連傷害の増加

- 業界の潜在的リスク&課題

- 高い治療費

- 代替治療の利用可能性

- 促進要因

- 成長可能性分析

- 規制状況

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 単回注射

- 3回注射

- 5回注射

第6章 市場推計・予測:由来別、2021年~2034年

- 主要動向

- 鳥類由来

- 非鳥類由来

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 整形外科クリニック

- 外来手術センター(ASCs)

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Anika Therapeutics

- APTISSEN

- Avanos

- Biotech Healthcare

- Bioventus

- Ferring Pharmaceuticals

- Fidia Pharma

- Premier Surgical

- Sanofi

- Seikagaku Corporation

- Stellar Pharmaceuticals

- TRB Pharma

- Zimmer Biomet

The Global Viscosupplementation Market reached USD 4.5 billion in 2024 and is projected to grow at a CAGR of 8.4% from 2025 to 2034. The rising prevalence of osteoarthritis, particularly knee osteoarthritis, continues to drive the demand for advanced treatment solutions. As a non-surgical intervention, viscosupplementation is gaining widespread recognition for its ability to improve joint mobility, alleviate pain, and delay the need for invasive procedures. The market is witnessing rapid expansion due to the aging population, as older individuals are more susceptible to joint degeneration and osteoarthritis-related complications.

With osteoarthritis cases surging globally, healthcare providers and patients alike are increasingly turning to viscosupplementation for long-term symptom management. The procedure involves injecting hyaluronic acid into the affected joints to restore lubrication, reduce stiffness, and enhance mobility. Patients prefer this treatment for its minimal recovery time and reduced dependence on pain medication. Meanwhile, ongoing advancements in formulation technologies and product purity are expanding adoption across diverse patient groups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 8.4% |

The introduction of next-generation viscosupplements with extended efficacy and improved biocompatibility is further fueling market growth. Manufacturers are continuously innovating to enhance product performance, ensuring that viscosupplementation remains a preferred choice for osteoarthritis management. Additionally, supportive government initiatives, rising healthcare expenditure, and increasing awareness about non-surgical treatment alternatives are accelerating the market's trajectory.

The viscosupplementation market is segmented by product type into single injection, three injections, and five injections. Among these, the three-injection segment dominated the market with USD 2.1 billion in revenue in 2024 and is expected to reach USD 4.8 billion by 2034, registering a CAGR of 8.5%. Its effectiveness in managing osteoarthritis symptoms and restoring joint function has made it the standard treatment approach. Physicians favor this regimen due to its structured dosing schedule, which provides sustained symptom relief while minimizing the need for frequent medical visits. The segment's popularity continues to rise due to its ease of administration, balanced treatment duration, and consistent clinical outcomes.

By source, the market is categorized into avian-origin and non-avian-origin viscosupplements, with non-avian-origin products accounting for 71.6% of the market share in 2024. This segment is projected to reach USD 7.1 billion by 2034, driven by growing concerns over allergic reactions, ethical considerations, and improved product consistency. Non-avian-origin viscosupplements offer enhanced purity and a lower risk of immune response, making them increasingly preferred by both patients and healthcare providers. The transition toward synthetic and bioengineered alternatives is further shaping the market as manufacturers focus on developing allergen-free, high-purity formulations.

North America viscosupplementation market reached USD 1.8 billion in 2024, as osteoarthritis cases continue to rise across the region. Studies indicate that arthritis remains the most common joint disorder, affecting millions of individuals, with osteoarthritis being the leading cause of disability among aging populations. Research shows that 43% of individuals aged 65 and above suffer from osteoarthritis, primarily due to cartilage degeneration, joint deterioration, and reduced resilience. As demand for effective, minimally invasive solutions grows, viscosupplementation continues to cement its position as a key treatment option in osteoarthritis care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population prone to osteoarthritis

- 3.2.1.2 Rising demand for minimally invasive treatments

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increasing sport-related injuries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Availability of alternative treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single injection

- 5.3 3 injections

- 5.4 5 injections

Chapter 6 Market Estimates and Forecast, By Source of Origin, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Avian origin

- 6.3 Non-avian origin

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anika Therapeutics

- 9.2 APTISSEN

- 9.3 Avanos

- 9.4 Biotech Healthcare

- 9.5 Bioventus

- 9.6 Ferring Pharmaceuticals

- 9.7 Fidia Pharma

- 9.8 Premier Surgical

- 9.9 Sanofi

- 9.10 Seikagaku Corporation

- 9.11 Stellar Pharmaceuticals

- 9.12 TRB Pharma

- 9.13 Zimmer Biomet