|

市場調査レポート

商品コード

1699275

真空遮断器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Vacuum Circuit Breaker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 真空遮断器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

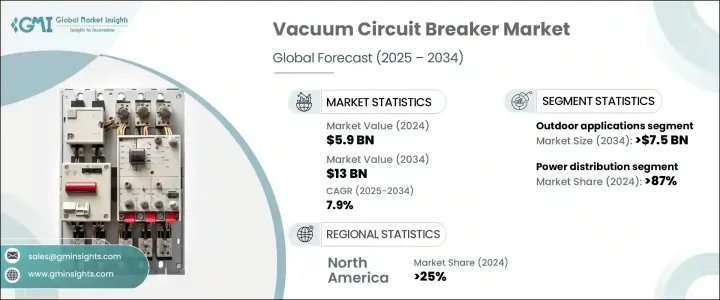

真空遮断器の世界市場規模は2024年に59億米ドルとなり、2025年から2034年にかけてCAGR 7.9%で拡大すると予測されています。

この成長には、公益事業、産業、商業の各分野で信頼性が高く効率的な配電に対する需要が高まっていることが背景にあります。再生可能エネルギー、スマートグリッド、デジタル変電所の採用が増加していることが、市場拡大を加速しています。真空遮断器は、従来のサーキットブレーカに比べて高い動作効率、優れた消弧能力、低メンテナンスを提供します。現在進行中の電化イニシアチブとトランスミッションおよび配電インフラの近代化が需要をさらに押し上げています。

業界各社は、機器の信頼性と性能を高めるため、リアルタイム監視、IoT接続、予知保全の統合に注力しています。急速な工業化と大規模なインフラプロジェクトにより、インドと中国が主導するアジア太平洋地域が市場を独占しています。しかし、真空遮断器を既存のグリッドシステムに統合するには、主に初期投資コストに起因する課題があります。しかし、技術の進歩、エネルギー効率の高いプロジェクトに対する政府の優遇措置、スマート電力システムへのシフトが、こうした障害を軽減するのに役立っています。持続可能なエネルギー・ソリューションを促進する規制措置も、市場の成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 59億米ドル |

| 予測金額 | 130億米ドル |

| CAGR | 7.9% |

屋外用真空遮断器分野は、2034年までに75億米ドルを超えると予想されています。これらのブレーカーは送電・配電ネットワークで広く使用され、グリッドの信頼性と回復力を確保しています。屋外設置の拡大は、農村部の電化、送電網の近代化、再生可能エネルギープロジェクトの展開の増加によって推進されています。過酷な環境条件下でも機能するように設計されたこれらのブレーカは、変電所や大規模な再生可能発電所で重要な役割を果たしています。耐候性材料とスマートグリッドインターフェイス技術の開発により、耐久性と効率がさらに向上しています。公益事業者はネットワークの安定性を優先しており、屋外用真空遮断器の安定した需要を支えています。

屋内用真空遮断器は、メンテナンスの必要性が低く、環境に優しい設計であるため、商業用および産業用アプリケーションで人気を集めています。スマートビルやデジタル変電所の普及により、自動予知保全、遠隔監視、運転安全性の強化が可能な屋内ブレーカの採用が増加しています。さらに、過酷な環境条件にさらされるのを最小限に抑え、機器の経年劣化を抑えるため、産業界は屋内設置を好んでいます。屋内と屋外の両セグメントは拡大を続けているが、どちらを好むかはエンドユーザーの特定の運用要件や環境要件によって異なります。

配電は、2024年には87%以上を占める圧倒的な市場シェアを占めており、さらなる成長が見込まれています。電力需要の増加とスマートグリッドやデジタル変電所の進歩が相まって、この分野での真空遮断器の採用が進んでいます。これらのブレーカは、産業、商業施設、集合住宅の高圧スイッチギヤに広く組み込まれています。真空遮断器は効率的なアーク消火機能、メンテナンスの軽減、環境面のメリットを提供するため、送電網の近代化に向けた政府や電力会社の投資が市場の拡大をさらに後押ししています。

米国市場は大きく成長し、2022年には9億米ドル、2023年には10億米ドル、2024年には11億米ドルに達します。SF6フリー・ソリューションへの移行と、信頼性の高い中高圧配電機器への需要の高まりが、この拡大に寄与している主な要因です。産業施設、データセンター、EV充電インフラの増加が市場需要をさらに押し上げ、真空遮断器は最新の電気ネットワークに不可欠なコンポーネントとして位置づけられています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:定格電流別、2021年~2034年

- 主要動向

- 500 A

- 500~1,500 A

- 1,500~2,500 A

- 2,500~4,500 A

- 4,500 A超

第6章 市場規模・予測:設置別、2021年~2034年

- 主要動向

- 屋内

- 屋外

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 配電

- 送電

第8章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業

- 産業

- ユーティリティ

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- ドイツ

- イタリア

- 英国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- ABB

- Eaton Corporation

- General Electric

- HD Hyundai Electric &Energy System

- Kirloskar Electric

- LS Electric

- Mitsubishi Electric Corporation

- Powell Industries

- Schneider Electric

- Siemens Energy

- Toshiba International Corporation

- WEG

The Global Vacuum Circuit Breaker Market was valued at USD 5.9 billion in 2024 and is projected to expand at a CAGR of 7.9% from 2025 to 2034. This growth is fueled by the rising demand for reliable and efficient power distribution across utility, industrial, and commercial sectors. The increasing adoption of renewable energy, smart grids, and digital substations is accelerating the market expansion. Vacuum circuit breakers offer higher operational efficiency, superior arc-extinguishing capabilities, and lower maintenance compared to traditional circuit breakers. The ongoing electrification initiatives and modernization of transmission and distribution infrastructure further boost demand.

Industry players are focusing on integrating real-time monitoring, IoT connectivity, and predictive maintenance to enhance equipment reliability and performance. The Asia-Pacific region, led by India and China, dominates the market due to rapid industrialization and large-scale infrastructure projects. However, the integration of vacuum circuit breakers into existing grid systems presents challenges, primarily due to initial investment costs. Despite this, advancements in technology, government incentives for energy-efficient projects, and the shift toward smart power systems help mitigate these obstacles. Regulatory measures promoting sustainable energy solutions are also driving market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.9 Billion |

| Forecast Value | $13 Billion |

| CAGR | 7.9% |

The outdoor vacuum circuit breaker segment is expected to surpass USD 7.5 billion by 2034. These breakers are widely used in power transmission and distribution networks, ensuring grid reliability and resilience. The expansion of outdoor installations is driven by rural electrification, grid modernization, and the increasing deployment of renewable energy projects. Engineered to function under extreme environmental conditions, these breakers play a crucial role in substations and large-scale renewable power plants. The development of weather-resistant materials and smart grid interfacing technologies has further enhanced their durability and efficiency. Utilities prioritize network stability, supporting steady demand for outdoor vacuum circuit breakers.

Indoor vacuum circuit breakers are gaining popularity in commercial and industrial applications due to their low maintenance requirements and environmentally friendly design. The proliferation of smart buildings and digital substations is increasing the adoption of indoor breakers, which enable automated predictive maintenance, remote supervision, and enhanced operational safety. Additionally, industries prefer indoor installations to minimize exposure to harsh environmental conditions, reducing equipment degradation over time. While both indoor and outdoor segments continue to expand, the preference depends on the specific operational and environmental requirements of end users.

Power distribution holds a dominant market share, accounting for over 87% in 2024, and is expected to see further growth. The rising demand for electricity, combined with advancements in smart grids and digital substations, is driving the adoption of vacuum circuit breakers in this segment. These breakers are widely integrated into medium-voltage switchgear for industries, commercial establishments, and residential complexes. Government and utility investments in grid modernization further support market expansion, as vacuum circuit breakers offer efficient arc-extinguishing capabilities, reduced maintenance, and environmental benefits.

The U.S. market witnessed significant growth, reaching USD 0.9 billion in 2022, USD 1 billion in 2023, and USD 1.1 billion in 2024. The transition toward SF6-free solutions and the rising demand for reliable medium-voltage power distribution equipment are key factors contributing to this expansion. The increasing number of industrial facilities, data centers, and EV charging infrastructure further fuels market demand, positioning vacuum circuit breakers as essential components in modern electrical networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Rated Current, 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 500 A

- 5.3 500 to 1,500 A

- 5.4 1,500 to 2,500 A

- 5.5 2,500 to 4,500 A

- 5.6 > 4,500 A

Chapter 6 Market Size and Forecast, By Installation, 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Indoor

- 6.3 Outdoor

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 Power distribution

- 7.3 Power transmission

Chapter 8 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.5 Utility

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 France

- 9.3.2 Germany

- 9.3.3 Italy

- 9.3.4 UK

- 9.3.5 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Kuwait

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Eaton Corporation

- 10.3 General Electric

- 10.4 HD Hyundai Electric & Energy System

- 10.5 Kirloskar Electric

- 10.6 LS Electric

- 10.7 Mitsubishi Electric Corporation

- 10.8 Powell Industries

- 10.9 Schneider Electric

- 10.10 Siemens Energy

- 10.11 Toshiba International Corporation

- 10.12 WEG