|

市場調査レポート

商品コード

1699266

迅速インフルエンザ診断検査市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Rapid Influenza Diagnostic Tests (RIDT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 迅速インフルエンザ診断検査市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

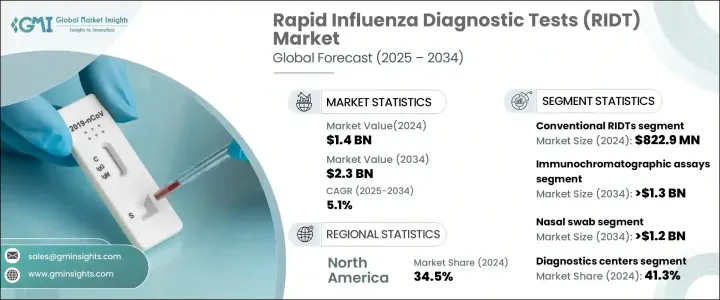

世界の迅速インフルエンザ診断検査市場は、2024年に14億米ドルに達し、2025年から2034年にかけてCAGR 5.1%で成長すると予測されています。

季節性インフルエンザの流行の増加、ポイントオブケア検査の進歩、診断方法の継続的な革新が市場の成長を促進しています。世界各国の政府はインフルエンザのサーベイランスを強化し、啓発キャンペーンを実施しており、RIDTの採用をさらに拡大しています。技術の進歩は検査精度を大幅に向上させ、デジタルRIDTは感度と特異度を高めています。

定性的RIDTから半定量的RIDTへの移行は臨床的妥当性を高め、複数の呼吸器病原体を検出できる多重化検査は一般的になりつつあります。人工知能(AI)と機械学習は検査解釈を最適化し、エラーを減らし、診断をより身近なものにしています。ヘルスケア・インフラへの投資の拡大も、こうした検査の可用性を向上させています。規制機関は、合理化された承認や公衆衛生イニシアチブへの財政支援を通じて、迅速なインフルエンザ診断を支援しています。診断検査への資金援助が増加することで、一般市民の意識が高まり、早期発見・早期治療が促進され、市場が前進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 23億米ドル |

| CAGR | 5.1% |

RIDTs市場は、製品タイプ、技術、サンプルタイプ、最終用途、地域によって区分されます。従来型RIDTsセグメントは2024年に8億2,290万米ドルを創出しました。これらの検査は、手頃な価格で入手しやすいため、特にヘルスケアインフラが限られている地域で広く使用されています。シンプルなデザインで製造コストが低いため、公衆衛生プログラムでの使用に理想的であり、幅広い利用が可能です。使いやすく、必要なトレーニングも最小限であるため、診療所、職場、学校など、さまざまな環境で実施することができます。迅速な結果は迅速な意思決定を可能にし、季節性インフルエンザの流行管理に非常に効果的です。

技術別では、イムノクロマトアッセイがCAGR 5.9%の予測で市場成長をリードし、2034年までに13億米ドル以上に達すると予想されています。これらの検査は感度と特異性が高く、小児や高齢者といった脆弱な集団におけるインフルエンザの検出に特に有用です。イムノクロマトアッセイの需要は、薬局や急患センターなど、分散化したヘルスケア環境において増加しています。イムノクロマトアッセイはコンパクトな設計で、必要な機器も最小限であるため、このような場所での使用に適しています。継続的な技術の進歩により、スピードと精度がさらに向上し、ヘルスケア専門家の間で好まれる選択肢となっています。

サンプルタイプ別では、鼻腔スワブ分野はCAGR 5.9%で成長し、2034年までに12億米ドルを超えると予測されています。鼻腔スワブは、適用が簡単でインフルエンザの検出精度が高いため、広く使用されています。他のサンプル採取法よりも侵襲性が低いため、小児から成人まで適しています。高いウイルス量を捕らえることができるため、インフルエンザの早期診断に有効であり、ポイントオブケアとラボ検査の両方の環境でヘルスケアプロバイダーに利益をもたらしています。

診断センターは、2024年に41.3%と最も高い最終用途の売上シェアを占めました。これらの施設は高度な診断技術を提供し、訓練を受けた専門家を雇用することで、正確で効率的な検査を実現しています。複数の呼吸器感染症に対するマルチプレックス検査など、総合的な診断サービスに対する需要の高まりが、診断センターにおけるRIDTへの依存度を高める一因となっています。これらの施設は大規模なインフルエンザ・モニタリング・プログラムで重要な役割を果たしており、市場の優位性を強めています。

北米は、確立されたヘルスケアシステム、迅速検査キットの普及、ポイント・オブ・ケア検査の採用増加により、2024年には34.5%の最大市場シェアを獲得しました。米国市場は2021年に3億3,100万米ドル、2022年に3億6,580万米ドル、2023年に4億130万米ドルとなり、同地域での優位性を反映しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- インフルエンザの流行拡大

- 技術の進歩

- インフルエンザの早期診断と管理に対する需要の高まり

- 迅速診断検査の普及

- 業界の潜在的リスク&課題

- 熟練した専門家の不足

- 厳しい規制

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 価格分析

- ギャップ分析

- ポーター分析

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 従来型RIDT

- デジタルRIDT

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- イムノクロマトアッセイ

- ラテラルフローアッセイ

- PCR法

- その他のテクノロジー

第7章 市場推計・予測:サンプルタイプ別、2021年~2034年

- 主要動向

- 鼻腔スワブ

- 咽頭スワブ

- その他のサンプルタイプ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 診断センター

- 病院

- 研究ラボ

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 3B BlackBio

- Abbott

- Access Bio

- BD

- bioMérieux

- CHEMBIO

- DiaSorin

- Meridian

- Quidel Corporation

- Roche

- SEKISUI

- Siemens HEALTHINEERS

- Thermo Fisher

The Global Rapid Influenza Diagnostic Tests Market reached USD 1.4 billion in 2024 and is projected to grow at a CAGR of 5.1% from 2025 to 2034. The rising prevalence of seasonal flu, advancements in point-of-care testing, and continuous innovations in diagnostic methods are driving market growth. Governments worldwide are strengthening influenza surveillance and running awareness campaigns, further expanding the adoption of RIDTs. Technological advancements have significantly improved test accuracy, with digital RIDTs offering enhanced sensitivity and specificity.

The shift from qualitative to semi-quantitative RIDTs has increased their clinical relevance, and multiplexed tests capable of detecting multiple respiratory pathogens are becoming more common. Artificial intelligence (AI) and machine learning are optimizing test interpretation, reducing errors, and making diagnostics more accessible. Growing investments in healthcare infrastructure are also improving the availability of these tests. Regulatory bodies are supporting rapid influenza diagnosis through streamlined approvals and financial support for public health initiatives. Increased funding for diagnostic testing is helping expand public awareness, encouraging early detection and treatment, and driving the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.1% |

The RIDTs market is segmented based on product type, technology, sample type, end-use, and region. The conventional RIDTs segment generated USD 822.9 million in 2024. These tests remain widely used due to their affordability and ease of access, particularly in regions with limited healthcare infrastructure. Their simple design and low production cost make them ideal for use in public health programs, ensuring broad availability. The ease of use and minimal training requirements allow these tests to be implemented in a variety of settings, including clinics, workplaces, and schools. Fast results enable quick decision-making, making them highly effective in managing seasonal flu outbreaks.

By technology, immunochromatographic assays are expected to lead market growth with a projected CAGR of 5.9%, reaching over USD 1.3 billion by 2034. These tests offer high sensitivity and specificity, making them particularly valuable for detecting influenza in vulnerable populations, such as children and the elderly. The demand for immunochromatographic assays is increasing in decentralized healthcare settings, including pharmacies and urgent care centers. Their compact design and minimal equipment requirements make them well-suited for such locations. Continued technological advancements have further improved their speed and accuracy, making them a preferred choice among healthcare professionals.

Based on sample type, the nasal swab segment is projected to grow at a CAGR of 5.9%, surpassing USD 1.2 billion by 2034. Nasal swabs are widely used due to their ease of application and high accuracy in detecting influenza. They are less invasive than other sample collection methods, making them suitable for both children and adults. Their ability to capture high viral loads makes them effective in early influenza diagnosis, benefiting healthcare providers in both point-of-care and laboratory testing environments.

Diagnostic centers accounted for the highest end-use revenue share of 41.3% in 2024. These facilities offer advanced diagnostic technologies and employ trained professionals, ensuring accurate and efficient testing. The increasing demand for comprehensive diagnostic services, including multiplex testing for multiple respiratory infections, has contributed to the growing reliance on RIDTs in diagnostic centers. These facilities play a crucial role in large-scale influenza monitoring programs, reinforcing their market dominance.

North America captured the largest market share of 34.5% in 2024, driven by a well-established healthcare system, the widespread availability of rapid test kits, and the increasing adoption of point-of-care testing. The US market was valued at USD 331 million in 2021, rising to USD 365.8 million in 2022 and USD 401.3 million in 2023, reflecting its dominant position within the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of influenza

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising demand for early influenza diagnosis and management

- 3.2.1.4 Increasing popularity of rapid diagnostic tests

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Stringent regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pricing analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional RIDTs

- 5.3 Digital RIDTs

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunochromatographic assays

- 6.3 Lateral flow assays

- 6.4 PCR

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Sample Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Nasal swab

- 7.3 Throat swab

- 7.4 Other sample types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostic centers

- 8.3 Hospitals

- 8.4 Research laboratories

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3B BlackBio

- 10.2 Abbott

- 10.3 Access Bio

- 10.4 BD

- 10.5 bioMérieux

- 10.6 CHEMBIO

- 10.7 DiaSorin

- 10.8 Meridian

- 10.9 Quidel Corporation

- 10.10 Roche

- 10.11 SEKISUI

- 10.12 Siemens HEALTHINEERS

- 10.13 Thermo Fisher