触覚センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Tactile Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699246

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

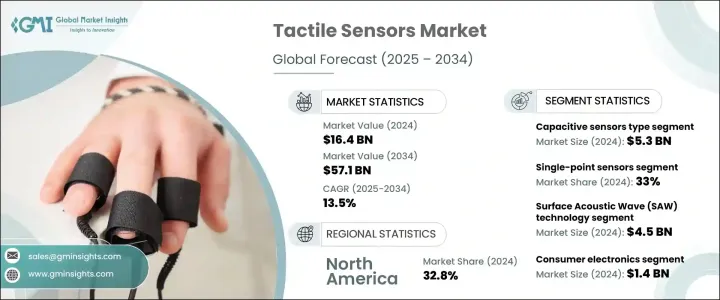

世界の触覚センサー市場は、2024年に164億米ドルと評価され、2025年から2034年にかけてCAGR 13.5%で拡大すると予測されています。

この成長の原動力となっているのは、民生用電子機器の採用が増加していること、自動車分野で触覚センサーの使用が増加していること、自動化やロボット工学への傾斜が強まっていることです。人間の触覚を再現するように設計されたこれらのセンサーは、機能性と効率性を向上させ、複数の産業で支持を集めています。ユーザー・インタフェースを改善し、よりスマートでインタラクティブなシステムを実現する役割が需要を促進しています。人工知能、機械学習、IoT技術の普及は、特にハイテク産業での採用をさらに加速しています。さらに、センサーの精度、感度、耐久性の継続的な進歩は、医療機器、産業オートメーション、防衛分野での幅広い応用を可能にしています。AIを搭載した触覚センサーをスマートデバイスや自律システムに統合することが重要なトレンドになりつつあり、企業は性能と効率を高めるために高度なセンサー技術への投資を促しています。

タイプ別では、静電容量式センサーが2024年に53億米ドルを占める。抵抗センサーや誘導センサーに比べて精度が高く、寿命が長く、感度が高いことが普及に寄与しています。また、ピンチ・ツー・ズームなどの機能を備えたマルチタッチ・インターフェイスに対する需要の高まりも、同分野の拡大を後押ししています。民生用電子機器が洗練されたタッチセンサー機能で進化を続ける中、静電容量式センサーは引き続きメーカーに選ばれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 164億米ドル |

| 予測金額 | 571億米ドル |

| CAGR | 13.5% |

製品セグメントには、統合センサー、アレイセンサー、シングルポイントセンサー、ハイブリッドセンサーが含まれます。2024年には、シングルポイントセンサーセグメントが世界市場の33%のシェアを占める。正確な力と圧力の検出が可能なため、産業オートメーション、ロボット工学、ウェアラブル技術に不可欠となっています。これらのセンサーの需要は、産業界が支援技術からスマートウェアラブルに至るまで、より高度なタッチセンシティブ・ソリューションを求めるにつれて高まっています。

市場は技術別に表面弾性波(SAW)、電気活性ポリマー(EAP)、微小電気機械システム(MEMS)、その他に区分されます。SAW技術は2024年に45億米ドルで市場をリード。コスト効率に優れ、コンパクトで高効率なセンサー部品へのニーズの高まりが、特に5GやIoT技術の台頭とともに、その採用を後押ししています。小型化された電子機器やモバイル機器は、SAWベースのセンサーを搭載することが増えており、成長をさらに後押ししています。

用途別では、民生用電子機器、自動車、ヘルスケア、産業用オートメーション、航空宇宙、その他に広がっています。スマートフォンやタブレットの普及、高度な触覚フィードバック技術に牽引され、2024年には民生用電子機器が14億米ドルで優位を占める。触覚センサーは、タッチをシミュレートすることでユーザー体験を向上させ、最新の電子機器に不可欠なものとなっています。

地域別では、北米が2024年の市場収益シェアの32.8%を占め、研究開発への多額の投資と厳しい産業オートメーション安全規制に支えられています。米国市場だけでも35億米ドルと評価され、ロボット工学、医療用ウェアラブル、義肢装具技術の進歩に起因する旺盛な需要があります。大手センサーメーカーの存在は、技術革新と製品開発をさらに促進しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 民生用電子機器の採用増加

- 自動車産業における触覚センサーの利用拡大

- 自動化とロボット工学への傾斜の高まり

- 技術開発の増加

- 業界の潜在的リスク&課題

- 設計とテストに伴う複雑さ

- 消費電力に関する懸念の高まり

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 静電容量式センサー

- 抵抗センサー

- 圧電センサー

- 光センサー

- その他

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- シングルポイントセンサー

- アレイセンサー

- 統合型センサー

- ハイブリッドセンサー

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 表面弾性波(SAW)

- 電気活性ポリマー(EAP)

- 微小電気機械システム(MEMS)

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 家電

- 自動車

- ヘルスケア・医療機器

- ロボット

- 産業オートメーション

- 航空宇宙・防衛

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airmar Technology Corporation

- Analog Devices, Inc.

- Bosch Sensortec GmbH

- Cypress Semiconductor Corporation

- Honeywell International Inc.

- Infineon Technologies AG

- Melexis NV

- Microchip Technology Inc.

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors

- Omron Corporation

- Panasonic Corporation

- Pepperl+Fuchs SE

- Renesas Electronics Corporation

- STMicroelectronics

- TE Connectivity Ltd.

- Texas Instruments Incorporated

目次

The Global Tactile Sensors Market was valued at USD 16.4 billion in 2024 and is projected to expand at a CAGR of 13.5% from 2025 to 2034. This growth is driven by the increasing adoption of consumer electronic devices, the rising use of tactile sensors in the automotive sector, and the growing inclination toward automation and robotics. These sensors, designed to replicate the human sense of touch, are gaining traction across multiple industries, enhancing functionality and efficiency. Their role in improving user interfaces and enabling smarter, more interactive systems is fueling demand. The expanding footprint of artificial intelligence, machine learning, and IoT technologies is further accelerating adoption, particularly in high-tech industries. Additionally, ongoing advancements in sensor accuracy, sensitivity, and durability are enabling broader applications in medical devices, industrial automation, and defense sectors. The integration of AI-powered tactile sensors into smart devices and autonomous systems is becoming a key trend, prompting companies to invest in advanced sensor technologies to enhance performance and efficiency.

Based on type, capacitive sensors accounted for USD 5.3 billion in 2024. Their superior accuracy, longer lifespan, and higher sensitivity compared to resistive and inductive sensors have contributed to their widespread use. The increasing demand for multi-touch interfaces with functions such as pinch-to-zoom is also supporting segment expansion. As consumer electronics continue to evolve with sophisticated touch-sensitive features, capacitive sensors remain a preferred choice for manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.4 billion |

| Forecast Value | $57.1 billion |

| CAGR | 13.5% |

The product segment includes integrated sensors, array sensors, single-point sensors, and hybrid sensors. In 2024, the single-point sensors segment held a 33% share of the global market. Their ability to provide precise force and pressure detection has made them essential in industrial automation, robotics, and wearable technologies. Demand for these sensors is rising as industries seek more advanced touch-sensitive solutions in applications ranging from assistive technologies to smart wearables.

The market is segmented by technology into Surface Acoustic Wave (SAW), Electroactive Polymers (EAP), Micro-electromechanical Systems (MEMS), and others. SAW technology led the market with USD 4.5 billion in 2024. The growing need for cost-effective, compact, and highly efficient sensor components has driven its adoption, particularly with the rise of 5G and IoT technologies. Miniaturized electronics and mobile devices are increasingly incorporating SAW-based sensors, further propelling growth.

Application-wise, the market spans consumer electronics, automotive, healthcare, industrial automation, aerospace, and others. Consumer electronics dominated with USD 1.4 billion in 2024, driven by the widespread adoption of smartphones, tablets, and advanced haptic feedback technologies. Tactile sensors enhance user experience by simulating touch, making them integral to modern electronic devices.

Regionally, North America accounted for 32.8% of the market's revenue share in 2024, supported by substantial investments in R&D and stringent industrial automation safety regulations. The U.S. market alone was valued at USD 3.5 billion, with strong demand stemming from advancements in robotics, medical wearables, and prosthetic technologies. The presence of leading sensor manufacturers is further fostering innovation and product development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing adoption of consumer electronic devices

- 3.6.1.2 Emerging use of tactile sensors in automotive industry

- 3.6.1.3 Rising inclination towards automation and robotics

- 3.6.1.4 Increasing technological developments

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Complexities associated with designing and testing

- 3.6.2.2 Growing concerns regarding power consumption

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Capacitive sensors

- 5.3 Resistive sensors

- 5.4 Piezoelectric sensors

- 5.5 Optical sensors

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Single-point sensors

- 6.3 Array sensors

- 6.4 Integrated sensors

- 6.5 Hybrid sensors

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Surface Acoustic Wave (SAW)

- 7.3 Electroactive Polymers (EAP)

- 7.4 Micro-electromechanical Systems (MEMS)

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Healthcare & medical devices

- 8.5 Robotics

- 8.6 Industrial automation

- 8.7 Aerospace & defense

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airmar Technology Corporation

- 10.2 Analog Devices, Inc.

- 10.3 Bosch Sensortec GmbH

- 10.4 Cypress Semiconductor Corporation

- 10.5 Honeywell International Inc.

- 10.6 Infineon Technologies AG

- 10.7 Melexis NV

- 10.8 Microchip Technology Inc.

- 10.9 Murata Manufacturing Co., Ltd.

- 10.10 NXP Semiconductors

- 10.11 Omron Corporation

- 10.12 Panasonic Corporation

- 10.13 Pepperl+Fuchs SE

- 10.14 Renesas Electronics Corporation

- 10.15 STMicroelectronics

- 10.16 TE Connectivity Ltd.

- 10.17 Texas Instruments Incorporated

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日