コンピュータマイクロチップ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Computer Microchips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699243

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

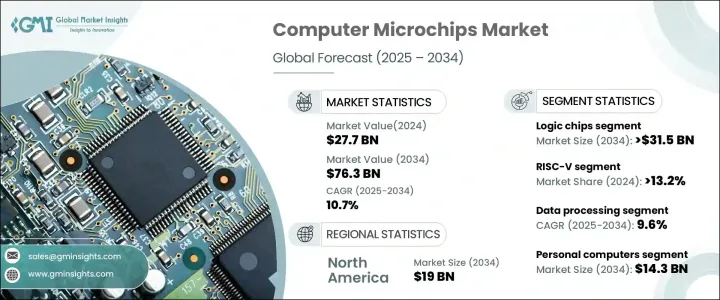

コンピュータマイクロチップの世界市場は2024年に277億米ドルとなり、2025年から2034年にかけてCAGR 10.7%で拡大すると予測されています。

人工知能、機械学習、クラウドコンピューティングの採用が増加しており、高性能で低消費電力のマイクロチップの需要が高まっています。企業や消費者のデジタルトランスフォーメーションへの依存度が高まる中、先進的なプロセッサ、メモリチップ、ネットワークコンポーネントのニーズは高まり続けています。企業は、AI主導のアプリケーション、データ集約型のワークロード、クラウドベースの運用をサポートするため、スケーラブルでエネルギー効率の高いチップに注目しています。データセンター・インフラの拡大も、電力効率を最適化し運用コストを削減するために企業が先進的なマイクロチップに投資することで市場の成長を加速させています。半導体製造の革新とAIに最適化されたチップの台頭が業界の進化を形成しています。

メーカー各社は、AIやクラウドコンピューティング用途に合わせた高性能・低消費電力チップを優先しています。AIワークロードには、ディープラーニング、ニューラルネットワーク、ビッグデータ分析用に設計された専用プロセッサが必要です。より高速で効率的なコンピューティングが重視されるようになり、マイクロチップアーキテクチャの革新が進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 277億米ドル |

| 予測金額 | 763億米ドル |

| CAGR | 10.7% |

チップタイプ別では、メモリチップ、ロジックチップ、SoC、ASICに区分されます。ロジックチップ分野は、半導体技術の進歩、5GやIoTの利用拡大により、大幅な拡大が見込まれます。ロジックチップ市場は、スマートフォン、タブレット、ノートパソコン、ゲーム機器の需要増が成長に寄与し、2034年には315億米ドルを超えると予測されています。複数の処理機能を1つのユニットに統合したシステムオンチップ(SoC)アーキテクチャは、モバイル機器やウェアラブル機器の性能を高めています。

アーキテクチャ別の市場セグメンテーションには、x86、ARM、RISC-V、その他が含まれます。RISC-Vセグメントは、オープンソースのフレームワーク、柔軟性、コストメリットにより急成長を遂げています。2024年には、RISC-Vが市場の13.2%以上を占める。RISC-Vはオープンソースであるため、企業はライセンシング費用をかけずにカスタムチップ設計を開発でき、大幅なコスト削減とベンダー依存の回避を実現できます。

アプリケーション別では、データ処理、グラフィックス・レンダリング、AI・機械学習、ネットワーキング、センサー統合、暗号化、セキュリティに分類されます。データ処理分野は、2034年までにCAGR 9.6%で成長すると予測されています。AIベースの分析、ビッグデータ、クラウドコンピューティング、高性能コンピューティングに対する需要の拡大が、大規模な計算ワークロードを処理できる高度なチップの要件を押し上げています。

最終用途のセグメンテーションには、パーソナルコンピュータ、サーバーとデータセンター、スマートフォンとタブレット、ゲーム機、その他が含まれます。パーソナルコンピュータ分野は、リモートワーク、オンライン教育、デジタルコンテンツ制作の需要増に牽引され、2034年には143億米ドルに達すると予測されています。AIを搭載したノートPCやARMベースのプロセッサの採用が拡大しており、PC業界の形を変えつつあります。

地域別では、北米は2034年までに190億米ドルに達すると予測され、強力な研究開発投資、先進的な半導体サプライチェーン、AIとクラウドベースの技術に対する需要の高まりから恩恵を受けています。米国だけでも、国内半導体生産を拡大し、外部サプライチェーンへの依存を減らす政府のイニシアティブに支えられ、167億米ドルに達すると予想されています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- AIと機械学習の進歩

- 家電製品の成長

- クラウドコンピューティングとデータセンターの拡大

- 半導体需要の増加

- 電気自動車(EV)と自律走行車の増加

- 業界の潜在的リスク&課題

- 世界半導体サプライチェーンの混乱

- 複雑化と製造コストの上昇

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:チップタイプ別、2021年~2034年

- 主要動向

- ロジックチップ

- メモリーチップ

- ASICチップ

- SoCチップ

第6章 市場推計・予測:アーキテクチャ別、2021年~2034年

- 主要動向

- x86

- ARM

- RISC-V

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- データ処理

- グラフィックスレンダリング

- 人工知能と機械学習

- ネットワーキングとコネクティビティ

- センサー統合

- 暗号化とセキュリティ

- その他

第8章 市場推計・予測:エンドユーザー別、2021年~2034年

- 主要動向

- パーソナルコンピュータ

- サーバー、データセンター

- スマートフォン、タブレット

- ゲーム機

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Micro Devices

- Analog Devices

- Arm Holdings

- Broadcom

- Espressif Systems

- Infineon Technologies

- Intel

- Kioxia Holdings

- Marvell Technology Group

- Microchip Technology

- Micron Technology

- NVIDIA

- NXP Semiconductors

- Qualcomm

- Renesas Electronics

- Samsung Electronics

- STMicroelectronics

- Taiwan Semiconductor Manufacturing Company

- Texas Instruments

目次

The Global Computer Microchips Market was valued at USD 27.7 billion in 2024 and is projected to expand at a CAGR of 10.7% from 2025 to 2034. Increasing adoption of artificial intelligence, machine learning, and cloud computing is fueling demand for high-performance, low-power microchips. With businesses and consumers increasingly relying on digital transformation, the need for advanced processors, memory chips, and networking components continues to rise. Companies are focusing on scalable and energy-efficient chips to support AI-driven applications, data-intensive workloads, and cloud-based operations. Expanding data center infrastructure is also accelerating the market's growth as firms invest in advanced microchips to optimize power efficiency and reduce operational costs. Innovations in semiconductor manufacturing and the rise of AI-optimized chips are shaping the industry's evolution.

Manufacturers are prioritizing high-performance, low-power chips tailored for AI and cloud computing applications. AI workloads require specialized processors designed for deep learning, neural networks, and big data analytics. The growing emphasis on faster, more efficient computing is driving innovation in microchip architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.7 Billion |

| Forecast Value | $76.3 Billion |

| CAGR | 10.7% |

By chip type, the market is segmented into memory chips, logic chips, SoCs, and ASICs. The logic chips segment is expected to witness substantial expansion, driven by advancements in semiconductor technology and the increasing use of 5G and IoT. The market for logic chips is projected to exceed USD 31.5 billion by 2034, with rising demand for smartphones, tablets, laptops, and gaming devices contributing to its growth. System-on-chip (SoC) architectures that integrate multiple processing functions into a single unit are enhancing the performance of mobile and wearable devices.

Market segmentation by architecture includes x86, ARM, RISC-V, and others. The RISC-V segment is experiencing rapid growth due to its open-source framework, flexibility, and cost benefits. In 2024, RISC-V accounted for over 13.2% of the market. Its open-source nature allows companies to develop custom chip designs without licensing fees, offering significant cost savings and avoiding vendor dependency.

By application, the market is categorized into data processing, graphics rendering, AI and machine learning, networking, sensor integration, encryption, and security. The data processing segment is forecasted to grow at a CAGR of 9.6% by 2034. Expanding demand for AI-based analytics, big data, cloud computing, and high-performance computing is boosting the requirement for sophisticated chips that can handle large-scale computational workloads.

The end-use segmentation includes personal computers, servers and data centers, smartphones and tablets, gaming consoles, and others. The personal computers segment is expected to reach USD 14.3 billion by 2034, driven by increasing demand for remote work, online education, and digital content creation. The growing adoption of AI-powered laptops and ARM-based processors is reshaping the PC industry.

Regionally, North America is forecasted to reach USD 19 billion by 2034, benefiting from strong R&D investments, an advanced semiconductor supply chain, and rising demand for AI and cloud-based technologies. The U.S. market alone is expected to hit USD 16.7 billion, supported by government initiatives to expand domestic semiconductor production and reduce reliance on external supply chains.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in AI and machine learning

- 3.2.1.2 Growth in consumer electronics

- 3.2.1.3 Expansion of cloud computing and data centres

- 3.2.1.4 Increasing demand for semiconductors

- 3.2.1.5 Rise in electric vehicles (EVs) and autonomous cars

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Global semiconductor supply chain disruptions

- 3.2.2.2 Rising complexity and manufacturing costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Chip Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Logic chips

- 5.3 Memory chips

- 5.4 ASICs

- 5.5 SoCs

Chapter 6 Market Estimates and Forecast, By Architecture, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 x86

- 6.3 ARM

- 6.4 RISC-V

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Data processing

- 7.3 Graphics rendering

- 7.4 Artificial intelligence and machine learning

- 7.5 Networking and connectivity

- 7.6 Sensor integration

- 7.7 Encryption and security

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-use, 2021– 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Personal computers

- 8.3 Servers and data centers

- 8.4 Smartphones and tablets

- 8.5 Gaming consoles

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Micro Devices

- 10.2 Analog Devices

- 10.3 Arm Holdings

- 10.4 Broadcom

- 10.5 Espressif Systems

- 10.6 Infineon Technologies

- 10.7 Intel

- 10.8 Kioxia Holdings

- 10.9 Marvell Technology Group

- 10.10 Microchip Technology

- 10.11 Micron Technology

- 10.12 NVIDIA

- 10.13 NXP Semiconductors

- 10.14 Qualcomm

- 10.15 Renesas Electronics

- 10.16 Samsung Electronics

- 10.17 STMicroelectronics

- 10.18 Taiwan Semiconductor Manufacturing Company

- 10.19 Texas Instruments

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日