|

市場調査レポート

商品コード

1698595

太陽電池市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Solar Cells Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 太陽電池市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月14日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

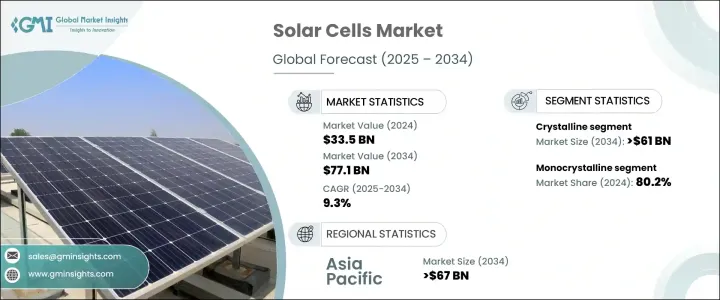

世界の太陽電池市場は2024年に335億米ドルとなり、2025年から2034年にかけてCAGR 9.3%で成長すると予測されています。

同市場は、技術の進歩、生産コストの低下、再生可能エネルギーソリューションに対する意識の高まりによって牽引力を増しています。太陽電池効率の革新と太陽エネルギー・システムの普及が、業界を再構築しています。政府の支援政策、ネットメータリング優遇措置、再生可能エネルギー義務化は、拡大を加速させています。製造コストの低下と競合の激化が、効率的な太陽光発電ソリューションの開発をさらに促進しています。遠隔地におけるオフグリッド太陽光発電アプリケーションの採用増加や、太陽光発電と蓄電池システムの統合も、市場の需要を促進しています。さらに、住宅用太陽光発電システムの設置が増加していることも、業界の足跡を拡大する上で重要な役割を果たしています。

結晶系太陽電池分野は、費用対効果と優れた効率に牽引され、2034年までに610億米ドルを超えると予想されています。単結晶技術は定評があり、効率20%を超える高性能ソーラーパネルを提供しています。パッシベーション型エミッター・リアセル(PERC)、ヘテロ接合技術(HJT)、N型シリコンなどの先進技術の導入により、効率レベルはさらに向上し、ソーラー・ソリューションは多様な用途でより現実的なものとなっています。2024年に太陽電池市場の80.2%を占める単結晶パネルの採用が拡大しているのは、その信頼性と性能向上の証です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 335億米ドル |

| 予測金額 | 771億米ドル |

| CAGR | 9.3% |

セル技術の進歩により、太陽エネルギー利用が最適化され、エネルギー変換率が向上し、電子再結合損失が減少しています。結晶系太陽電池、特に単結晶系太陽電池は、その耐久性と優れたエネルギー出力により、引き続き市場を独占しています。多結晶、CdTe、アモルファスシリコン(A-Si)、セレン化銅インジウムガリウム(CIGS)技術も進化しており、住宅、商業、工業の各分野における太陽電池用途の拡大に貢献しています。

米国の太陽電池市場は、2022年に8億4,000万米ドル、2023年に8億8,000万米ドル、2024年に9億1,000万米ドルを記録しました。成長の原動力となっているのは、太陽光発電所の設置が増加し、再生可能エネルギーへの取り組みが拡大していることです。同国は大規模な太陽光発電プロジェクトに力を入れており、国の政策も後押ししているため、公共施設、住宅、商業施設での導入が進んでいます。

アジア太平洋地域の太陽電池市場は、政府の強力なインセンティブと高効率太陽電池技術への投資増に支えられ、2034年までに670億米ドルを超えると予測されています。新興国における急速な都市化と工業化が、信頼性が高く持続可能なエネルギー源に対する需要を高めています。農村電化プログラムの拡大や、風力と蓄電池を統合したハイブリッド・ソーラー・プロジェクトの市場開拓が、市場の成長をさらに後押ししています。東南アジアの国々は太陽光発電設備の急増を目の当たりにしており、同地域を世界の太陽光発電市場の主要貢献地域として位置付けています。

各国がエネルギーの自立と持続可能性の目標達成に向けて取り組む中、太陽エネルギーの採用は加速すると予想されます。太陽光発電技術の進歩が進み、政策的支援も増えていることから、市場は今後数年で大きく拡大する構えです。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 基本推定と計算

- 予測モデル

- 1次調査と検証

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションとテクノロジーの展望

第5章 市場規模・予測:材料別、2021年~2034年

- 主要動向

- 結晶性

- N材料

- P材料

- 薄膜

第6章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 単結晶

- 多結晶

- テルル化カドミウム(CDTE)

- アモルファスシリコン(A-Si)

- 二セレン化銅インジウムガリウム(CIGS)

第7章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- BSF

- PERC/PERL/PERT/トップコン

- HJT

- IBC &MWT

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- 欧州

- ドイツ

- スペイン

- フランス

- オランダ

- アジア太平洋

- 中国

- マレーシア

- 韓国

- 日本

- 台湾

- インド

- 世界のその他の地域

第9章 企業プロファイル

- Canadian Solar

- DuPont

- Hevel

- Hanwha Q Cells

- Jinko Solar

- JINERGY

- JA SOLAR Technology

- Meyer Burger

- MOTECH Industries

- RENESOLA

- REC Solar Holdings

- Silfab Solar

- Singulus Technologies

- SunPower Corporation

- Sunport Power

- AIKO

- Tongwei

- United Renewable Energy

- Vikram Solar

- Wuxi Suntech Power

- Yingli Solar

The Global Solar Cells Market was valued at USD 33.5 billion in 2024 and is projected to grow at a CAGR of 9.3% from 2025 to 2034. The market is gaining traction due to advancements in technology, declining production costs, and increasing awareness of renewable energy solutions. Innovations in solar cell efficiency and the widespread adoption of solar energy systems are reshaping the industry. Supportive government policies, net metering incentives, and renewable energy mandates are accelerating expansion. Lower manufacturing expenses and growing competition are further fostering the development of efficient solar power solutions. The rising adoption of off-grid solar applications in remote regions and the integration of solar power with battery storage systems are also fueling market demand. Additionally, increasing installations of residential solar power systems are playing a crucial role in expanding the industry's footprint.

The crystalline solar cells segment is anticipated to surpass USD 61 billion by 2034, driven by cost-effectiveness and superior efficiency. Monocrystalline technology is well-established, offering high-performance solar panels with efficiency rates exceeding 20%. The introduction of advanced technologies such as Passivated Emitter and Rear Cell (PERC), heterojunction technology (HJT), and N-type silicon has further enhanced efficiency levels, making solar solutions more viable for diverse applications. The growing adoption of monocrystalline panels, which accounted for 80.2% of the solar cells market in 2024, is a testament to their reliability and improved performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $33.5 Billion |

| Forecast Value | $77.1 Billion |

| CAGR | 9.3% |

Advancements in cell technology are optimizing solar energy utilization, improving energy conversion rates, and reducing electron recombination losses. Crystalline solar cells, particularly monocrystalline variants, continue to dominate the market due to their durability and superior energy output. Polycrystalline, CdTe, amorphous silicon (A-Si), and copper indium gallium selenide (CIGS) technologies are also evolving, contributing to the expansion of solar applications across residential, commercial, and industrial sectors.

The US solar cells market recorded values of USD 840 million in 2022, USD 880 million in 2023, and USD 910 million in 2024. The growth is fueled by increasing installations of solar power plants and expanding renewable energy initiatives. The country's focus on large-scale solar projects and supportive state policies is driving adoption across utility-scale, residential, and commercial installations.

The Asia Pacific solar cells market is projected to exceed USD 67 billion by 2034, supported by strong government incentives and rising investments in high-efficiency solar technology. Rapid urbanization and industrialization in emerging economies are increasing the demand for reliable and sustainable energy sources. The expansion of rural electrification programs and the development of hybrid solar projects integrating wind and battery storage are further bolstering market growth. Countries across Southeast Asia are witnessing a surge in solar installations, positioning the region as a key contributor to the global solar market.

The adoption of solar energy is expected to accelerate as nations work toward achieving energy independence and sustainability goals. With ongoing advancements in solar technology and increasing policy support, the market is poised for significant expansion in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Material, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Crystalline

- 5.2.1 N Material

- 5.2.2 P Material

- 5.3 Thin Film

Chapter 6 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Monocrystalline

- 6.3 Polycrystalline

- 6.4 Cadmium Telluride (CDTE)

- 6.5 Amorphous Silicon (A-Si)

- 6.6 Copper Indium Gallium Diselenide (CIGS)

Chapter 7 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 BSF

- 7.3 PERC/PERL/PERT/TOPCON

- 7.4 HJT

- 7.5 IBC & MWT

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 Spain

- 8.3.3 France

- 8.3.4 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Malaysia

- 8.4.3 South Korea

- 8.4.4 Japan

- 8.4.5 Taiwan

- 8.4.6 India

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Canadian Solar

- 9.2 DuPont

- 9.3 Hevel

- 9.4 Hanwha Q Cells

- 9.5 Jinko Solar

- 9.6 JINERGY

- 9.7 JA SOLAR Technology

- 9.8 Meyer Burger

- 9.9 MOTECH Industries

- 9.10 RENESOLA

- 9.11 REC Solar Holdings

- 9.12 Silfab Solar

- 9.13 Singulus Technologies

- 9.14 SunPower Corporation

- 9.15 Sunport Power

- 9.16 AIKO

- 9.17 Tongwei

- 9.18 United Renewable Energy

- 9.19 Vikram Solar

- 9.20 Wuxi Suntech Power

- 9.21 Yingli Solar