X線検出器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

X-ray Detectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698594

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

X線検出器の世界市場は、2024年には40億米ドルと評価され、2025年から2034年にかけてCAGR 6%で拡大すると予測されています。

X線放射を電子信号や視覚信号に変換するこれらの検出器は、特に医療や歯科分野など、さまざまな画像処理アプリケーションで重要な役割を果たしています。慢性疾患の増加により、疾病の早期発見に対する需要が高まっていることが、市場拡大に拍車をかけています。がんは依然として世界の主要死因の1つであり、高度なスクリーニングや診断ソリューションの必要性が高まっています。ヘルスケアシステムが早期診断と画像精度の向上を重視していることから、X線検出器の採用は増加すると予想されます。

技術の進歩によってX線検出の効率は大幅に向上し、画質の向上と診断の迅速化につながっています。フィルムベースからデジタルX線検出器への移行が加速し、医療現場での迅速な画像撮影とワークフローの合理化が可能になりました。スピードと正確さで知られるダイレクトデジタルX線撮影(DR)システムが普及しつつあります。軽量でワイヤレスな検出器の統合により、空間分解能の向上と放射線被曝の低減を実現し、市場は進化を続けています。検出器技術の革新が、今後数年間の業界成長を牽引すると期待されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 40億米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 6% |

検出器タイプ別では、フラットパネル検出器(FPD)、コンピューテッドラジオグラフィ(CR)検出器、電荷結合素子検出器などがあります。2023年の市場売上高は38億米ドルで、FPD分野が優位を占め、2024年には20億米ドルの貢献となります。FPDは、高画質、高速処理、フィルムベースのイメージングを排除する能力で支持され、ヘルスケア施設の効率を向上させています。デジタルX線撮影や透視アプリケーションでの採用が増加しており、市場成長を加速しています。直接変換とワイヤレス接続の継続的な強化により、業界での地位はさらに強化され、医療画像診断の専門家に好まれる選択肢となっています。

市場は医療用、歯科用、その他の用途に分類され、2024年の売上シェアは医療用が46.9%を占める。この分野は、筋骨格系疾患と慢性呼吸器疾患の有病率の増加に牽引され、2034年までに34億米ドルの売上が見込まれています。骨や関節に影響を及ぼす疾患の増加により、正確な診断と治療計画のためにX線画像診断への依存度が高まっています。また、呼吸器疾患では頻繁な撮影が必要となるため、先進的なX線検出器ソリューションの需要が高まっています。

病院は依然として主要なエンドユーザーであり、2024年の売上シェアは34.5%です。病院の患者数の多さと高度な画像処理インフラが市場の優位性を支えています。デジタルX線撮影システムの統合はワークフローの効率を高め、X線検出器の普及を支えています。病院が画像診断の需要増に対応するために放射線科の拡張を続けているため、先進画像技術に対する政府投資の増加が市場成長をさらに後押ししています。

米国では、2023年の市場収益は15億3,000万米ドルで、2034年には63億米ドルに達すると予測されています。慢性疾患の罹患率の上昇と高額なヘルスケア支出が、医療施設におけるX線検出器の広範な採用を支えています。早期診断に対する意識の高まりが引き続き需要を牽引しており、米国は世界市場拡大の主要貢献国となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 疾患の早期診断に対する需要の高まり

- 技術の進歩

- X線技術の利点に対する意識の高まり

- 有利な償還シナリオ

- 業界の潜在的リスク&課題

- X線検出器のコスト高

- 厳しい規制シナリオ

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:検出器タイプ別、2021年~2034年

- 主要動向

- フラットパネル検出器(FPD)

- コンピューテッドラジオグラフィー(CR)検出器

- 電荷結合素子検出器

- その他の検出器タイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 医療用途

- 歯科用途

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診断研究所

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Agfa-Gevaert Group

- Canon Medical Systems

- Carestream Health

- Fujifilm

- General Electric Company

- Konica Minolta

- Koninklijke Philips

- PerkinElmer

- Siemens Healthineers

- Teledyne Technologies

- Thales Group

- Toshiba

- Varex Imaging

目次

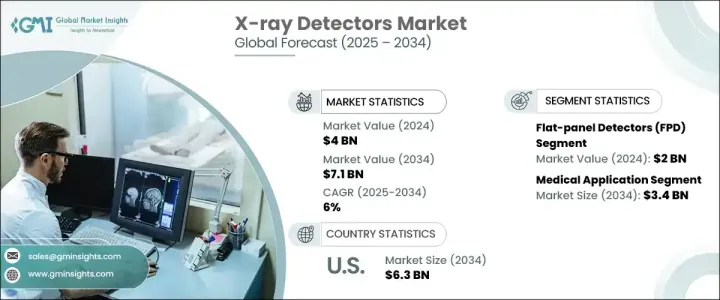

The Global X-Ray Detectors Market was valued at USD 4 billion in 2024 and is projected to expand at a CAGR of 6% from 2025 to 2034. These detectors, which convert X-ray radiation into electronic or visual signals, play a critical role in various imaging applications, particularly in the medical and dental fields. The rising demand for early disease detection, driven by the growing prevalence of chronic illnesses, is fueling market expansion. Cancer remains one of the leading causes of death worldwide, increasing the need for advanced screening and diagnostic solutions. The adoption of X-ray detectors is expected to rise as healthcare systems emphasize early diagnosis and improved imaging accuracy.

Technological advancements have significantly enhanced the efficiency of X-ray detection, leading to improved image quality and faster diagnosis. The transition from film-based to digital X-ray detectors has accelerated, enabling quicker image capture and streamlined workflow in medical settings. Direct digital radiography (DR) systems, known for their speed and accuracy, are gaining traction. The market continues to evolve with the integration of lightweight and wireless detectors, offering better spatial resolution and reduced radiation exposure. Innovations in detector technology are expected to drive industry growth in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6% |

By detector type, the market includes flat-panel detectors (FPD), computed radiography (CR) detectors, and charge-coupled device detectors, among others. In 2023, market revenue stood at USD 3.8 billion, with the FPD segment dominating, contributing USD 2 billion in 2024. FPDs are favored for their high image quality, rapid processing speed, and ability to eliminate film-based imaging, improving efficiency in healthcare facilities. Their increasing adoption in digital radiography and fluoroscopy applications is accelerating market growth. Continuous enhancements in direct conversion and wireless connectivity further strengthen their position in the industry, making them the preferred choice for medical imaging professionals.

The market is categorized into medical, dental, and other applications, with the medical segment accounting for 46.9% of revenue share in 2024. This segment is expected to generate USD 3.4 billion by 2034, driven by the increasing prevalence of musculoskeletal disorders and chronic respiratory diseases. A rise in conditions affecting bones and joints has led to greater reliance on X-ray imaging for accurate diagnosis and treatment planning. Additionally, respiratory illnesses necessitate frequent imaging, reinforcing the demand for advanced X-ray detector solutions.

Hospitals remain the leading end users, capturing a 34.5% revenue share in 2024. The high patient volume and sophisticated imaging infrastructure in hospitals contribute to their dominant market position. The integration of digital radiography systems enhances workflow efficiency, supporting the widespread adoption of X-ray detectors. Increased government investment in advanced imaging technologies further propels market growth, as hospitals continue to expand radiology departments to meet the growing demand for diagnostic imaging.

In the U.S., market revenue was USD 1.53 billion in 2023 and is projected to reach USD 6.3 billion by 2034. The rising incidence of chronic diseases and high healthcare expenditure support the extensive adoption of X-ray detectors across medical facilities. Increased awareness of early diagnosis continues to drive demand, positioning the U.S. as a key contributor to global market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.3 Methodology and Scope

- 1.3.1 Research approach

- 1.3.2 Data collection methods

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Forecast model

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.6.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for early disease diagnosis

- 3.2.1.2 Technological advancement

- 3.2.1.3 Increased awareness about the benefits of X-ray technology

- 3.2.1.4 Favorable reimbursement scenario

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with X-ray detectors

- 3.2.2.2 Stringent regulatory scenario

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Detector Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flat-panel detectors (FPD)

- 5.3 Computed radiography (CR) detectors

- 5.4 Charge coupled device detectors

- 5.5 Other detector types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Medical application

- 6.3 Dental application

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Agfa-Gevaert Group

- 9.2 Canon Medical Systems

- 9.3 Carestream Health

- 9.4 Fujifilm

- 9.5 General Electric Company

- 9.6 Konica Minolta

- 9.7 Koninklijke Philips

- 9.8 PerkinElmer

- 9.9 Siemens Healthineers

- 9.10 Teledyne Technologies

- 9.11 Thales Group

- 9.12 Toshiba

- 9.13 Varex Imaging

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日