衛星レーザー通信市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Satellite Laser Communication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698562

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

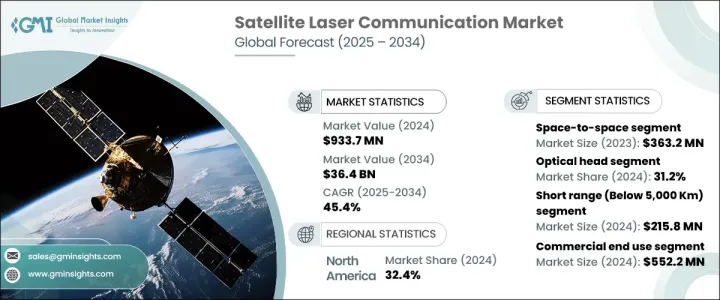

衛星レーザー通信の世界市場は、2024年に9億3,370万米ドルと評価され、2025年から2034年にかけてCAGR 45.4%で急増すると予測されています。

この成長の背景には、高速データトランスミッション、帯域幅の向上、複雑なファイバーシステムへの広範な展開に対する需要の高まりがあります。キャリア周波数が進化するにつれて変調技術が向上し、効率的なポイント・ツー・ポイント・トランスミッションのデータ伝送容量が増大します。世界中の企業は、生産性を高め、顧客サービスを向上させるために、高速で信頼性の高い接続性を優先しており、高速データ伝送の需要を促進しています。衛星レーザー通信は、信号損失を最小限に抑え、シームレスな伝送を保証しながら、優れたデータレートを実現します。この技術は、無線周波数システムよりも高い帯域幅を提供し、重量、体積、電力が少なくて済むため、衛星コンステレーションや宇宙探査に理想的です。地球低軌道(LEO)衛星の増加に伴い、衛星レーザー通信の採用は拡大し続けています。企業は、データの信頼性とトランスミッション効率を最適化するため、高度な変調技術に投資しています。

市場は、ソリューションによって宇宙-宇宙、宇宙-地上局、宇宙-その他のアプリケーションに区分されます。宇宙-宇宙通信は、2023年に3億6,320万米ドルで、高速衛星間データ転送をサポートし、リアルタイム接続を強化します。2022年に1億9,600万米ドルとなる宇宙-地上局間セグメントは、科学研究、世界ブロードバンド、気象予報サービスのための効率的なデータトランスミッションを可能にします。2021年に4,650万米ドルだった宇宙-その他アプリケーションには、深宇宙探査や惑星ミッションが含まれ、最小レイテンシで長距離光通信が必要。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億3,370万米ドル |

| 予測金額 | 364億米ドル |

| CAGR | 45.4% |

市場はまた、光ヘッド、モデム、レーザレシーバとトランスミッタ、変調器などのコンポーネント別に分類されます。オプティカルヘッドセグメントは、2024年に市場の31.2%を占めると予測されており、高度な光学系を使用した正確なレーザビームトランスミッションに不可欠です。市場の24.8%を占めると予測されているレーザレシーバとトランスミッタは、安全で高速なデータ交換を保証します。20.4%のシェアを占めるモデムは、デジタルデータを光信号に変換してシームレス伝送を実現し、市場の17.2%を占める変調器は、スペクトル効率とデータスループットを高める。

通信距離別には、短距離通信、中距離通信、長距離通信があります。短距離通信は2024年に2億1,580万米ドルで、地球観測用LEO衛星リンクとリアルタイムブロードバンドネットワークをカバーします。中距離通信は2023年に1億2,330万米ドルで、異なる軌道の衛星を接続します。2022年に3億2,590万米ドルとなる長距離セグメントは、深宇宙ミッションや惑星間探査をサポートします。

最終用途には、商業、政府、軍事が含まれます。2024年に5億5,220万米ドルで最大となる商業セグメントは、世界のブロードバンドとデータ中継サービスの需要増加により拡大しています。政府部門は、2024年に2億80万米ドルで、気候モニタリング、災害管理、安全なデータ交換にレーザ通信を活用しています。軍事分野は、2025年から2034年にかけてCAGR 46.7%の成長が見込まれており、防衛や監視活動のために安全な高速通信に投資しています。

北米は2024年に32.4%のシェアを占め、市場を独占しています。これは通信インフラへの大規模な投資が原動力となっています。米国市場は、2024年に2億5,580万米ドルと評価され、衛星ベースの通信システムに対する政府と民間部門の強力な投資により、急速に進展しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 高速データトランスミッションの需要増加

- 宇宙探査と衛星コンステレーション

- 宇宙ベースのサービス採用の増加

- レーザー通信技術の進歩

- 政府のイニシアティブと投資

- 業界の潜在的リスク&課題

- 高い開発・展開コスト

- 宇宙用コンポーネントの入手が困難

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- 宇宙ステーション間

- 宇宙-地上局間

- 宇宙対その他のアプリケーション

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 光ヘッド

- レーザーレシーバー・トランスミッター

- モデム

- 変調器

- その他

第7章 市場推計・予測:レンジ別、2021年~2034年

- 主要動向

- 短距離(5,000Km未満)

- 中距離(5,000~35,000Km)

- 長距離(35,000Km以上)

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 商業

- 官公庁

- 軍用

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airbus SE

- Axelspace Corporation

- Ball Aerospace &Technologies Corp.

- Blue Canyon Technologies LLC

- BridgeComm, Inc.

- EnduroSat AD

- General Atomics Electromagnetic Systems Inc.

- Infostellar Inc.

- Kongsberg Satellite Services AS

- L3 Harris Technologies, Inc.

- Laser Light Communications, LLC

- Lockheed Martin Corporation

- Mynaric AG

- NEC Corporation

- Thales Group

目次

The Global Satellite Laser Communication Market, valued at USD 933.7 million in 2024, is projected to surge at a CAGR of 45.4% from 2025 to 2034. This growth is driven by escalating demand for high-speed data transmission, enhanced bandwidth, and widespread deployment in complex fiber systems. As carrier frequencies evolve, modulation techniques improve, increasing data-carrying capacity for efficient point-to-point transmission. Businesses worldwide are prioritizing fast and reliable connectivity to boost productivity and enhance customer service, driving demand for high-speed data transmission. Satellite laser communication enables superior data rates, minimizing signal loss and ensuring seamless transmission. The technology offers higher bandwidth than radio frequency systems and requires lower weight, volume, and power, making it ideal for satellite constellations and space exploration. With the rising number of low Earth orbit (LEO) satellites, the adoption of satellite laser communication continues to expand. Companies are investing in advanced modulation techniques to optimize data reliability and transmission efficiency.

The market is segmented based on solutions into space-to-space, space-to-ground station, and space-to-other applications. Space-to-space communication, valued at USD 363.2 million in 2023, supports high-speed inter-satellite data transfer, enhancing real-time connectivity. The space-to-ground station segment, worth USD 196 million in 2022, enables efficient data transmission for scientific research, global broadband, and weather forecasting services. Space-to-other applications, which generated USD 46.5 million in 2021, include deep-space exploration and planetary missions, necessitating long-range optical communication with minimal latency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $933.7 Million |

| Forecast Value | $36.4 Billion |

| CAGR | 45.4% |

The market is also classified by components, including optical heads, modems, laser receivers and transmitters, and modulators. The optical head segment is set to account for 31.2% of the market in 2024, crucial for precise laser beam transmission using advanced optics. Laser receivers and transmitters, projected to hold 24.8% of the market, ensure secure, high-speed data exchange. Modems, with a 20.4% share, convert digital data into optical signals for seamless transmission, while modulators, representing 17.2% of the market, enhance spectral efficiency and data throughput.

Segmentation by range includes short, medium, and long-range communication. The short-range segment, valued at USD 215.8 million in 2024, covers LEO satellite links for Earth observation and real-time broadband networks. Medium-range communication, worth USD 123.3 million in 2023, connects satellites in different orbits. The long-range segment, valued at USD 325.9 million in 2022, supports deep-space missions and interplanetary probes.

End-use categories include commercial, government, and military applications. The commercial segment, the largest at USD 552.2 million in 2024, is expanding due to increased demand for global broadband and data relay services. The government sector, valued at USD 200.8 million in 2024, leverages laser communication for climate monitoring, disaster management, and secure data exchange. The military sector, expected to grow at a 46.7% CAGR from 2025 to 2034, invests in secure, high-speed communication for defense and surveillance operations.

North America dominates the market with a 32.4% share in 2024, driven by significant investments in telecommunication infrastructure. The US market, valued at USD 255.8 million in 2024, is advancing rapidly due to strong government and private sector investments in satellite-based communication systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-speed data transmission

- 3.6.1.2 Space exploration and satellite constellations

- 3.6.1.3 Increasing adoption of space-based services

- 3.6.1.4 Advancements in laser communication technology

- 3.6.1.5 Government initiatives and investments

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and deployment costs

- 3.6.2.2 Limited availability of space-qualified components

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Space-to-Space

- 5.3 Space-to-Ground station

- 5.4 Space-to-Other applications

Chapter 6 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Optical head

- 6.3 Laser receivers and transmitters

- 6.4 Modems

- 6.5 Modulators

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Range, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Short range (Below 5,000 Km)

- 7.3 Medium range (5,000-35,000 Km)

- 7.4 Long range (Above 35,000 Km)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

- 8.4 Military

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus SE

- 10.2 Axelspace Corporation

- 10.3 Ball Aerospace & Technologies Corp.

- 10.4 Blue Canyon Technologies LLC

- 10.5 BridgeComm, Inc.

- 10.6 EnduroSat AD

- 10.7 General Atomics Electromagnetic Systems Inc.

- 10.8 Infostellar Inc.

- 10.9 Kongsberg Satellite Services AS

- 10.10. L3 Harris Technologies, Inc.

- 10.11 Laser Light Communications, LLC

- 10.12 Lockheed Martin Corporation

- 10.13 Mynaric AG

- 10.14 NEC Corporation

- 10.15 Thales Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日