|

市場調査レポート

商品コード

1698525

水リサイクル・再利用の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Water Recycle and Reuse Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 水リサイクル・再利用の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月05日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

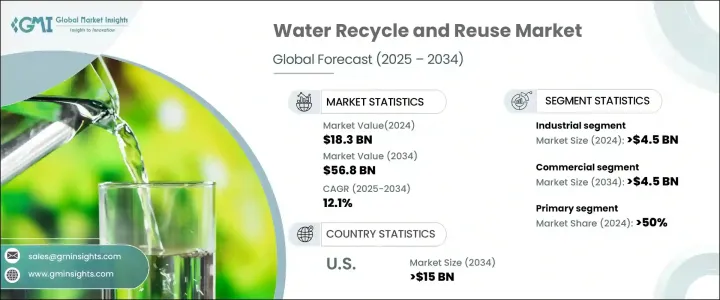

世界の水リサイクル・再利用市場は、2024年に183億米ドルと評価され、2025年から2034年にかけてCAGR12.1%で成長すると予測されています。

急速な人口増加、気候変動、都市化に伴う淡水需要の増加が、産業界、自治体、農業部門に水リサイクルソリューションへの投資を促しています。世界各国の政府は、厳格な節水政策を実施し、高度な再生・処理技術を推進しており、市場の成長を強化しています。

膜分離活性汚泥法、紫外線消毒法、ろ過法、逆浸透法などの継続的な進歩により、水リサイクルシステムのコスト効率と効率が向上し、需要がさらに刺激されています。天然水源への依存を減らすため、持続可能な水ソリューションへのシフトが進んでいることも、市場拡大に寄与しています。食品・飲料加工、石油・ガス、発電、製造など、業務効率を維持するために大量の水を必要とする業界は、市場開拓の主要な促進要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 183億米ドル |

| 予測金額 | 568億米ドル |

| CAGR | 12.1% |

市場は技術別に一次、二次、三次処理システムに区分されます。一次処理分野は2024年の収益の50%以上を占め、規制への対応と世界の水不足に支えられています。環境基準を満たし、資源効率の向上を目指す産業界による海水淡水化とゼロ液体排出ソリューションの採用が、市場浸透の原動力となっています。

工業分野は2024年に45億米ドルに達し、2034年には150億米ドルを超えると予測され、企業は地方自治体の水供給への依存を減らすため、モジュール式で拡張可能なオンサイトリサイクルシステムに注力しています。製薬、食品加工、石油化学、半導体産業では、安定した水質と高純度の水が必要とされており、これが市場力学に影響を与える主な要因となっています。2024年に35億米ドルと評価される農業分野は、気候変動、地下水の枯渇、予測不可能な降雨パターンにより、水リサイクルソリューションの採用が増加しています。濾過、UV消毒、逆浸透などの技術は、安全で効果的な農業廃水の再利用を可能にしています。

住宅部門は2024年に14%の売上シェアを占め、住宅所有者は廃棄物を最小限に抑え、日常使用の水供給を最適化するために水再利用技術に投資しています。洗濯、シャワー、雨水の再利用など、非飲料水用途のリサイクルシステムが人気を集めています。病院、ショッピングセンター、ホテル、オフィスビル、その他の商業施設で水再利用システムの導入が進んでいることから、商業分野は2034年までに45億米ドルを超えると予想されています。政府の優遇措置、税制優遇措置、連邦政府からの補助金が、この動向をさらに後押ししています。

都市化と厳しい廃水規制により、下水処理と水調達技術の導入が促進されています。各都市は、運用コストの削減とインフラ強化のため、これらのソリューションを統合しています。米国市場は2024年に69億米ドルと評価され、自治体や産業界が水不足、インフラの課題、気候関連の懸念に対処するための持続可能なソリューションを模索していることから、2034年には150億米ドルを超えると予測されています。この地域は地下水に依存しており、干ばつが長期化していることが、再生水プラントの採用に拍車をかけています。

北米は、ESG戦略、節水、高度ろ過技術を重視する傾向が強まっており、2034年までCAGR10%以上の成長が見込まれています。各国政府は、持続可能な水再利用ソリューションを促進するためのインセンティブを提供し、研究開発イニシアチブに資金を提供しており、市場全体の勢いを促進しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 一次

- 二次

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 一次

- 精密ろ過(MF)

- 限外ろ過(UF)

- ナノろ過(NF)

- 逆浸透(RO)

- 脱塩

- 二次

- 高度酸化プロセス(AOP)

- 消毒

- 化学凝集・凝集

- 膜分離活性汚泥法(MBR)

- 粒状活性炭(GAC)ろ過

- イオン交換

- 生物学的治療

- 三次処理

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 工業

- 農業

- 住宅

- 商業

- 自治体

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- シンガポール

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

第8章 企業プロファイル

- 3M

- ABB

- American Water

- Aquatech

- BASF

- Dow

- Ecolab

- Hitachi

- Kurita Water Industries

- MANN+HUMMEL

- OVIVO

- Pentair

- Siemens

- SUEZ

- Triveni Engineering &Industries

- Trojan Technologies Group

- Veolia

- Xylem

The Global Water Recycle And Reuse Market was valued at USD 18.3 billion in 2024 and is projected to grow at a CAGR of 12.1% from 2025 to 2034. Rising demand for freshwater, driven by rapid population growth, climate change, and urbanization, is pushing industries, municipalities, and the agricultural sector to invest in water recycling solutions. Governments worldwide are enforcing strict water conservation policies and promoting advanced reclamation and treatment technologies, strengthening market growth.

Ongoing advancements in membrane bioreactors, ultraviolet disinfection, filtration, and reverse osmosis are making water recycling systems more cost-effective and efficient, further stimulating demand. The increasing shift toward sustainable water solutions to reduce dependence on natural water sources is also contributing to market expansion. Industries such as food and beverage processing, oil and gas, power generation, and manufacturing, which require large volumes of water to maintain operational efficiency, are key drivers of market development.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.3 Billion |

| Forecast Value | $56.8 Billion |

| CAGR | 12.1% |

The market is segmented by technology into primary, secondary, and tertiary treatment systems. The primary segment accounted for over 50% of revenue in 2024, supported by regulatory compliance and increasing global water stress. The adoption of desalination and zero-liquid discharge solutions by industries aiming to meet environmental standards and improve resource efficiency is driving market penetration.

The industrial sector reached USD 4.5 billion in 2024 and is projected to exceed USD 15 billion by 2034, with companies focusing on modular and scalable on-site recycling systems to reduce reliance on municipal water supplies. The need for consistent water quality and high-purity water in pharmaceutical, food processing, petrochemical, and semiconductor industries is a key factor influencing market dynamics. The agricultural sector, valued at USD 3.5 billion in 2024, is experiencing increased adoption of water recycling solutions due to climate change, groundwater depletion, and unpredictable rainfall patterns. Technologies such as filtration, UV disinfection, and reverse osmosis are ensuring safe and effective agricultural wastewater reuse.

The residential segment held a 14% revenue share in 2024, with homeowners investing in water reuse technologies to minimize waste and optimize water supply for daily use. Recycling systems for non-potable applications, including laundry, showers, and rainwater reuse, are gaining popularity. The commercial segment is set to exceed USD 4.5 billion by 2034, as water reuse systems are increasingly implemented in hospitals, shopping centers, hotels, office buildings, and other commercial establishments. Government incentives, tax benefits, and federal grants are further supporting this trend.

Municipal water recycling held a 28.9% market share in 2024, with urbanization and stringent wastewater regulations promoting the adoption of sewage treatment and water procurement technologies. Cities are integrating these solutions to reduce operational costs and enhance infrastructure. The U.S. market was valued at USD 6.9 billion in 2024 and is anticipated to surpass USD 15 billion by 2034, as municipalities and industries seek sustainable solutions to address water scarcity, infrastructure challenges, and climate-related concerns. The region's dependence on groundwater and prolonged droughts are fueling the adoption of recycled water plants.

North America is expected to grow at a CAGR of over 10% through 2034, with increasing emphasis on ESG strategies, water conservation, and advanced filtration technologies. Governments are offering incentives and funding R&D initiatives to promote sustainable water reuse solutions, driving overall market momentum.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Primary

- 5.2.1 Microfiltration (MF)

- 5.2.2 Ultrafiltration (UF)

- 5.2.3 Nanofiltration (NF)

- 5.2.4 Reverse Osmosis (RO)

- 5.2.5 Desalination

- 5.3 Secondary

- 5.3.1 Advanced Oxidation Processes (AOP)

- 5.3.2 Disinfection

- 5.3.3 Chemical coagulation and flocculation

- 5.3.4 Membrane Bioreactors (MBRs)

- 5.3.5 Granular Activated Carbon (GAC) filtration

- 5.3.6 Ion exchange

- 5.3.7 Biological treatment

- 5.4 Tertiary

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Industrial

- 6.3 Agriculture

- 6.4 Residential

- 6.5 Commercial

- 6.6 Municipal

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Singapore

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

Chapter 8 Company Profiles

- 8.1 3M

- 8.2 ABB

- 8.3 American Water

- 8.4 Aquatech

- 8.5 BASF

- 8.6 Dow

- 8.7 Ecolab

- 8.8 Hitachi

- 8.9 Kurita Water Industries

- 8.10 MANN+HUMMEL

- 8.11 OVIVO

- 8.12 Pentair

- 8.13 Siemens

- 8.14 SUEZ

- 8.15 Triveni Engineering & Industries

- 8.16 Trojan Technologies Group

- 8.17 Veolia

- 8.18 Xylem