|

市場調査レポート

商品コード

1698323

ワイヤレスセンサーネットワーク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Wireless Sensor Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ワイヤレスセンサーネットワーク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月05日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

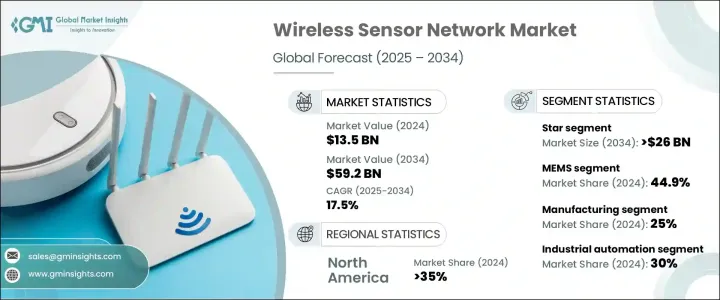

ワイヤレスセンサーネットワークの世界市場は、2024年に135億米ドルと評価され、業界全体でIoTとスマート技術の採用が増加していることを背景に、2025年から2034年にかけてCAGR 17.5%で拡大すると予測されています。

企業や消費者がコネクテッド・デバイスを日常業務に組み込み続ける中、効率的で信頼性の高いセンサーベースのネットワークに対する需要が急増しています。ワイヤレスセンサーネットワークは、産業プロセスの自動化、リアルタイム・データ収集の最適化、多様なアプリケーションの接続性強化に不可欠となっています。スマートホームや産業オートメーションからヘルスケアや環境モニタリングに至るまで、これらのネットワークは業務を合理化し、効率を向上させています。

世界中の組織がデジタルトランスフォーメーションへの取り組みを加速させる中、業界ではデータ主導の意思決定を強化するため、先進的なセンサーネットワークへの投資が増加しています。インダストリー4.0技術の広範な採用は、特にリアルタイムのモニタリングと自動化が重要な製造業やロジスティクスにおいて、無線センサーネットワークの需要を促進しています。従来の有線システムの制約を受けずにシームレスな接続性を提供するこれらのネットワークの能力が、市場の成長を後押ししています。政府や企業もスマートシティ構想に投資しており、交通管理、大気質モニタリング、セキュリティなどの用途でセンサーベースのネットワークの採用をさらに促進しています。低消費電力通信プロトコルとエッジ・コンピューティングの進歩により、ワイヤレスセンサーネットワークは、業界全体でより高い効率性、信頼性、拡張性を実現するように進化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 135億米ドル |

| 予測金額 | 592億米ドル |

| CAGR | 17.5% |

市場は、バス、スター、ツリー、メッシュ構成など、ネットワーク・トポロジー別に区分されます。2024年の市場シェアはスター型が40%を占め、2034年には260億米ドルに達すると予測されています。企業がスター型トポロジーを好むのは、すべてのセンサーノードが中央ハブに接続し、通信の複雑さを軽減し、システムの信頼性を高めるという、そのわかりやすい構造によるものです。この設計により、データ転送の遅延が最小限に抑えられ、高速で安全な無線通信が保証されるため、効率性と導入の容易さが求められるアプリケーションに最適です。スター型トポロジーの低メンテナンス要件と費用対効果は、さまざまな産業での採用拡大にさらに貢献しています。

ワイヤレスセンサーネットワークはセンサの種類によっても分類され、MEMSセンサ、CMOSベース・センサ、LEDセンサなどが市場で重要な役割を果たしています。2024年の市場シェアはMEMSセンサが44.9%を占め、優位を占めています。小型でエネルギー効率が高く、電子機器にシームレスに統合できることから、産業オートメーション、ヘルスケア、環境モニタリング用途に好まれています。データ主導の洞察に頼る産業が増える中、MEMSセンサーはリアルタイムのモニタリングと業務効率の強化に計り知れない価値を発揮しています。

米国はワイヤレスセンサーネットワーク市場をリードし、2024年には35%のシェアを占める。同国は依然として産業用IoT導入の最前線にあり、企業はワイヤレスセンサネットワークを活用して生産性の向上、物流の合理化、自動化を推進しています。確立されたセンサー技術産業と堅牢な無線インフラが相まって、市場の拡大が加速しています。接続技術が進歩し、スマートソリューションが普及するにつれて、ワイヤレスセンサーネットワークは、自動化、リアルタイム分析、インテリジェントな意思決定の未来を形成する上で、さまざまな分野で変革的な役割を果たすようになると思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ソリューションプロバイダー

- サービスプロバイダー

- テクノロジープロバイダー

- エンドユース

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- IoTとスマートデバイスの需要増加

- 産業オートメーションやスマートシティでの採用拡大

- AIや機械学習との統合

- 業界の潜在的リスク&課題

- 設置やメンテナンスのコストが高い

- エネルギー消費の課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:トポロジー別、2021年~2034年

- 主要動向

- バス

- スター

- ツリー

- メッシュ

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 地上

- 地中

- 水中

- マルチメディア

- モバイル

第7章 市場推計・予測:センサー別、2021~2034年

- 主要動向

- MEMS

- CMOSセンサー

- LEDセンサー

- その他

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ワイヤレスHART

- ZigBee

- Wi-Fi

- IPv6

- Bluetooth

- Dash 7

- Z-Wave

第9章 市場推計・予測:アプリケーション別、2021年~2034年

- 主要動向

- ホームオートメーションとビルディングオートメーション

- 産業オートメーション

- 軍事監視

- スマート輸送

- 患者モニタリング

- 機械監視

- その他

第10章 市場推計・予測:産業別、2021年~2034年

- 主要動向

- 自動車

- ヘルスケア

- エネルギー・公益事業

- IT・通信

- 製造業

- 小売

- 航空宇宙・防衛

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- ABB

- Advantech

- Analog Devices

- Broadcom

- Butlr Technologies

- Cisco

- Digi International

- Emerson Electric

- FreeWave Technologies

- Honeywell

- Intel

- Libelium

- Link Labs

- NXP Semiconductors

- Qualcomm

- Schneider Electric

- Siemens

- STMicroelectronics

- TE Connectivity

- Texas Instruments

The Global Wireless Sensor Network Market, valued at USD 13.5 billion in 2024, is projected to expand at a CAGR of 17.5% between 2025 and 2034, driven by the increasing adoption of IoT and smart technology across industries. As businesses and consumers continue to integrate connected devices into their daily operations, the demand for efficient and reliable sensor-based networks is surging. Wireless sensor networks are becoming essential for automating industrial processes, optimizing real-time data collection, and enhancing connectivity across diverse applications. From smart homes and industrial automation to healthcare and environmental monitoring, these networks are streamlining operations and improving efficiency.

As organizations worldwide accelerate digital transformation efforts, industries are increasingly investing in advanced sensor networks to enhance data-driven decision-making. The widespread adoption of Industry 4.0 technologies is fueling the demand for wireless sensor networks, particularly in manufacturing and logistics, where real-time monitoring and automation are critical. The ability of these networks to provide seamless connectivity without the limitations of traditional wired systems is propelling market growth. Governments and enterprises are also investing in smart city initiatives, further driving the adoption of sensor-based networks for applications such as traffic management, air quality monitoring, and security. With advancements in low-power communication protocols and edge computing, wireless sensor networks are evolving to deliver greater efficiency, reliability, and scalability across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.5 billion |

| Forecast Value | $59.2 billion |

| CAGR | 17.5% |

The market is segmented by network topology, including bus, star, tree, and mesh configurations. In 2024, the star topology segment held a 40% market share and is expected to generate USD 26 billion by 2034. Businesses prefer star topology due to its straightforward structure, where all sensor nodes connect to a central hub, reducing communication complexity and enhancing system reliability. This design minimizes data transfer delays and ensures high-speed, secure wireless communication, making it ideal for applications that require efficiency and ease of deployment. The low maintenance requirements and cost-effectiveness of star topology further contribute to its growing adoption across various industries.

Wireless sensor networks are also categorized by sensor type, with MEMS, CMOS-based sensors, LED sensors, and others playing a significant role in the market. MEMS sensors dominated in 2024, accounting for a 44.9% market share. Their compact size, energy efficiency, and ability to integrate seamlessly into electronic devices make them a preferred choice for industrial automation, healthcare, and environmental monitoring applications. With industries increasingly relying on data-driven insights, MEMS sensors are proving invaluable in enhancing real-time monitoring and operational efficiency.

The U.S. leads the wireless sensor network market, holding a 35% share in 2024. The country remains at the forefront of Industrial IoT adoption, with businesses leveraging wireless sensor networks to enhance productivity, streamline logistics, and drive automation. A well-established sensor technology industry, combined with robust wireless infrastructure, is accelerating market expansion. As connectivity technologies advance and smart solutions gain traction, wireless sensor networks are set to play a transformative role in shaping the future of automation, real-time analytics, and intelligent decision-making across multiple sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Solution provider

- 3.1.2 Services provider

- 3.1.3 Technology provider

- 3.1.4 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for IoT and smart devices

- 3.7.1.2 Growing adoption in industrial automation and smart cities

- 3.7.1.3 Integration with AI and machine learning

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High costs of installation and maintenance

- 3.7.2.2 Energy consumption challenges

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Topology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Bus

- 5.3 Star

- 5.4 Tree

- 5.5 Mesh

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Terrestrial

- 6.3 Underground

- 6.4 Underwater

- 6.5 Multimedia

- 6.6 Mobile

Chapter 7 Market Estimates & Forecast, By Sensors, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 MEMS

- 7.3 CMOS-based sensors

- 7.4 LED sensors

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Wireless HART

- 8.3 ZigBee

- 8.4 Wi-Fi

- 8.5 IPv6

- 8.6 Bluetooth

- 8.7 Dash 7

- 8.8 Z-Wave

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Home and building automation

- 9.3 Industrial automation

- 9.4 Military surveillance

- 9.5 Smart transportation

- 9.6 Patient monitoring

- 9.7 Machine monitoring

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Industry, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Healthcare

- 10.4 Energy & utilities

- 10.5 IT & telecom

- 10.6 Manufacturing

- 10.7 Retail

- 10.8 Aerospace & defense

- 10.9 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Advantech

- 12.3 Analog Devices

- 12.4 Broadcom

- 12.5 Butlr Technologies

- 12.6 Cisco

- 12.7 Digi International

- 12.8 Emerson Electric

- 12.9 FreeWave Technologies

- 12.10 Honeywell

- 12.11 Intel

- 12.12 Libelium

- 12.13 Link Labs

- 12.14 NXP Semiconductors

- 12.15 Qualcomm

- 12.16 Schneider Electric

- 12.17 Siemens

- 12.18 STMicroelectronics

- 12.19 TE Connectivity

- 12.20 Texas Instruments