断熱材付パイプシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pre-Insulated Pipe Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698321

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

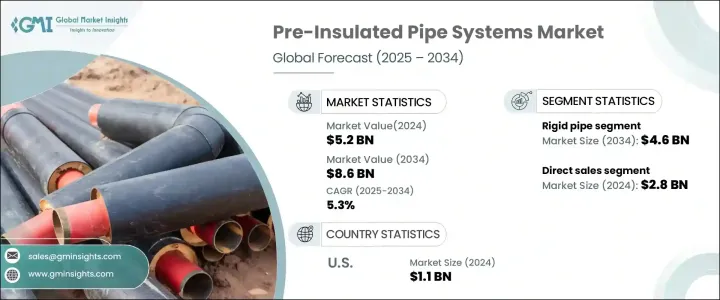

世界の断熱材付パイプシステム市場は、2024年に52億米ドルと評価され、2025年から2034年にかけてCAGR 5.3%で拡大すると予想されています。

地域冷暖房システムの採用が増加していることが、この成長の主な要因です。これらのシステムでは、複数の建物に集中型の冷暖房を供給するために高効率のインフラが必要となるためです。断熱材付パイプは、トランスミッション中の熱損失を最小限に抑え、エネルギー効率を高めるように設計されています。世界の気温上昇に伴い、冷房需要は増加すると予測され、効果的な熱管理ソリューションの必要性が高まっています。化学、製薬、石油化学、データセンターなどの産業の拡大は、温水、冷却水、油、廃水の輸送に断熱材付パイプシステムが不可欠であることから、市場の成長をさらに加速させる。また、大規模な産業用途でエネルギー効率の高いソリューションへの注目が高まっていることも一因となっています。

市場は製品タイプ別に軟質パイプと硬質パイプに区分されます。2024年に28億米ドルと評価された硬質パイプセグメントは、2034年には46億米ドルに達すると予測されています。このセグメントは、耐久性、極端な温度への耐性、機械的ストレスや腐食に耐える能力により、優位性を維持すると予想されます。外側のケーシング、絶縁層、中実の内管を特徴とする硬質プレインシュレーテッドパイプは、地域暖房システム、化学処理、石油・ガスパイプライン、大規模インフラプロジェクトで広く使用されています。発展途上地域におけるエネルギー需要の高まりが、製油所、発電所、工業施設での採用を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 52億米ドル |

| 予測金額 | 86億米ドル |

| CAGR | 5.3% |

流通チャネル別に見ると、市場は直接販売と間接販売に分けられます。直接販売分野は、2024年に28億米ドルとなり、2025年から2034年にかけてCAGR 5.5%で成長すると予測されます。直接販売は、メーカーが建設会社、工業企業、政府機関などのエンドユーザーに製品を供給するものです。このアプローチは、長期的な協力関係を育み、オーダーメイドのソリューションを保証します。電力・エネルギー部門を含む大規模なインフラ・プロジェクトは、プロジェクトのスケジュールを遵守する上で直接販売が効率的であるため、直接調達に大きく依存しています。メーカーは、顧客との直接的なコミュニケーションによって、カスタマイズされた製品を提供し、リードタイムを短縮できるというメリットがあります。

米国の断熱材付パイプシステム市場は、2024年に11億米ドルと評価され、2025年から2034年にかけてCAGR 5.2%で成長すると予測されています。北米の市場拡大は、急速な都市化、インフラ開拓、地域冷暖房システムの採用拡大が原動力となっています。エネルギー効率と持続可能性への取り組みが重視され、再生可能エネルギープロジェクトの増加も相まって、需要はさらに高まっています。商業・工業用途で熱効率を高める取り組みが進む中、プレインシュレーテッド・パイプ・システムは、エネルギー使用の最適化と運用コストの削減において重要な役割を果たし続けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測パラメータ

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- 小売業者

- 影響要因

- 促進要因

- 地域冷暖房システムの需要急増

- 最終用途産業からの需要の増加

- 業界の潜在的リスク&課題

- 高い初期費用とメンテナンス費用

- 安全性への懸念と熟練労働者の不足

- 促進要因

- 技術革新の状況

- 潜在成長力の分析

- 規制状況

- 価格分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2032年

- 軟質パイプ

- 硬質パイプ

第6章 市場推計・予測:防火タイプ別、2021年~2032年

- 主要動向

- 難燃性パイプ

- 非難燃性パイプ

第7章 難燃性パイプ市場推計・予測:ディメンション別、2021~2032年

- 主要動向

- 小径パイプ(65mm未満)

- 軟質パイプ

- 硬質パイプ

- 中口径パイプ(65~300mm)

- 軟質パイプ

- 硬質パイプ

- 大口径管(300mm以上)

- 軟質パイプ

- 硬質パイプ

第8章 市場推計・予測:設置別、2021年~2032年

- 主要動向

- 地下

- 地上

第9章 市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 住宅用ビル

- 商業ビル

- 産業用ビル

第10章 市場推計・予測:流通チャネル別、2021年~2032年

- 主要動向

- 直接販売

- 間接販売

第11章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 中東・アフリカ

- サウジアラビア

- UAE

- 南アフリカ

- 世界のその他の地域

第12章 企業プロファイル

- Aquatherm

- Brugg Group

- CPV

- Ecoline

- Elips

- Georg Fischer

- Insul-Pipe Systems

- KE KELIT

- LOGSTOR

- Perma-Pipe International

- Polypipe Group

- REHAU

- Thermaflex International

- Vital Energi Utilities

- Watts Water Technologies

目次

The Global Pre-Insulated Pipe Systems Market, valued at USD 5.2 billion in 2024, is expected to expand at a CAGR of 5.3% from 2025 to 2034. The rising adoption of district heating and cooling systems is a key driver of this growth, as these systems require highly efficient infrastructure to deliver centralized heating and cooling to multiple buildings. Pre-insulated pipes are designed to minimize heat loss during transmission, enhancing energy efficiency. As global temperatures rise, cooling demand is projected to increase, pushing the need for effective thermal management solutions. The expansion of industries such as chemical, pharmaceutical, petrochemical, and data centers further accelerates market growth, as pre-insulated pipe systems are essential for transporting hot water, cooling water, oil, and wastewater. The increasing focus on energy-efficient solutions in large-scale industrial applications is also a contributing factor.

The market is segmented by product type into flexible and rigid pipes. The rigid pipe segment, valued at USD 2.8 billion in 2024, is anticipated to reach USD 4.6 billion by 2034. This segment is expected to maintain its dominance due to its durability, resistance to extreme temperatures, and ability to withstand mechanical stress and corrosion. Rigid pre-insulated pipes featuring an outer casing, insulating layer, and solid inner pipe are widely used in district heating systems, chemical processing, oil and gas pipelines, and large-scale infrastructure projects. The growing demand for energy in developing regions is fueling their adoption in refineries, power plants, and industrial facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.3% |

By distribution channel, the market is divided into direct and indirect sales. The direct sales segment, valued at USD 2.8 billion in 2024, is projected to grow at a CAGR of 5.5% from 2025 to 2034. Direct sales involve manufacturers supplying products to end users such as construction firms, industrial businesses, and government agencies. This approach fosters long-term collaborations and ensures tailored solutions. Large-scale infrastructure projects, including those in the power and energy sectors, rely heavily on direct procurement due to the efficiency of direct sales in meeting project timelines. Manufacturers benefit from direct communication with customers, enabling them to provide customized products and reduce lead times.

The U.S. pre-insulated pipe systems market, valued at USD 1.1 billion in 2024, is forecasted to grow at a CAGR of 5.2% between 2025 and 2034. North America's market expansion is driven by rapid urbanization, infrastructure development, and increased adoption of district heating and cooling systems. The emphasis on energy efficiency and sustainability initiatives, coupled with the rise of renewable energy projects, is further boosting demand. With growing efforts to enhance thermal efficiency in commercial and industrial applications, pre-insulated pipe systems continue to play a crucial role in optimizing energy usage and reducing operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for district heating and cooling system

- 3.2.1.2 Increase in demand from end-use industries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial and maintenance cost

- 3.2.2.2 Safety concern and limited availability of skilled labor

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2032, (USD Million) (Million Meters)

- 5.1 Flexible pipe

- 5.2 Rigid pipe

Chapter 6 Market Estimates & Forecast, By Fire Protection, 2021 – 2032, (USD Million) (Million Meters)

- 6.1 Key trends

- 6.2 Flame-Retardant pipes

- 6.3 Non-Flame-Retardant pipes

Chapter 7 Market Estimates & Forecast, By Dimensions, 2021 – 2032, (USD Million) (Million Meters)

- 7.1 Key trends

- 7.2 Small diameter pipes(Up to 65 mm)

- 7.2.1 Flexible pipe

- 7.2.2 Rigid pipe

- 7.3 Medium diameter pipes(65 to 300 mm)

- 7.3.1 Flexible pipe

- 7.3.2 Rigid pipe

- 7.4 Large diameter pipes(Above 300 mm)

- 7.4.1 Flexible pipe

- 7.4.2 Rigid pipe

Chapter 8 Market Estimates & Forecast, By Installation, 2021 – 2032, (USD Million) (Million Meters)

- 8.1 Key trends

- 8.2 Below ground

- 8.3 Above ground

Chapter 9 Market Estimates & Forecast, By End Use, 2021 – 2032, (USD Million) (Million Meters)

- 9.1 Key trends

- 9.2 Residential buildings

- 9.3 Commercial buildings

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 – 2032, (USD Million) (Million Meters)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 – 2032, (USD Million) (Million Meters)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 MEA

- 11.4.1 Saudi Arabia

- 11.4.2 UAE

- 11.4.3 South Africa

- 11.5 Rest of World

Chapter 12 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 12.1 Aquatherm

- 12.2 Brugg Group

- 12.3 CPV

- 12.4 Ecoline

- 12.5 Elips

- 12.6 Georg Fischer

- 12.7 Insul-Pipe Systems

- 12.8 KE KELIT

- 12.9 LOGSTOR

- 12.10 Perma-Pipe International

- 12.11 Polypipe Group

- 12.12 REHAU

- 12.13 Thermaflex International

- 12.14 Vital Energi Utilities

- 12.15 Watts Water Technologies

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日