|

市場調査レポート

商品コード

1698311

シグナルインテリジェンス(SIGINT)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Signals Intelligence (SIGINT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| シグナルインテリジェンス(SIGINT)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月14日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

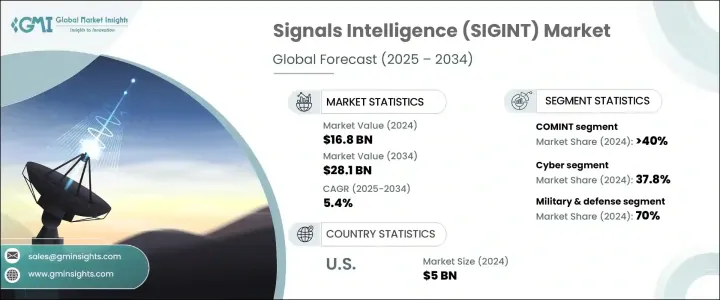

世界のシグナルインテリジェンス市場は2024年に168億米ドルに達し、2025年から2034年にかけてCAGR 5.4%で成長すると予測されています。

この成長の主な要因は、人工知能(AI)とセンサー技術の急速な進歩です。AIアルゴリズムは膨大な量のデータを迅速に処理する能力を強化し、脅威の迅速な特定を可能にします。機械学習と相まって、これらのシステムは通信や電子信号のパターンや異常を認識する能力に長けてきています。感度やフィルタリングの向上など、センサー機能の強化により、SIGINT・プラットフォームの探知範囲と精度が大幅に向上し、より効率的で正確な情報収集が可能になりました。このような進歩により、戦術的・戦略的情報活動の有効性が高まる一方で、人間のオペレーターへの依存度が低下しています。

世界の地政学的緊張と軍事的対立の高まりにより、SIGINTシステムに対する需要はエスカレートしています。また、電子戦(EW)に対する懸念から市場も拡大しており、SIGINTはジャミングやスプーフィングなどの電子的脅威に対抗する上で重要な役割を果たしています。特に東欧、インド太平洋、中東などの地域では脅威が進化し続けているため、各国は現代戦での競合を維持するためにSIGINTを軍事戦略に組み込んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 168億米ドル |

| 予測金額 | 281億米ドル |

| CAGR | 5.4% |

市場は主に通信諜報(COMINT)、電子諜報(ELINT)、対外計測信号諜報(FISINT)などタイプ別に区分されます。このうちCOMINTが市場をリードし、2024年にはシェア全体の40%以上を占める。COMINTソリューションは、音声、テキスト、暗号化されたメッセージの傍受と分析に軍事・安全保障機関での利用が増加しており、リアルタイムの脅威検知とサイバー防衛において重要な役割を果たしています。

用途別では、サイバー分野が急成長を遂げており、市場で大きなシェアを占めています。サイバースパイやデジタル戦争による脅威の増大に伴い、重要インフラの保護を目的としたサイバーSIGINT技術への資金提供が急増しています。政府や防衛機関は、リアルタイムの脅威検知能力を強化するため、自動化されたAI主導のシステムに多額の投資を行っています。

軍事・防衛分野は引き続きSIGINT市場を独占しており、2024年には市場シェア全体の70%近くを占める。電子戦や脅威検知ソリューションに対する需要の高まりが、この分野の大きな成長を後押ししています。さらに、各国政府はスパイ活動、テロ対策、国境警備活動にSIGINTを活用しています。商業部門もサイバー脅威から保護し、安全な通信を確保するためにSIGINT技術を採用しています。

北米は世界のSIGINT市場をリードしており、米国は2024年に50億米ドルの大きなシェアを占める。米国はAIを活用した信号処理とデータ分析に多額の投資を行い、防衛と諜報能力を強化し、強固な国家安全保障を確保しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テレマティクス・ハードウェア・プロバイダー

- ソフトウェア開発企業

- 無線通信事業者

- システムインテグレーター

- 車両管理サービスプロバイダー

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 使用事例

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- テレマティクスとIoTに対する需要の高まり

- 厳しい安全・排ガス規制

- eコマースとラストワンマイルデリバリーの成長

- 電気自動車と自律走行車の採用拡大

- 業界の潜在的リスク&課題

- データ過多と管理上の懸念

- ドライバー管理と安全性の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- COMINT(通信インテリジェンス)

- ELINT(エレクトロニック・インテリジェンス)

- FISINT(対外計測信号情報)

第6章 市場推計・予測:アプリケーション別、2021年~2034年

- 主要動向

- サイバー

- 地上

- 航空機

- 戦闘機

- 特殊任務機

- 輸送機

- 無人航空機(UAV)

- 海軍

- 船舶

- 潜水艦

- 無人海上車両(UMV)

- 宇宙

第7章 市場推計・予測:モビリティ別、2021年~2034年

- 主要動向

- 固定型

- ポータブル

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 軍事・防衛

- 政府・法執行機関

- 商業・民間

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Airbus

- BAE Systems

- Boeing

- Collins Aerospace

- DRS RADA Technologies

- Elbit Systems

- General Atomics

- General Dynamics

- Hensoldt

- Israel Aerospace Industries

- L3Harris

- Leonardo

- Lockheed Martin

- Mercury Systems

- Northrop Grumman

- Raytheon

- Rohde &Schwarz

- Saab

- SRC

- Thales

The Global Signals Intelligence Market reached USD 16.8 billion in 2024 and is expected to grow at a CAGR of 5.4% from 2025 to 2034. This growth is primarily fueled by rapid advancements in artificial intelligence (AI) and sensor technologies. AI algorithms enhance the ability to process vast amounts of data quickly, allowing for faster identification of threats. Coupled with machine learning, these systems are becoming more adept at recognizing patterns and anomalies in communications and electronic signals. Enhanced sensor capabilities, such as improved sensitivity and filtering, have significantly increased the range and precision of SIGINT platforms, enabling more efficient and accurate intelligence collection. These advancements are reducing the reliance on human operators while boosting the effectiveness of both tactical and strategic intelligence operations.

The rising geopolitical tensions and military confrontations worldwide have escalated the demand for SIGINT systems, as countries are increasingly relying on these technologies to monitor adversaries and secure national defense. The market is also expanding due to concerns over electronic warfare (EW), with SIGINT playing a crucial role in countering jamming, spoofing, and other electronic threats. Countries are integrating SIGINT into their military strategies to maintain a competitive edge in modern warfare, especially as threats continue to evolve in regions like Eastern Europe, the Indo-Pacific, and the Middle East.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.8 Billion |

| Forecast Value | $28.1 Billion |

| CAGR | 5.4% |

The market is primarily segmented by types, including Communications Intelligence (COMINT), Electronic Intelligence (ELINT), and Foreign Instrumentation Signals Intelligence (FISINT). Among these, COMINT leads the market, accounting for over 40% of the total share in 2024. COMINT solutions are increasingly used by military and security agencies for intercepting and analyzing voice, text, and encrypted messages, which play a critical role in real-time threat detection and cyber defense.

In terms of applications, the cyber segment is witnessing rapid growth, capturing a significant share of the market. With the increasing threats from cyber espionage and digital warfare, there has been a surge in funding for cyber SIGINT technologies aimed at protecting critical infrastructure. Governments and defense agencies are heavily investing in automated, AI-driven systems to enhance real-time threat detection capabilities.

The military and defense sector continues to dominate the SIGINT market, accounting for nearly 70% of the total market share in 2024. The increasing demand for electronic warfare and threat detection solutions is driving significant growth in this sector. Additionally, governments are leveraging SIGINT for espionage, counterterrorism, and border security operations. The commercial sector is also adopting SIGINT technologies to safeguard against cyber threats and ensure secure communication.

North America leads the global SIGINT market, with the United States contributing a substantial share of USD 5 billion in 2024. The U.S. is making significant investments in AI-powered signal processing and data analytics to strengthen its defense and intelligence capabilities, ensuring robust national security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Telematics hardware providers

- 3.2.2 Software developers

- 3.2.3 Wireless carriers

- 3.2.4 System integrators

- 3.2.5 Fleet management service providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising Demand for telematics & IoT

- 3.9.1.2 Stringent safety & emission regulations

- 3.9.1.3 Growth in e-commerce & last-mile delivery

- 3.9.1.4 Growing adoption of electric & autonomous vehicles

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data overload and management concerns

- 3.9.2.2 Driver management and safety issues

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 COMINT (Communications Intelligence)

- 5.3 ELINT (Electronic Intelligence)

- 5.4 FISINT (Foreign Instrumentation Signals Intelligence)

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cyber

- 6.3 Ground

- 6.4 Airborne

- 6.4.1 Fighter jets

- 6.4.2 Special mission aircraft

- 6.4.3 Transport aircraft

- 6.4.4 Unmanned Aerial Vehicles (UAVs)

- 6.5 Naval

- 6.5.1 Ships

- 6.5.2 Submarines

- 6.5.3 Unmanned Marine Vehicles (UMVs)

- 6.6 Space

Chapter 7 Market Estimates & Forecast, By Mobility, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Fixed

- 7.3 Portable

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Military & defense

- 8.3 Government & law enforcement

- 8.4 Commercial & private sector

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airbus

- 10.2 BAE Systems

- 10.3 Boeing

- 10.4 Collins Aerospace

- 10.5 DRS RADA Technologies

- 10.6 Elbit Systems

- 10.7 General Atomics

- 10.8 General Dynamics

- 10.9 Hensoldt

- 10.10 Israel Aerospace Industries

- 10.11 L3Harris

- 10.12 Leonardo

- 10.13 Lockheed Martin

- 10.14 Mercury Systems

- 10.15 Northrop Grumman

- 10.16 Raytheon

- 10.17 Rohde & Schwarz

- 10.18 Saab

- 10.19 SRC

- 10.20 Thales