|

市場調査レポート

商品コード

1698299

次世代ネットワーキング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Next Generation Networking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 次世代ネットワーキング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

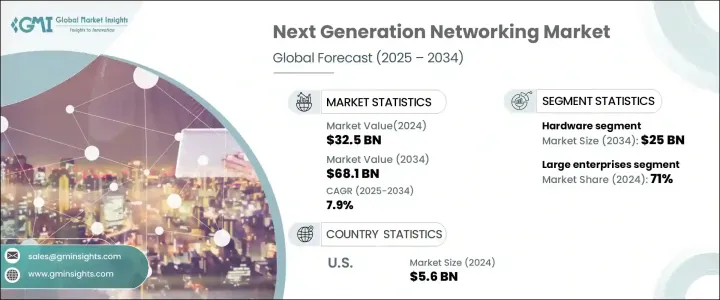

次世代ネットワーキングの世界市場規模は2024年に325億米ドルとなり、2025年から2034年にかけてCAGR 7.9%で成長すると予測されています。

同市場は、クラウドコンピューティングやクラウドストレージサービスへの依存度の高まり、世界のデジタルインフラの拡大などを背景に、急速な変貌を遂げています。企業が業務とデータをクラウドに移行するにつれ、シームレスな接続性、高帯域幅、低遅延を提供する高度なネットワーキング・ソリューションの必要性がこれまで以上に高まっています。人工知能(AI)、モノのインターネット(IoT)、5Gネットワークの採用が進むにつれ、業務効率とリアルタイムデータ処理を強化する最先端技術を求める企業の需要はさらに高まっています。

ソフトウェア定義ネットワーキング(SDN)とネットワーク機能仮想化(NFV)へのシフトは、市場の状況を再形成しており、企業によるネットワーク管理の柔軟性、自動化、コスト効率の向上を可能にしています。また、サイバーセキュリティの脅威と規制コンプライアンス要件により、企業は堅牢なセキュリティ対策でネットワークフレームワークをアップグレードし、データの完全性と回復力を確保する必要に迫られています。さらに、スマートシティ、自律走行車、エッジコンピューティングソリューションの普及により、複雑なデータ集約型アプリケーションをサポートできる次世代ネットワーキング・システムへの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 325億米ドル |

| 予測金額 | 681億米ドル |

| CAGR | 7.9% |

市場はハードウェア、ソフトウェア、サービスに区分され、ハードウェアが最大のシェアを占める。2024年の市場シェアはハードウェアが40%を占め、2034年には250億米ドルに達すると予測されています。ルーター、スイッチ、サーバー、ネットワーク・プロセッサーなどの重要なネットワーキング・コンポーネントは、特に5G、SDN、NFV技術の展開に伴い、高性能インフラを実現する上で極めて重要な役割を果たします。企業は、クラウド・コンピューティング、企業データセンター、通信ネットワークにおける進化する需要に対応するため、スケーラブルで高速なネットワーク機器への投資を優先しています。

企業規模も市場力学に重要な役割を果たしており、大企業が採用を主導しています。2024年には、大企業が次世代ネットワーキング市場で71%のシェアを占め、その資金力を活用して高度で安全なネットワーキング・ソリューションを導入しています。これらの企業は、大規模な業務、従業員のコラボレーション、データ主導の意思決定をサポートする高性能ネットワークに依存しています。一方、中小企業(SME)は、競争力を維持するために拡張性とコスト効率の高いソリューションの必要性を認識し、次世代ネットワーキング技術への投資を徐々に増やしています。

北米は2024年の次世代ネットワーキング世界市場で34%のシェアを占め、米国は地域別評価額に56億米ドルを拠出しています。大手通信事業者の存在に加え、5G展開やデジタル変革イニシアティブへの積極的な投資により、同地域はネットワーク革新のフロントランナーとして位置付けられています。ヘルスケア、金融、製造業などの業界全体で高速かつ低遅延の接続に対する需要が高まっていることが、引き続き市場成長の原動力となっています。次世代無線インフラと新たなネットワーキング技術に強い関心を寄せる北米は、世界のネットワーキング・ソリューションの未来を形作る重要なプレーヤーであり続けると思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ネットワーク・インフラ・プロバイダー

- 通信サービスプロバイダー

- ネットワーク技術とソリューションのベンダー

- エンドユース

- 利益率分析

- テクノロジー&イノベーション・情勢

- 特許分析

- コスト内訳分析

- 主要ニュースと取り組み

- 使用事例

- 規制状況

- 影響要因

- 促進要因

- クラウドコンピューティングとストレージの採用

- 低遅延・リアルタイムアプリケーションの需要

- モノのインターネット(IoT)の台頭

- 5Gの採用拡大

- コスト効率と拡張性の向上

- 業界の潜在的リスク&課題

- 高いインフラコスト

- セキュリティとプライバシーに関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ルーター

- スイッチ

- ファイアウォール

- サーバー

- その他

- ソフトウェア

- ネットワーク管理システム

- ネットワーク・セキュリティ・ソフトウェア

- SDNコントローラー

- ネットワーク仮想化

- その他

- サービス

- プロフェッショナルサービス

- マネージドサービス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- SDN

- NFV

- 5Gネットワーク

- エッジコンピューティング

- その他

第7章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信

- ヘルスケア

- 政府機関

- 自動車

- 製造業

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- A10 Networks

- Adtran

- AT&T

- Check Point Software Technologies

- Ciena Corporation

- Cisco

- Commverge Solutions

- Ericsson

- Forcepoint

- Fortinet

- Huawei

- IBM

- Juniper Networks

- Keysight Technologies

- NEC

- Nokia

- Samsung

- TelcoBridges

- VMware(Broadcom)

- ZTE

The Global Next-Generation Networking Market was valued at USD 32.5 billion in 2024 and is projected to grow at a CAGR of 7.9% between 2025 and 2034. The market is witnessing a rapid transformation driven by the increasing reliance on cloud computing, cloud storage services, and the expansion of digital infrastructures worldwide. As businesses migrate their operations and data to the cloud, the need for advanced networking solutions that offer seamless connectivity, high bandwidth, and low latency is becoming more critical than ever. The growing adoption of artificial intelligence (AI), the Internet of Things (IoT), and 5G networks further fuels the demand as companies seek cutting-edge technologies to enhance operational efficiency and real-time data processing.

The shift toward software-defined networking (SDN) and network function virtualization (NFV) is reshaping the market landscape, enabling organizations to achieve greater flexibility, automation, and cost efficiency in managing their networks. Cybersecurity threats and regulatory compliance requirements are also pushing enterprises to upgrade their networking frameworks with robust security measures, ensuring data integrity and resilience. Additionally, the proliferation of smart cities, autonomous vehicles, and edge computing solutions is amplifying the demand for next-generation networking systems that can support complex, data-intensive applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.5 Billion |

| Forecast Value | $68.1 Billion |

| CAGR | 7.9% |

The market is segmented into hardware, software, and services, with hardware accounting for the largest share. In 2024, the hardware segment held a 40% market share and is expected to reach USD 25 billion by 2034. Essential networking components such as routers, switches, servers, and network processors play a pivotal role in enabling high-performance infrastructure, particularly with the deployment of 5G, SDN, and NFV technologies. Businesses are prioritizing investments in scalable, high-speed networking equipment to meet evolving demands in cloud computing, enterprise data centers, and telecommunication networks.

Enterprise size also plays a significant role in market dynamics, with large enterprises leading adoption. In 2024, large enterprises dominated the next-generation networking market with a 71% share, leveraging their financial capabilities to implement advanced, secure networking solutions. These organizations rely on high-performance networks to support large-scale operations, workforce collaboration, and data-driven decision-making. Meanwhile, small and medium-sized enterprises (SME) are gradually increasing their investments in next-generation networking technologies, recognizing the need for scalable, cost-effective solutions to stay competitive.

North America held a 34% share of the global next-generation networking market in 2024, with the United States contributing USD 5.6 billion to the regional valuation. The presence of major telecom players, coupled with aggressive investments in 5G deployment and digital transformation initiatives, has positioned the region as a frontrunner in network innovation. The increasing demand for high-speed, low-latency connectivity across industries, including healthcare, finance, and manufacturing, continues to drive market growth. With a strong focus on next-gen wireless infrastructure and emerging networking technologies, North America is set to remain a key player in shaping the future of global networking solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Network infrastructure providers

- 3.2.2 Telecommunication service providers

- 3.2.3 Network technology and solutions vendors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Use cases

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Adoption of cloud computing and storage

- 3.10.1.2 Demand for low latency and real-time applications

- 3.10.1.3 Rise of the Internet of Things (IoT)

- 3.10.1.4 Growing 5G adoption

- 3.10.1.5 Increased cost efficiency and scalability

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High infrastructure costs

- 3.10.2.2 Security and privacy concerns

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Routers

- 5.2.2 Switches

- 5.2.3 Firewalls

- 5.2.4 Servers

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Network management systems

- 5.3.2 Network security software

- 5.3.3 SDN controllers

- 5.3.4 Network virtualization

- 5.3.5 Others

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 SDN

- 6.3 NFV

- 6.4 5G networks

- 6.5 Edge computing

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Cloud-based

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Telecommunication

- 9.3 Healthcare

- 9.4 Government

- 9.5 Automotive

- 9.6 Manufacturing

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 A10 Networks

- 11.2 Adtran

- 11.3 AT&T

- 11.4 Check Point Software Technologies

- 11.5 Ciena Corporation

- 11.6 Cisco

- 11.7 Commverge Solutions

- 11.8 Ericsson

- 11.9 Forcepoint

- 11.10 Fortinet

- 11.11 Huawei

- 11.12 IBM

- 11.13 Juniper Networks

- 11.14 Keysight Technologies

- 11.15 NEC

- 11.16 Nokia

- 11.17 Samsung

- 11.18 TelcoBridges

- 11.19 VMware (Broadcom)

- 11.20 ZTE