|

市場調査レポート

商品コード

1698283

ユーティリティ向け分路リアクトル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Utility Scale Shunt Reactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ユーティリティ向け分路リアクトル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 126 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

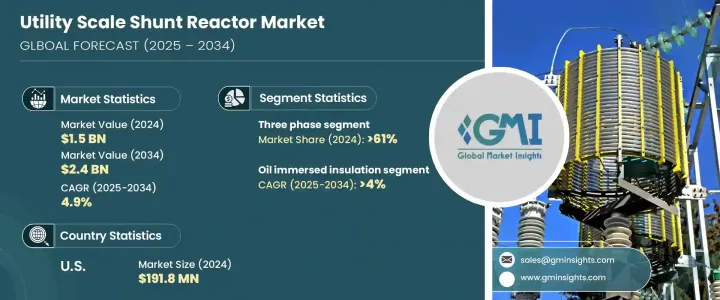

世界のユーティリティ向け分路リアクトル市場は、2024年に15億米ドルを生み出し、2025年から2034年にかけてCAGR 4.9%で拡大すると予測されています。

この着実な成長の背景には、世界のエネルギー需要の増加、老朽化した送電網の近代化、再生可能エネルギー源の急速な統合があります。各国が送電網の効率と信頼性を優先する中、分路リアクトルは電圧調整と電力管理で重要な役割を果たし、トランスミッションの損失を減らして全体的な送電網の安定性を高めています。電力消費の急増と再生可能エネルギー発電への移行に伴い、実用規模の分路リアクトルは進化する電力インフラにとって不可欠な要素になりつつあります。

送電網の改善を目的とした技術の進歩や政府の取り組みが、こうしたシステムの需要をさらに押し上げています。新興経済諸国は新しい電力インフラに多額の投資を行っているが、先進国は既存の送電網の近代化に注力しています。国境を越えた送電プロジェクトや超高圧送電線が、高度な分路リアクトル・ソリューションの採用を促進しています。電力会社がリアルタイムの監視・制御メカニズムの強化を目指す中、デジタル化・自動化された送電網システムの台頭も市場力学を形成する重要な動向です。さらに、持続可能なエネルギーの実践を支援する規制政策が、電力会社に効率的な電圧管理ソリューションの統合を促し、再生可能エネルギーの入力が変動しても安定した運用を保証しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 24億米ドル |

| CAGR | 4.9% |

市場は主に三相リアクトルと単相リアクトルの2つに区分されます。三相リアクトルは、2024年の市場シェア61%を占め、今後数年間で大きく成長する見込みです。三相リアクトルの普及は、超高圧トランスミッションの拡大と産業用グリッドの近代化に起因します。これらのリアクトルは、相互接続された送電網内の無効電力を管理し、効率を最適化し、トランスミッションの損失を最小限に抑えるために不可欠です。国境を越えた電力相互接続など、大規模なエネルギー・プロジェクトが拡大するにつれ、三相リアクトルの需要は増加の一途をたどっています。

絶縁タイプに基づき、市場は油浸リアクトルと空芯リアクトルに分けられます。油浸リアクトルは2024年に62.8%のシェアで市場をリードし、2034年まで4%の割合で安定成長すると予想されます。その優位性は、優れた冷却性能と高い信頼性によるもので、特に高電圧用途に適しています。世界の電力セクターが送電網の安定性と効率的な電圧調整に重点を置いているため、油入リアクトルへの嗜好は依然として強いです。トランス・オイル技術の進歩は、その魅力をさらに高め、電力会社が大電力トランスミッション・ネットワークで最適な性能を達成することを可能にしています。

米国のユーティリティ向け分路リアクトル市場は、2024年に1億9,180万米ドルと評価され、老朽化した送電網インフラのアップグレードが進むにつれて成長すると見られています。再生可能エネルギーへの依存度の高まりが、デジタル監視機能を含む高度な分路リアクトル技術の採用を加速させています。高圧送電網の拡張とスマートグリッドの開発は、米国のエネルギー部門における近代化という幅広い動向と一致し、市場の上昇軌道を強めています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:断熱材別、2021~2034年

- 主要動向

- 油浸

- 空芯

第7章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 固定分路リアクトル

- 可変分路リアクトル

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- CG Power &Industrial Solutions

- Fuji Electric

- GBE

- GE

- GETRA

- HICO America

- Hitachi Energy

- Hyosung Heavy Industries

- Nissin Electric

- SGB SMIT

- Shrihans Electricals

- Siemens Energy

- TMC Transformers

- Toshiba Energy Systems &Solutions Corporation

- WEG

The Global Utility Scale Shunt Reactor Market generated USD 1.5 billion in 2024 and is projected to expand at a CAGR of 4.9% between 2025 and 2034. This steady growth is fueled by the increasing demand for energy worldwide, the modernization of aging electrical grids, and the rapid integration of renewable energy sources. As countries prioritize grid efficiency and reliability, shunt reactors play a vital role in voltage regulation and power management, reducing transmission losses and enhancing overall grid stability. With the surge in electricity consumption and the transition toward renewable power generation, utility-scale shunt reactors are becoming an essential component of the evolving power infrastructure.

Technological advancements and government initiatives aimed at upgrading energy transmission networks are further boosting the demand for these systems. Emerging economies are heavily investing in new power infrastructure, while developed nations are focused on modernizing existing grids. Cross-border electricity transmission projects and ultra-high voltage transmission lines are driving the adoption of advanced shunt reactor solutions. The rise of digitalized and automated power grid systems is another key trend shaping market dynamics, as utilities seek to enhance real-time monitoring and control mechanisms. Additionally, regulatory policies supporting sustainable energy practices are prompting power companies to integrate efficient voltage management solutions, ensuring stable operations even with fluctuating renewable energy inputs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 4.9% |

The market is segmented into two primary categories: three-phase reactors and single-phase reactors. Three-phase reactors accounted for a dominant 61% market share in 2024 and are poised for significant growth over the coming years. Their widespread adoption stems from the expansion of ultra-high voltage transmission networks and industrial grid modernization. These reactors are essential in managing reactive power within interconnected power grids, optimizing efficiency, and minimizing transmission losses. As large-scale energy projects expand, including cross-border power interconnections, the demand for three-phase reactors continues to rise.

Based on insulation type, the market is divided into oil-immersed and air-core reactors. Oil-immersed reactors led the market with a 62.8% share in 2024 and are expected to grow steadily at a rate of 4% through 2034. Their dominance is attributed to their superior cooling performance and high reliability, making them particularly suitable for high-voltage applications. As the global power sector focuses on grid stability and efficient voltage regulation, the preference for oil-immersed reactors remains strong. The advancement of transformer oil technologies further enhances their appeal, allowing utilities to achieve optimal performance in high-power transmission networks.

U.S. utility scale shunt reactor market was valued at USD 191.8 million in 2024 and is set to grow as the country continues upgrading its aging grid infrastructure. The rising dependence on renewable energy sources is accelerating the adoption of advanced shunt reactor technologies, including digital monitoring capabilities. High-voltage transmission grid expansions and smart grid developments are reinforcing the market's upward trajectory, aligning with the broader trend of modernization within the U.S. energy sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Insulation, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Oil immersed

- 6.3 Air core

Chapter 7 Market Size and Forecast, By Product, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Fixed shunt reactors

- 7.3 Variable shunt reactors

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 CG Power & Industrial Solutions

- 9.2 Fuji Electric

- 9.3 GBE

- 9.4 GE

- 9.5 GETRA

- 9.6 HICO America

- 9.7 Hitachi Energy

- 9.8 Hyosung Heavy Industries

- 9.9 Nissin Electric

- 9.10 SGB SMIT

- 9.11 Shrihans Electricals

- 9.12 Siemens Energy

- 9.13 TMC Transformers

- 9.14 Toshiba Energy Systems & Solutions Corporation

- 9.15 WEG