|

市場調査レポート

商品コード

1698280

インクレチンベース医薬品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Incretin-based Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| インクレチンベース医薬品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

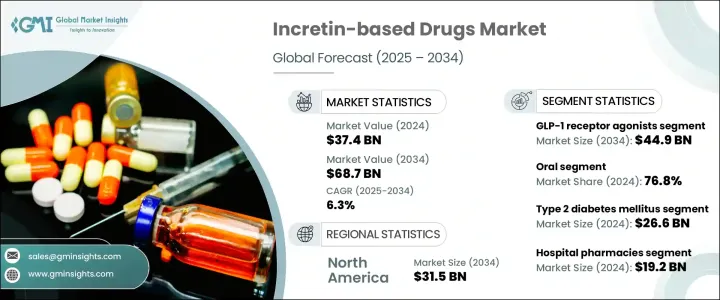

世界のインクレチンベース医薬品市場は、2024年に374億米ドルと評価され、2025年から2034年にかけてCAGR 6.3%で成長すると予測されています。

インクレチンベース医薬品は、食後の血糖値を調整する腸内ホルモンによってインスリン分泌を刺激することで、2型糖尿病の管理に役立ちます。主に肥満、高齢化、座りっぱなしのライフスタイルによる糖尿病有病率の増加は、市場拡大を促進する重要な要因です。患者意識の高まり、薬剤製剤の進歩、糖尿病治療へのアクセス向上が、この成長をさらに後押ししています。

市場は薬剤タイプ別にGLP-1受容体作動薬とDPP-4阻害薬に分類され、2023年の市場規模は355億米ドルです。GLP-1受容体作動薬に対する需要の高まりは、インスリン分泌を促進し、グルカゴン濃度を抑制して血糖値を効果的に管理するその能力によるものです。これらの薬剤はまた、食欲をコントロールし消化を遅らせることで体重減少を促進するため、糖尿病患者にとって好ましい選択肢となっています。週1回注射などの徐放性製剤は、患者の服薬アドヒアランスを向上させ、市場規模を拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 374億米ドル |

| 予測金額 | 687億米ドル |

| CAGR | 6.3% |

市場はまた、投与経路によって経口薬と注射薬に区分されます。経口剤セグメントは2024年に287億米ドルを占め、市場シェアは76.8%です。経口製剤は注射剤に代わる利便性を提供し、患者のコンプライアンス向上につながります。継続的な研究努力により、有効性と安全性のプロファイルが改善され、経口薬がますます好まれるようになっています。これらの製剤は、配布、保管、投与が容易であるため、ヘルスケア提供者の負担が軽減され、さまざまな医療現場での利用しやすさが向上しています。

適応症別には、2型糖尿病、肥満症および体重管理、その他の代謝異常症が含まれます。2型糖尿病セグメントが最大のシェアを占め、2024年の売上高は266億米ドルでした。2型糖尿病の世界の罹患率の上昇は、食生活の乱れや生活習慣の悪化に起因しており、インクレチンベース医薬品の需要を促進しています。これらの治療薬は、低血糖のリスクを軽減しながら効果的に血糖値を下げるため、高齢化した人々や血糖値の変動が激しい人々に安全な治療選択肢を提供します。

流通チャネルは、病院薬局、小売薬局、eコマースで構成されます。病院薬局は2024年の売上高が192億米ドルで市場をリードしています。このような環境では、特に新たに診断された患者や専門的な治療を必要とする患者にとって、薬への確実なアクセスが保証されます。薬剤師は用量、副作用、製剤の違いに関する指導を行い、治療のアドヒアランスを高める。投薬管理プログラムや治療反応の綿密なモニタリングなど、包括的なサポートサービスがさらに市場の成長に寄与しています。

北米が市場を独占し、2024年には171億米ドルを占め、米国が155億米ドルでトップです。糖尿病、心血管疾患、肥満の有病率の上昇が、インクレチンベース医薬品の需要を引き続き牽引しています。この地域の市場拡大には、支持的な規制の枠組みや医薬品開発の急速な進歩が寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 2型糖尿病有病率の上昇

- 非インスリン療法へのシフト

- ドラッグデリバリー技術の進歩

- 心血管と体重管理の利点

- 業界の潜在的リスク&課題

- 高い治療費

- 副作用と禁忌

- 促進要因

- 成長可能性分析

- 規制状況

- ギャップ分析

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- GLP-1受容体作動薬

- DPP-4阻害薬

第6章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口剤

- 注射剤

第7章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 2型糖尿病

- 肥満症および体重管理

- その他の代謝性疾患

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AstraZeneca

- Boehringer Ingelheim

- Eli Lilly and Company

- GlaxoSmithKline

- Lupin Limited

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceutical Company

- Viatris

The Global Incretin-Based Drugs Market was valued at USD 37.4 billion in 2024 and is predicted to grow at a CAGR of 6.3% from 2025 to 2034. Incretin-based drugs help manage type 2 diabetes by stimulating insulin secretion through gut hormones, which regulate blood sugar levels after meals. The growing prevalence of diabetes, primarily due to obesity, aging populations, and sedentary lifestyles, is a key factor driving market expansion. Increasing patient awareness, advancements in drug formulations, and improved accessibility to diabetes treatments further support this growth.

The market is categorized by drug type into GLP-1 receptor agonists and DPP-4 inhibitors, with a market size of USD 35.5 billion in 2023. The rising demand for GLP-1 receptor agonists is driven by their ability to enhance insulin secretion and suppress glucagon levels, effectively managing blood sugar. These drugs also promote weight loss by controlling appetite and slowing digestion, making them a preferred option for diabetes patients. Extended-release formulations, such as once-weekly injections, improve patient adherence and expand market reach.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.4 Billion |

| Forecast Value | $68.7 Billion |

| CAGR | 6.3% |

The market is also segmented by the route of administration into oral and injectable drugs. The oral segment accounted for USD 28.7 billion in 2024, with a market share of 76.8%. Oral formulations offer a convenient alternative to injections, leading to higher patient compliance. Continuous research efforts have led to improved efficacy and safety profiles, making oral medications increasingly preferred. These formulations are easy to distribute, store, and administer, reducing the burden on healthcare providers and enhancing accessibility across various healthcare settings.

By indication, the market includes type 2 diabetes mellitus, obesity and weight management, and other metabolic disorders. The type 2 diabetes mellitus segment held the largest share, generating USD 26.6 billion in revenue in 2024. The rising global incidence of type 2 diabetes, attributed to poor dietary habits and lifestyle factors, fuels the demand for incretin-based drugs. These medications effectively lower blood sugar levels while reducing the risk of hypoglycemia, offering a safer treatment option for aging populations and those prone to severe blood sugar fluctuations.

The distribution channel segment comprises hospital pharmacies, retail pharmacies, and e-commerce. Hospital pharmacies led the market with USD 19.2 billion in revenue in 2024. These settings ensure secure access to medications, particularly for newly diagnosed patients or those requiring specialized care. Pharmacists provide guidance on dosage, side effects, and formulation differences, enhancing treatment adherence. Comprehensive support services, including medication management programs and close monitoring of treatment responses, further contribute to market growth.

North America dominated the market, accounting for USD 17.1 billion in 2024, with the U.S. leading at USD 15.5 billion. The rising prevalence of diabetes, cardiovascular diseases, and obesity continues to drive demand for incretin-based drugs. Supportive regulatory frameworks and rapid advancements in drug development contribute to the region's market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of type 2 diabetes mellitus

- 3.2.1.2 Shift toward non-insulin therapies

- 3.2.1.3 Advancements in drug delivery technologies

- 3.2.1.4 Cardiovascular and weight management benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Adverse effects and contraindications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Pipeline analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 GLP-1 receptor agonists

- 5.3 DPP-4 inhibitors

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Type 2 diabetes mellitus

- 7.3 Obesity and weight management

- 7.4 Other metabolic disorders

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Boehringer Ingelheim

- 10.3 Eli Lilly and Company

- 10.4 GlaxoSmithKline

- 10.5 Lupin Limited

- 10.6 Merck

- 10.7 Novo Nordisk

- 10.8 Pfizer

- 10.9 Sanofi

- 10.10 Takeda Pharmaceutical Company

- 10.11 Viatris