スマートホームセキュリティカメラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Smart Home Security Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698264

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

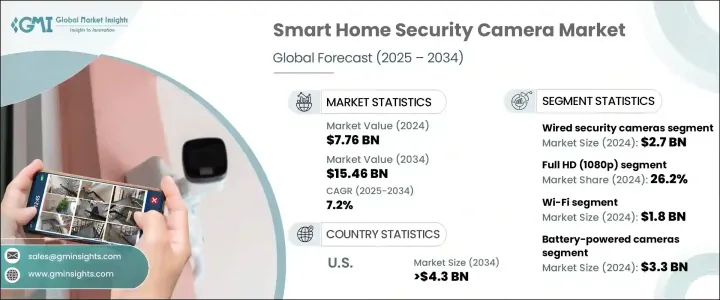

スマートホームセキュリティカメラの世界市場規模は2024年に77億6,000万米ドルとなり、2025年から2034年にかけてCAGR 7.2%で成長すると予測されています。

市場の拡大は、スマートホームデバイスの普及とセキュリティへの関心の高まりが大きな要因となっています。スマートカメラ、ロック、モーションセンサーは不可欠なものとなりつつあり、ホームオートメーションシステムとシームレスに統合しながら自宅を遠隔監視できるようになっています。5GネットワークとIoT技術の普及により、スマートセキュリティシステムの性能は大幅に向上しています。さらに、スマートフォンや音声アシスタントのユーザー数の増加が引き続き市場の成長を支えており、セキュリティ・ソリューションのシームレスな運用を可能にしています。セキュリティ脅威の高まりは、高解像度カメラ、クラウドストレージ、AIベースの脅威検出を特徴とする高度な監視ソリューションへのニーズをさらに高めています。

市場は有線セキュリティカメラと無線セキュリティカメラに分けられます。2024年、有線セキュリティカメラの評価額は27億米ドルでした。その人気の理由は、信頼性の向上、最適な電力供給、優れた映像品質です。さらに、パワー・オーバー・イーサネット(PoE)技術により、複数のセキュリティ機器の設置が簡素化されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 77億6,000万米ドル |

| 予測金額 | 154億6,000万米ドル |

| CAGR | 7.2% |

解像度別では、HD(720p)、フルHD(1080p)、2K、4K以上のカメラが含まれます。2024年の市場シェアはフルHD(1080p)カメラが26.2%を占める。これらのカメラは、信頼性の高い接続性とネットワークビデオレコーダーや集中監視システムとの互換性により、大規模物件や商業環境で広く使用されています。

同市場は、Wi-Fi、Bluetooth、ZigBeeなどの接続オプションによっても分類されます。Wi-Fi対応セキュリティカメラは、2024年に18億米ドルで市場をリードしています。Wi-Fi対応防犯カメラは、設置が簡単で、ホームネットワークとのシームレスな統合が可能であり、リモートアクセスも可能であるため、普及が進んでいます。メッシュWi-FiやデュアルバンドWi-Fi技術の開発により、信頼性が向上し、接続の問題やタイムラグが減少しています。

電源については、市場は電池式、プラグイン式、太陽電池式カメラで構成されています。2024年の評価額は33億米ドルで、バッテリー式カメラがこの分野を支配しています。ソーラー充電、AIによるエネルギー管理、リチウムイオンバッテリー技術の進歩により、屋内と屋外の両方で需要が高まっています。ポータブルでDIYに適したセキュリティ・ソリューションへの嗜好の高まりが、引き続き採用を後押ししています。

用途別では、屋内セキュリティが急成長を遂げており、CAGRは10.4%と予測されています。消費者も企業も、特に赤ちゃんやペットの監視、高齢者ケアのために、屋内監視ソリューションへの投資を増やしています。AIを活用した動体検知、顔認識、クラウドストレージは、こうしたセキュリティ・ソリューションの魅力をさらに高めています。

流通チャネル・セグメントには、オンライン販売、スーパーマーケット、ハイパーマーケット、専門店、家電量販店が含まれます。オンライン販売は2024年に支配的なセグメントとして浮上し、30億米ドルを生み出しました。eコマースへの嗜好が高まっている背景には、競争力のある価格設定、製品の多様性、価格比較の利便性があります。

米国市場は、犯罪率の上昇とスマート・セキュリティ・ソリューションの需要増に後押しされ、2034年には43億米ドルを超えると予想されています。ホームオートメーションや保険優遇措置とセキュリティシステムの統合が、市場拡大をさらに後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- スマートホームデバイスの普及拡大

- セキュリティに対する懸念の高まり

- 技術の進歩

- 接続性の向上とリアルタイム監視

- DIYによる設置と費用対効果

- 業界の潜在的リスク&課題

- 高額な初期費用と加入料

- 限られたインターネット接続と帯域幅の問題

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 有線セキュリティカメラ

- ワイヤレスセキュリティカメラ

第6章 市場推計・予測:解像度別、2021年~2034年

- 主要動向

- HD(720p)

- フルHD(1080p)

- 2K

- 4K以上

第7章 市場推計・予測:コネクティビティ別、2021~2034年

- 主要動向

- Wi-Fi

- Bluetooth

- Zigbee

- その他

第8章 市場推計・予測:動力源別、2021年~2034年

- 主要動向

- バッテリー駆動カメラ

- プラグインカメラ

- ソーラーカメラ

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 屋内セキュリティ

- 屋外セキュリティ

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン販売

- eコマース・プラットフォーム

- ブランドサイト

- スーパーマーケット/ハイパーマーケット

- 専門店

- 家電量販店

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- Abode Systems, Inc.

- ADT Inc.

- Arlo Technologies, Inc.

- Blink

- Canary Connect, Inc.

- D-Link Corporation

- Ecobee

- Eufy

- Frontpoint Security Solutions, LLC

- Google Nest

- Hikvision Digital Technology

- Lorex

- Reolink

- Ring

- Samsung Electronics Co., Ltd.

- SimpliSafe

- Synology

- TP-Link

- Ubiquiti Inc.

- Vivint Smart Home

- Wyze Labs, Inc.

- Xiaomi Inc.

- YI Technology

- Zmodo

目次

The Global Smart Home Security Camera Market was valued at USD 7.76 billion in 2024 and is projected to grow at a CAGR of 7.2% from 2025 to 2034. Market expansion is largely driven by the increasing adoption of smart home devices and heightened security concerns. Smart cameras, locks, and motion sensors are becoming essential, allowing users to monitor their homes remotely while seamlessly integrating with home automation systems. The widespread adoption of 5G networks and IoT technology has significantly enhanced the performance of smart security systems. Moreover, the growing number of smartphone and voice assistant users continues to support market growth, enabling seamless operation of security solutions. Rising security threats have further fueled the need for advanced surveillance solutions featuring high-definition cameras, cloud storage, and AI-based threat detection.

The market is divided into wired and wireless security cameras. In 2024, wired security cameras held a valuation of USD 2.7 billion. Their popularity stems from enhanced reliability, optimal power supply, and superior video quality. Additionally, Power over Ethernet (PoE) technology has simplified the installation of multiple security devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.76 Billion |

| Forecast Value | $15.46 Billion |

| CAGR | 7.2% |

By resolution, the market includes HD (720p), Full HD (1080p), 2K, and 4K & above cameras. Full HD (1080p) cameras accounted for 26.2% of the market share in 2024. They are widely used in large properties and commercial settings due to their reliable connectivity and compatibility with network video recorders and centralized monitoring systems.

The market is also categorized by connectivity options, including Wi-Fi, Bluetooth, and ZigBee. Wi-Fi-enabled security cameras led the market with USD 1.8 billion in 2024. Their increasing adoption is attributed to easy installation, seamless integration with home networks, and remote access. The development of mesh and dual-band Wi-Fi technology has improved reliability while reducing connectivity issues and lag.

Regarding power sources, the market consists of battery-powered, plug-in, and solar-powered cameras. Battery-powered cameras dominated the segment with a valuation of USD 3.3 billion in 2024. Their demand is rising for both indoor and outdoor use due to advancements in solar charging, AI-driven energy management, and lithium-ion battery technology. The increasing preference for portable, DIY-friendly security solutions continues to drive adoption.

In terms of application, indoor security is witnessing rapid growth, with a projected CAGR of 10.4%. Consumers and businesses alike are increasingly investing in indoor surveillance solutions, particularly for baby and pet monitoring, as well as elderly care. AI-powered motion detection, facial recognition, and cloud storage further enhance the appeal of these security solutions.

The distribution channel segment includes online sales, supermarkets, hypermarkets, specialty stores, and electronics retailers. Online sales emerged as the dominant segment in 2024, generating USD 3 billion. The growing preference for e-commerce is driven by competitive pricing, product variety, and convenient price comparisons.

The U.S. market is expected to exceed USD 4.3 billion by 2034, fueled by rising crime rates and increased demand for smart security solutions. The integration of security systems with home automation and insurance incentives is further supporting market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart home devices

- 3.2.1.2 Rising security concerns

- 3.2.1.3 Technological advancements

- 3.2.1.4 Improved connectivity and real-time monitoring

- 3.2.1.5 DIY installation and cost-effectiveness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost and subscription fees

- 3.2.2.2 Limited internet connectivity and bandwidth issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Wired security cameras

- 5.3 Wireless security cameras

Chapter 6 Market Estimates and Forecast, By Resolution, 2021 – 2034 (USD Mn)

- 6.1 Key trends

- 6.2 HD (720p)

- 6.3 Full HD (1080p)

- 6.4 2K

- 6.5 4K & Above

Chapter 7 Market Estimates and Forecast, By Connectivity, 2021 – 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Wi-Fi

- 7.3 Bluetooth

- 7.4 Zigbee

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Power Source, 2021 – 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Battery-powered cameras

- 8.3 Plug-in power cameras

- 8.4 Solar-powered cameras

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Mn)

- 9.1 Key trends

- 9.2 Indoor security

- 9.3 Outdoor security

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Mn)

- 10.1 Key trends

- 10.2 Online sales

- 10.2.1 E-commerce platforms

- 10.2.2 Brand websites

- 10.3 Supermarkets/Hypermarkets

- 10.4 Specialty stores

- 10.5 Electronics stores

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Abode Systems, Inc.

- 12.2 ADT Inc.

- 12.3 Arlo Technologies, Inc.

- 12.4 Blink

- 12.5 Canary Connect, Inc.

- 12.6 D-Link Corporation

- 12.7 Ecobee

- 12.8 Eufy

- 12.9 Frontpoint Security Solutions, LLC

- 12.10 Google Nest

- 12.11 Hikvision Digital Technology

- 12.12 Lorex

- 12.13 Reolink

- 12.14 Ring

- 12.15 Samsung Electronics Co., Ltd.

- 12.16 SimpliSafe

- 12.17 Synology

- 12.18 TP-Link

- 12.19 Ubiquiti Inc.

- 12.20 Vivint Smart Home

- 12.21 Wyze Labs, Inc.

- 12.22 Xiaomi Inc.

- 12.23 YI Technology

- 12.24 Zmodo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日