エンタープライズモニタリング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Enterprise Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698250

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

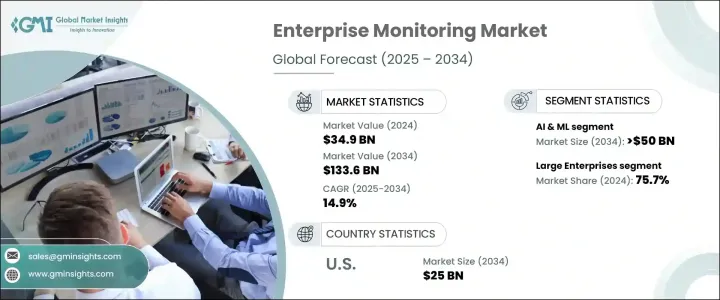

世界のエンタープライズモニタリング市場は大きく成長し、2024年には349億米ドルに達し、2025年から2034年までのCAGRは14.9%で拡大すると予測されています。

企業がハイブリッド環境やマルチクラウド環境に適応し続けるにつれ、複雑なITインフラの管理はますます困難になっています。エンタープライズモニタリング・サービスは、これらのシステムに不可欠な可視性を提供し、企業が潜在的な問題にプロアクティブに対処し、ワークフローを最適化し、業務効率を改善するのを支援します。これらのサービスに対する需要は、継続的なアップタイム、リソース利用率の向上、効果的な問題解決の必要性によって急増しています。

企業がデジタルフットプリントを強化する中、監視ソリューションはダウンタイムを最小限に抑え、システムの信頼性を確保する上で重要な役割を果たしています。サイバー脅威の高度化に伴い、企業は業界規制へのコンプライアンスを維持し、機密データを保護するために、高度なサイバーセキュリティ・モニタリング・ツールを利用するようになっています。これらのツールは、リアルタイムの脅威検出、侵害の特定、脆弱性の監視を提供し、組織のIT環境の安全確保を支援します。AIと機械学習(AI/ML)技術の台頭は企業モニタリング分野に大きな影響を与えており、AI主導のソリューションは現在、重要なタスクを自動化し、異常検知を改善し、潜在的なシステム障害を予測しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 349億米ドル |

| 予測金額 | 1,336億米ドル |

| CAGR | 14.9% |

同市場ではまた、AIを活用した観測可能性ツールへの依存が高まっています。このツールは、ITパフォーマンスに関するより深い洞察を提供し、問題が深刻化する前にその根本原因を特定するのに役立ちます。このような進歩により、企業のITインフラ管理方法は一変し、企業は事後対応型から事前対応型の管理アプローチに移行できるようになりました。さらに、AIOpsの動向は、根本原因の分析やアプリケーション・パフォーマンスの最適化に機械学習を活用することで、運用効率を高めています。このような進化により、企業は問題の検出と解決が容易になり、ITシステムの円滑な稼動が保証されるようになっています。

エンタープライズモニタリング市場は、組織の規模によってさらに細分化され、大企業が圧倒的なシェアを占めています。これらの企業は、大規模なITシステムを効率的に管理するために、包括的な監視ソリューションを必要としています。クラウドベースでAIと統合された監視プラットフォームは、その拡張性と柔軟性から人気が高まっています。これらのツールは、大規模なオンサイト・インフラを必要とせずに、企業がパフォーマンスを監視し、データを分析し、異常を検出するのに役立ちます。

北米は世界市場をリードし、2024年には市場シェアの40%以上を占め、米国は2034年までに250億米ドルに達する見通しです。同地域は、AIベースのモニタリング、サイバーセキュリティ・ソリューション、クラウド・コンピューティング技術への高額の投資による恩恵を受けており、これらは引き続き市場拡大の原動力となっています。さらに、ヘルスケアや金融などの主要セクターにおけるITインフラストラクチャのセキュリティ強化に向けた取り組みが、市場のさらなる成長に拍車をかけています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テクノロジー&インフラストラクチャープロバイダー

- エンタープライズモニタリング・ソフトウェア開発企業

- システムインテグレーターとマネージドサービスプロバイダー

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 促進要因

- クラウドコンピューティングとハイブリッドIT環境の採用の増加

- サイバーセキュリティとコンプライアンス監視のニーズの高まり

- ITインフラの複雑化

- DevOpsと継続的モニタリングに対する需要の高まり

- エンドユーザー・エクスペリエンスのモニタリングに対する需要の高まり

- 業界の潜在的リスク&課題

- 高い導入コストとメンテナンスコスト

- マルチクラウドとハイブリッド環境の管理の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- AIとML

- ビッグデータ分析

- IoTとエッジコンピューティング

- ブロックチェーン

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- インフラモニタリング

- アプリケーションパフォーマンス監視

- セキュリティモニタリング

- ネットワーク・モニタリング

- データベース監視

- 従業員モニタリング

- サービス

- マネージドサービス

- プロフェッショナルサービス

第9章 市場推計・予測:データ別、2021年~2034年

- 主要動向

- リアルタイムデータ監視

- ヒストリカル・データ・モニタリング

- 構造化データモニタリング

- 非構造化データモニタリング

第10章 市場推計・予測:エンドユース別、2021年~2034年

- 主要動向

- 小売・eコマース

- BFSI

- IT・通信

- ヘルスケア

- 運輸・物流

- 製造業

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- BMC Software

- Cisco

- Coralogic

- Datadog

- Dynatrace

- Elastic N.V.

- Grafana Labs

- IBM

- LogicMonitor

- Microsoft

- Nagios

- New Relic

- Oracle

- Paessler

- Pandora FMS

- ScienceLogic

- SolarWinds

- Trianz

- VirtualMetric

- Zoho

目次

The Global Enterprise Monitoring Market is projected to grow significantly, reaching USD 34.9 billion in 2024 and expanding at a CAGR of 14.9% from 2025 to 2034. As organizations continue to adapt to hybrid and multi-cloud environments, managing complex IT infrastructures becomes increasingly difficult. Enterprise monitoring services provide essential visibility into these systems, helping businesses proactively address potential issues, optimize workflows, and improve operational efficiency. The demand for these services has surged, driven by the need for continuous uptime, enhanced resource utilization, and effective issue resolution.

As companies enhance their digital footprint, monitoring solutions play a vital role in minimizing downtime and ensuring system reliability. With the growing sophistication of cyber threats, businesses are increasingly turning to advanced cybersecurity monitoring tools to maintain compliance with industry regulations and protect sensitive data. These tools provide real-time threat detection, breach identification, and vulnerability monitoring, helping organizations secure their IT environments. The rise of AI and machine learning (AI/ML) technologies has significantly impacted the enterprise monitoring sector, with AI-driven solutions now automating key tasks, improving anomaly detection, and predicting potential system failures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.9 Billion |

| Forecast Value | $133.6 Billion |

| CAGR | 14.9% |

The market is also witnessing a growing reliance on AI-powered observability tools, which offer deeper insights into IT performance and help identify root causes of issues before they escalate. These advancements have transformed how businesses manage their IT infrastructure, allowing them to shift from reactive to proactive management approaches. Additionally, the growing trend of AIOps is enhancing operational efficiency by leveraging machine learning for root-cause analysis and optimizing application performance. This evolution is making it easier for organizations to detect and resolve issues, ensuring that their IT systems run smoothly.

The enterprise monitoring market is further segmented by organization size, with large enterprises holding a dominant share. These businesses require comprehensive monitoring solutions to manage their expansive IT systems effectively. Cloud-based and AI-integrated monitoring platforms are becoming increasingly popular due to their scalability and flexibility. These tools help businesses monitor performance, analyze data, and detect anomalies without the need for extensive on-site infrastructure.

North America leads the global market, accounting for more than 40% of the market share in 2024, with the U.S. poised to reach USD 25 billion by 2034. The region benefits from high investments in AI-based monitoring, cybersecurity solutions, and cloud computing technologies, which continue to drive market expansion. Additionally, initiatives aimed at enhancing IT infrastructure security in key sectors, including healthcare and finance, are fueling further market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology & infrastructure providers

- 3.2.2 Enterprise monitoring software developers

- 3.2.3 System integrators & managed service providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising adoption of cloud computing & hybrid IT environments

- 3.8.1.2 Growing need for cybersecurity & compliance monitoring

- 3.8.1.3 Increasing complexity of IT infrastructure

- 3.8.1.4 Rising demand for DevOps & continuous monitoring

- 3.8.1.5 Increased demand for end-user experiences monitoring

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High implementation & maintenance costs

- 3.8.2.2 Complexity in managing multi-cloud & hybrid environments

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Cloud

- 5.3 On-premises

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 AI & ML

- 6.3 Big data analytics

- 6.4 IoT & edge computing

- 6.5 Blockchain

Chapter 7 Market Estimates & Forecast, By Organization size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprise

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Software

- 8.2.1 Infrastructure monitoring

- 8.2.2 Application performance monitoring

- 8.2.3 Security monitoring

- 8.2.4 Network monitoring

- 8.2.5 Database monitoring

- 8.2.6 Workforce monitoring

- 8.3 Services

- 8.3.1 Managed services

- 8.3.2 Professional services

Chapter 9 Market Estimates & Forecast, By Data, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Real-time data monitoring

- 9.3 Historical data monitoring

- 9.4 Structured data monitoring

- 9.5 Unstructured data monitoring

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 Retail & e-commerce

- 10.3 BFSI

- 10.4 IT & telecom

- 10.5 Healthcare

- 10.6 Transportation & logistics

- 10.7 Manufacturing

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 BMC Software

- 12.2 Cisco

- 12.3 Coralogic

- 12.4 Datadog

- 12.5 Dynatrace

- 12.6 Elastic N.V.

- 12.7 Grafana Labs

- 12.8 IBM

- 12.9 LogicMonitor

- 12.10 Microsoft

- 12.11 Nagios

- 12.12 New Relic

- 12.13 Oracle

- 12.14 Paessler

- 12.15 Pandora FMS

- 12.16 ScienceLogic

- 12.17 SolarWinds

- 12.18 Trianz

- 12.19 VirtualMetric

- 12.20 Zoho

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日