|

市場調査レポート

商品コード

2019248

カキおよびアサリの市場機会、成長要因、業界動向分析、および2026年~2035年の予測Oyster and Clam Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| カキおよびアサリの市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月23日

発行: Global Market Insights Inc.

ページ情報: 英文 187 Pages

納期: 2~3営業日

|

概要

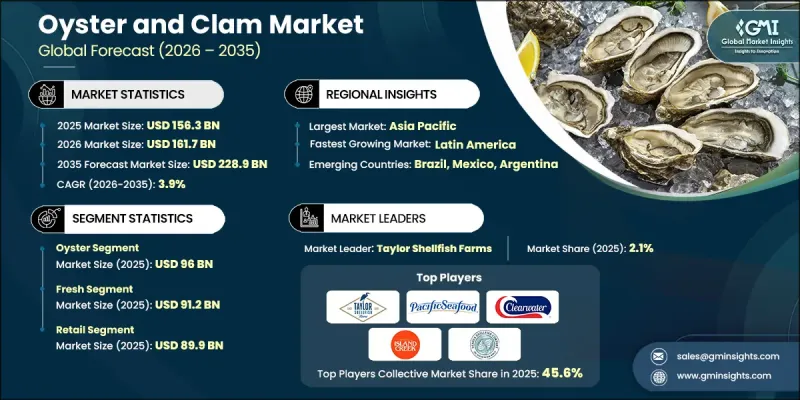

世界のカキ・アサリ市場は、2025年に1,563億米ドルと評価され、CAGR 3.9%で成長し、2035年までに2,289億米ドルに達すると推定されています。

二枚貝に分類されるカキとアサリは、内臓を保護する二つの貝殻を持つ構造が特徴です。カキは海水や汽水域の表面に付着して生息しますが、アサリは海岸線や淡水域の砂地や泥地に潜って生息することを好みます。両種とも自然のろ過摂食者としての役割を果たし、プランクトンや栄養分を捕食することで水質を改善します。カキは真珠の生産という点で市場においてさらに重要な意義を持ち、一方、アサリは料理への幅広い活用が評価されています。これらの貝類は、重要な生態学的便益をもたらしています。カキの礁は海洋生物の生息地となり水質を改善する一方、アサリが土中に穴を掘ることで土壌の通気性を高め、栄養分を循環させ、底生生態系を支えています。これらの存在は、バランスの取れた健全な水生環境の確かな指標であり、その生態学的および経済的価値を裏付けています。水産物への需要の高まり、持続可能な養殖、そして環境面での恩恵に対する認識の高まりが、世界市場の成長を牽引しています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 1,563億米ドル |

| 予測金額 | 2,289億米ドル |

| CAGR | 3.9% |

カキ市場は2025年に960億米ドルに達し、その独特の風味と食感により業界を牽引しています。その供給は天然漁獲と養殖の両方によって維持されており、年間を通じて安定した供給が確保されています。アサリはそのまろやかな味わいで、スープ、パスタ、レトルト食品、その他の料理に広く使用されており、業務用および家庭用の厨房において欠かせない食材となっています。アサリは様々な料理に幅広く活用できるため、カキと同様に安定した需要を生み出しています。

小売セグメントは2025年に899億米ドルを占め、カキとアサリの主要な販売チャネルとして台頭しました。スーパーマーケット、魚介類専門店、オンラインプラットフォームは、消費者に多様な商品ラインナップとパッケージ形態へのアクセスを提供しています。小売業者は、製品の品質を維持し鮮度を確保するために、保管、表示、陳列方法に注力しており、便利で高品質な貝類を求める都市部や内陸部の購入者のニーズに応えています。

米国のカキおよびアサリ市場は、水産物の消費増加と、持続可能な漁業および養殖手法への意識の高まりに牽引され、2025年には333億米ドルに達しました。生産者は、レストラン、小売業者、および地元市場からの需要に応えるため、安定した製品の供給に注力しています。品質基準を維持しつつ安定した供給を確保するには、持続可能な養殖手法が不可欠です。生産者と流通業者の連携は、販売範囲の拡大、製品の品質安定化、そして責任ある調達による新鮮なカキやアサリに対する消費者の信頼強化に寄与しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 水産物への需要の高まりが、カキやアサリの消費を後押ししています

- 近代的な養殖技術は、成長と疾病抵抗性を向上させます

- 持続可能な農業は長期的な生産を支えます

- 落とし穴・課題

- 水質汚染は貝類の健康に悪影響を及ぼします

- 過剰採取は野生個体群を減少させます

- 機会

- エコツーリズムおよび貝類フェスティバル

- バイオテクノロジーは収量と品質を向上させます

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術・イノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:タイプ別、2022-2035

- カキ

- アサリ

第6章 市場推計・予測:形態別、2022-2035

- 生鮮

- 冷凍

- 缶詰

第7章 市場推計・予測:流通チャネル別、2022-2035

- 小売り

- 外食産業

- その他

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Clearwater Seafoods

- Colville Bay Oyster Co. Ltd

- Five Star Shellfish Inc

- Island Creek Oysters

- Pacific Seafood

- Pangea Shellfish Company

- Royal Hawaiian Seafood

- Taylor Shellfish Farms

- Ward Oyster Company

- Woodstown Bay Shellfish Ltd