電気絶縁材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Electrical Insulation Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685213

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

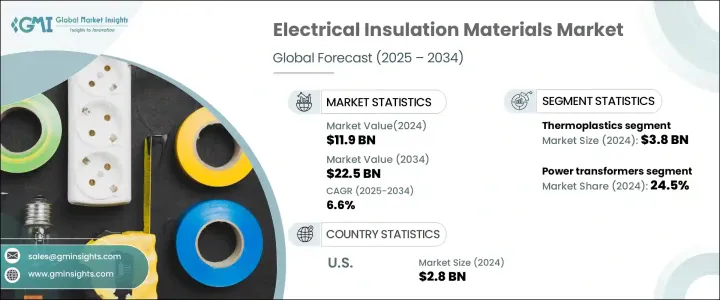

世界の電気絶縁材料市場は2024年に119億米ドルに達し、2025年から2034年にかけてCAGR 6.6%で拡大する見通しです。

この成長の原動力となっているのは、さまざまな産業で効率的で信頼性が高く、安全な電気システムへの需要が高まっていることです。電気絶縁材料は、電気部品の保護、寿命の確保、商用および産業用アプリケーションにおけるシステム性能の強化において重要な役割を果たしています。

産業が発展するにつれ、より厳しい規制や性能基準を満たすために、革新的で耐久性があり、持続可能な絶縁ソリューションに対するニーズが高まっています。エネルギー効率と持続可能性の重視の高まりとともに、材料技術の進歩が需要をさらに促進しています。インフラ、特に再生可能エネルギーと近代化された電力網の継続的な拡大も、市場の明るい見通しに寄与しています。環境に優しいソリューションへのシフトが進む中、メーカーは性能を向上させるだけでなく、環境に配慮した製品を提供することに注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 119億米ドル |

| 予測金額 | 225億米ドル |

| CAGR | 6.6% |

材料タイプ別に見ると、熱硬化性樹脂、ガラス繊維、マイカ、セラミック、熱可塑性樹脂、セルロース、綿、その他があります。2024年には、熱可塑性プラスチック部門が38億米ドルを生み出しました。熱硬化性樹脂は、その卓越した耐久性と高温耐性で知られ、要求の厳しい用途で人気の高い選択肢となっています。セラミックは、高電圧動作に理想的な優れた誘電特性で高く評価され、ガラス繊維は強度と優れた絶縁能力を提供します。マイカは、耐熱性と電気的保護の両方を提供し、高電圧環境で好まれる材料であり続けています。さらに、セルロースと綿は、耐火性を提供する環境に優しい材料として台頭してきており、電気分野における持続可能で安全なソリューションの増加傾向に合致しています。

電気絶縁材料の用途は幅広く、電力変圧器、配電変圧器、電気モーターと発電機、電線とケーブル、開閉装置、バッテリー、サーキットブレーカーなどの産業にサービスを提供しています。電力変圧器は2024年に市場シェアの24.5%を占め、2034年まで力強い成長が見込まれます。絶縁材料は配電変圧器や電気モーターの性能と効率を最適化するために極めて重要であり、発電、送電、産業オートメーションなどの重要なセクター全体の需要をさらに押し上げています。

米国では、電気絶縁材料市場は2024年に28億米ドルに達し、インフラへの多額の投資により大幅な成長が見込まれています。時代遅れの送電網を近代化し、再生可能エネルギーへの取り組みを拡大することが、高度な絶縁材料の採用を促進しています。持続可能性とエネルギー効率に優れたソリューションに重点を置く米国は、この地域市場の主要プレーヤーであり続け、予測期間を通じて継続的な成長を確保する構えです。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 自動車産業における需要の増加

- 航空宇宙用途での採用増加

- 化学加工産業の成長

- 業界の潜在的リスク&課題

- 電気絶縁材料の高コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:材料別、2021~2034年

- 主要動向

- フルオロカーボンエラストマー(FKM)

- 電気絶縁材料(FFKM)

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- シールとガスケット

- Oリング

- ホースとチューブ

- その他

第7章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙

- 石油・ガス

- 化学処理

第8章 市場規模・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M

- AGC(Asahi Glass)

- Chemours

- Daikin Industries

- DowDuPont

- DuPont(E. I. du Pont de Nemours and Company)

- Gujarat Fluorochemicals

- HaloPolymer

- Mitsui Chemicals

- Momentive Performance Materials

- Saint-Gobain Performance Plastics

- Shin-Etsu Chemical

- Solvay

- Wacker Chemie

- Zeon Corporation

目次

The Global Electrical Insulation Materials Market reached USD 11.9 billion in 2024 and is set to expand at a CAGR of 6.6% from 2025 to 2034. This growth is driven by the increasing demand for efficient, reliable, and safe electrical systems across various industries. Electrical insulation materials play a critical role in protecting electrical components, ensuring longevity, and enhancing system performance in both commercial and industrial applications.

As industries evolve, there is a rising need for innovative, durable, and sustainable insulation solutions to meet stricter regulations and performance standards. Advancements in material technology, along with a growing emphasis on energy efficiency and sustainability, are further fueling demand. The continued expansion of infrastructure, particularly in renewable energy and modernized electrical grids, is also contributing to the positive market outlook. With the ongoing shift toward eco-friendly solutions, manufacturers are focusing on providing products that not only improve performance but are also environmentally responsible.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.9 Billion |

| Forecast Value | $22.5 Billion |

| CAGR | 6.6% |

Based on material type, the market segments include thermosets, fiberglass, mica, ceramics, thermoplastics, cellulose, cotton, and others. In 2024, the thermoplastics segment generated USD 3.8 billion. Thermosets are known for their exceptional durability and high-temperature resistance, making them a popular choice in demanding applications. Ceramics are highly valued for their superior dielectric properties, ideal for high-voltage operations, while fiberglass provides strength and excellent insulation capabilities. Mica remains a preferred material in high-voltage environments, providing both heat resistance and electrical protection. Additionally, cellulose and cotton are emerging as eco-friendly materials that offer fire resistance, aligning with the growing trend of sustainable and safe solutions in the electrical sector.

The applications of electrical insulation materials are wide-ranging, serving industries like power transformers, distribution transformers, electrical motors and generators, wires and cables, switchgear, batteries, and circuit breakers. Power transformers accounted for 24.5% of the market share in 2024, with strong growth expected through 2034. Insulation materials are crucial for optimizing the performance and efficiency of distribution transformers and electrical motors, further boosting demand across critical sectors such as power generation, transmission, and industrial automation.

In the U.S., the electrical insulation materials market reached USD 2.8 billion in 2024 and is expected to grow significantly due to substantial investments in infrastructure. Modernizing outdated electrical grids and expanding renewable energy initiatives are driving the adoption of advanced insulation materials. With a focus on sustainability and energy-efficient solutions, the U.S. is poised to remain a major player in the regional market, ensuring continued growth throughout the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand in automotive industry

- 3.6.1.2 Rising adoption in aerospace applications

- 3.6.1.3 Growing chemical processing industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of electrical insulation materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fluorocarbon elastomers (FKM)

- 5.3 Perelectrical insulation materials (FFKM)

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Seals and gaskets

- 6.3 O-rings

- 6.4 Hoses and tubings

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use Industries, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Oil & gas

- 7.5 Chemical processing

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 AGC (Asahi Glass)

- 9.3 Chemours

- 9.4 Daikin Industries

- 9.5 DowDuPont

- 9.6 DuPont (E. I. du Pont de Nemours and Company)

- 9.7 Gujarat Fluorochemicals

- 9.8 HaloPolymer

- 9.9 Mitsui Chemicals

- 9.10 Momentive Performance Materials

- 9.11 Saint-Gobain Performance Plastics

- 9.12 Shin-Etsu Chemical

- 9.13 Solvay

- 9.14 Wacker Chemie

- 9.15 Zeon Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日