|

市場調査レポート

商品コード

1685207

防火材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Fire Stopping Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 防火材料市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月03日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

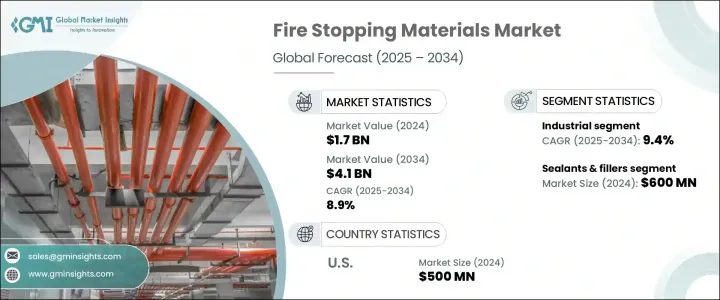

世界の防火材料市場は2024年に17億米ドルに達し、2025年から2034年までのCAGRは8.9%と、力強い成長が予測されています。

火災安全規制の強化、建設活動の急増、世界の都市化と工業化率の上昇など、いくつかの主要要因がこの市場拡大の原動力となっています。さらに、防火技術の進歩や防火安全に対する意識の高まりが、様々な分野における防火材料の需要をさらに高めています。石油・ガス、航空宇宙、海洋、データセンターなどの業界では、リスクが高いため厳しい防火要件が課せられています。

有望な成長軌道にもかかわらず、市場は大きな課題に直面しています。主なハードルのひとつは、高度な火災停止ソリューションに関連する高コストで、特に中小企業にとっては導入が阻害される可能性があります。また、地域によって規制の枠組みに一貫性がないという問題もあり、メーカーとエンドユーザーのコンプライアンスを複雑にしています。サプライチェーンの混乱や、初期コストを抑えられる代替素材との競合が、市場の複雑さをさらに高めています。また、建設業界の減速や熟練労働者の不足といった経済的な不確実性も、市場の安定した成長を達成する上での課題となっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 8.9% |

防火材料分野、特にシーラントと充填材のカテゴリーは、2024年に6億米ドルを占め、2034年までCAGR 9.4%で成長すると予測されます。シーリング材と充填材の技術革新がこの成長の主な鍵となっており、メーカーは性能の向上、塗布の容易さ、耐久性の向上を実現する製品を継続的に開発しています。特に浸透性シーリング材は、高温下で膨張して隙間を効果的に塞ぎ、火災の拡大を防ぐことから人気を集めています。防火モルタルもまた、特に耐火壁や床のケーブル、ダクト、パイプ周辺の大きな開口部を密閉する上で重要な役割を果たしており、これにより商業・工業環境における防火需要の高まりに対応しています。

2024年に防火材料市場の49%を占めた工業セクターは、2025年から2034年にかけてCAGR 9.4%で成長すると予測されています。この成長の背景には、石油・ガス施設、化学工場、製造現場といったリスクの高い環境における厳しい火災安全規制があります。可燃性の化学薬品、ガス、重機械が存在するため、これらの業務における延焼を防ぐ必要性は極めて重要です。これらの産業が拡大し続けるにつれ、防火資材の需要は増加の一途をたどると思われます。

米国では、2024年に5億米ドルの売上があり、2034年までCAGR 9.2%で成長すると予想されています。同国の成長は、火災安全基準の厳格化、建設業界の活況、受動的防火技術の継続的進歩に起因しています。改修、改築、重要インフラの保護に重点が置かれていることも、同地域の市場の力強い上昇傾向をさらに後押ししています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 火災安全規制の強化

- 建設、都市化、工業化の進展

- 業界の潜在的リスク&課題

- 防火材料の高コスト

- 熟練労働者の不足

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- コーティング剤

- シーラント&フィラー

- シリコン系シーラント

- アクリル系シーラント

- 浸透性シーラント

- その他(セメント系フィラーなど)

- シート・ボード

- ミネラルウールボード

- 蓄熱シート

- 複合ボード

- その他(石膏系ボードなど)

- パテ・フォーム

- 耐火パテ

- 耐火フォーム

- 発泡スチロール

- その他(パテパッド等)

- その他(カラー、防火ブロックなど)

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 受動的防火

- 能動的防火

第7章 市場推計・予測:火災等級別、2021~2034年

- 主要動向

- 1時間耐火

- 2時間耐火

- 3時間耐火

- 4時間耐火

- 4時間耐火超

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 電気

- 機械

- 配管

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業

- 産業

- 石油・ガス

- 自動車

- 製造業

- データセンター

- その他(自動車、海洋など)

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第11章 地域別市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- 3M

- Bostik

- Emseal Joint Systems

- Everkem

- Flame Stop

- Fosroc

- H. B. Fuller Company

- Hilti

- Promat

- RectorSeal

- Rockwool

- Sika

- Specified Technologies

- Tremco

- Unique Fire Stop Products

The Global Fire Stopping Materials Market reached USD 1.7 billion in 2024 and is projected to experience robust growth, with a CAGR of 8.9% from 2025 to 2034. Several key factors are driving this market expansion, including tightening fire safety regulations, a surge in construction activities, and the increasing rate of urbanization and industrialization worldwide. Additionally, advancements in fire stopping technologies and heightened awareness surrounding fire safety further fuel the demand for fire stopping materials across various sectors. The need for these materials is especially prominent in industries such as oil and gas, aerospace, marine, and data centers, all of which have strict fire safety requirements due to the high-risk nature of their operations.

Despite the promising growth trajectory, the market faces significant challenges. One of the primary hurdles is the high cost associated with advanced fire stopping solutions, which can inhibit adoption, particularly for small and medium-sized enterprises. There is also the issue of inconsistent regulatory frameworks across different regions, which complicates compliance for manufacturers and end-users alike. Supply chain disruptions and competition from alternative materials, which can offer lower initial costs, further add to the market's complexities. Economic uncertainties, such as slowdowns in the construction industry and the ongoing shortage of skilled labor, also pose challenges to achieving consistent growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 8.9% |

The fire stopping materials segment, specifically the sealants and fillers category, accounted for USD 600 million in 2024 and is expected to grow at a CAGR of 9.4% through 2034. Innovation in sealants and fillers has been key to this growth, with manufacturers continuously developing products that offer enhanced performance, easier application, and greater durability. Intumescent sealants, in particular, are gaining popularity as they expand under high temperatures to effectively seal gaps and prevent the spread of fire. Firestopping mortars also play a crucial role, particularly in sealing large openings around cables, ducts, and pipes in fire-rated walls and floors, thereby addressing the growing demand for fire protection in commercial and industrial settings.

The industrial sector, which accounted for 49% of the fire stopping materials market in 2024, is projected to grow at a CAGR of 9.4% between 2025 and 2034. This growth is driven by stringent fire safety regulations in high-risk environments such as oil and gas facilities, chemical plants, and manufacturing sites. The need to prevent fire spread in these operations is critical due to the presence of flammable chemicals, gases, and heavy machinery. As these industries continue to expand, the demand for fire stopping materials will only increase.

In the U.S., the fire stopping materials market generated USD 500 million in 2024 and is expected to grow at a CAGR of 9.2% through 2034. The country's growth is attributed to stricter fire safety standards, a booming construction industry, and ongoing advancements in passive fire protection technologies. The focus on retrofitting, renovations, and protecting critical infrastructure further supports the strong upward trend of the market in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Stricter fire safety regulations

- 3.6.1.2 Increased construction, urbanization, and industrialization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of fire stopping materials

- 3.6.2.2 Inadequate skilled labor

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Coatings

- 5.3 Sealants & fillers

- 5.3.1 Silicone-based sealants

- 5.3.2 Acrylic sealants

- 5.3.3 Intumescent sealants

- 5.3.4 Others (cementitious fillers etc.)

- 5.4 Sheets & boards

- 5.4.1 Mineral wool boards

- 5.4.2 Intumescent sheets

- 5.4.3 Composite boards

- 5.4.4 Others (gypsum-based boards etc.)

- 5.5 Putty & foam

- 5.5.1 Intumescent putty

- 5.5.2 Fire-rated foam

- 5.5.3 Expanding foam

- 5.5.4 Others (putty pads etc.)

- 5.6 Others (collars, fire blocks etc.)

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Passive fire protection

- 6.3 Active fire protection

Chapter 7 Market Estimates & Forecast, By Fire Rating, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 1-hour rated

- 7.3 2-hour rated

- 7.4 3-hour rated

- 7.5 4-hour rated

- 7.6 More than 4-hour rated

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Electrical

- 8.3 Mechanical

- 8.4 Plumbing

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

- 9.4.1 Oil & gas

- 9.4.2 Automotive

- 9.4.3 Manufacturing

- 9.4.4 Data centers

- 9.4.5 Others (automotive, marine etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 Bostik

- 12.3 Emseal Joint Systems

- 12.4 Everkem

- 12.5 Flame Stop

- 12.6 Fosroc

- 12.7 H. B. Fuller Company

- 12.8 Hilti

- 12.9 Promat

- 12.10 RectorSeal

- 12.11 Rockwool

- 12.12 Sika

- 12.13 Specified Technologies

- 12.14 Tremco

- 12.15 Unique Fire Stop Products