|

市場調査レポート

商品コード

1685188

内分泌検査市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Endocrine Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 内分泌検査市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

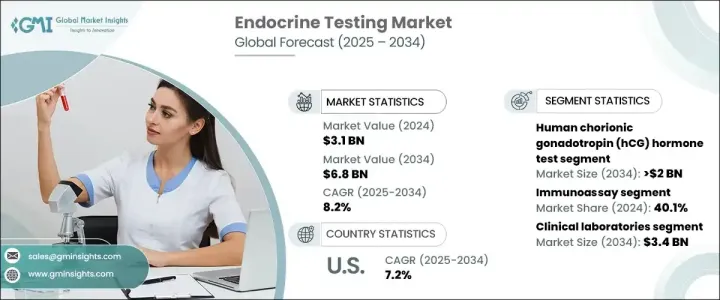

世界の内分泌検査市場は、2024年に31億米ドルと評価され、2025年から2034年までのCAGRは8.2%と予測され、大きな成長が見込まれています。

この成長の原動力は、内分泌疾患の有病率の上昇、定期健康診断に対する意識の高まり、ヘルスケアへのアクセス向上を目的とした政府の支援イニシアティブなど、いくつかの要因です。予防医療が重視されるようになったことで、特に糖尿病や甲状腺疾患などの慢性疾患を管理する人々の間で内分泌検査の需要が急増しています。

診断ツールの技術的進歩と検査サービスへのアクセスの向上が、市場の拡大をさらに加速しています。ポイント・オブ・ケア診断や個別化ヘルスケアソリューションなどの革新的な検査法の統合もまた、内分泌検査をより身近で効率的なものにし、状況を変えつつあります。世界中のヘルスケアシステムが内分泌関連疾患の早期発見と管理を優先していることから、市場は予測期間中に持続的な成長を遂げると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 31億米ドル |

| 予測金額 | 68億米ドル |

| CAGR | 8.2% |

様々な検査タイプの中で、ヒト絨毛性ゴナドトロピン(hCG)ホルモン検査はCAGR 7.6%で成長し、2034年には20億米ドルに達すると予測されています。妊娠検出に広く使用されているhCG検査は、その正確さと使いやすさで支持されています。これらの検査は、臨床現場でも家庭でも容易に入手できるため、信頼できる妊娠確認を求める個人にとって便利な選択肢となっています。これらの検査の採用が増加しているのは、ユーザーフレンドリーで正確な診断ソリューションに対する需要の高まりを反映しています。

市場は最終用途別に区分され、2024年には臨床検査室が最大のシェアを占める。このセグメントは2034年までに34億米ドルに達すると予測されています。臨床検査室には高度な診断技術が備わっており、熟練した専門家が常駐しているため、正確なホルモン検査を行うのに適しています。これらの施設は、糖尿病、甲状腺機能障害、副腎障害など、詳細かつ精密な検査を必要とする疾患の総合的な診断サービスを専門としています。臨床検査施設が提供する専門知識と信頼性が、市場における優位性を引き続き牽引しています。

米国の内分泌検査市場は2024年に12億米ドルを生み出し、2034年までCAGR 7.2%で成長すると予測されています。最先端の検査ソリューションを提供する大手診断企業や検査施設の存在が、米国における市場の成長を支えています。慢性疾患への対応や予防医療の推進を目的とした政府の取り組みが、市場の拡大にさらに貢献しています。さらに、ポイントオブケア検査と個別化ヘルスケアソリューションの採用が増加していることが、全米で内分泌検査の需要を促進しています。早期診断と個別化された治療オプションへの注目が高まるにつれ、米国市場は世界の内分泌検査業界にとって重要な貢献者であり続けると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 糖尿病、甲状腺、肥満の有病率の増加

- 政府の資金援助イニシアティブ

- 技術の進歩

- 日常的な健康モニタリングに対する意識の高まり

- 業界の潜在的リスク&課題

- 検査技術の開発コストの高さ

- 認識不足

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:検査タイプ別、2021年~2034年

- 主要動向

- ヒト絨毛性ゴナドトロピン(hCG)ホルモン検査

- 甲状腺刺激ホルモン(TSH)検査

- インスリン検査

- プロゲステロン検査

- 黄体形成ホルモン(LH)検査

- プロラクチン検査

- その他の検査タイプ

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 免疫測定法

- 質量分析法

- クロマトグラフィー

- 核酸ベース

- その他の技術

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 臨床検査室

- 病院

- 診断センター

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- Agilent

- BECKMAN COULTER

- BIO RAD

- biomedical TECHNOLOGIES

- BIOMERIEUX

- DH TECH

- Diasorin

- labcorp

- QuidelOrtho

- QIAGEN

- Quest Diagnostics

- Roche

- SCIEX

- SIEMENS Healthineers

- Thermo Fisher SCIENTIFIC

The Global Endocrine Testing Market, valued at USD 3.1 billion in 2024, is poised for significant growth, with a projected CAGR of 8.2% from 2025 to 2034. This growth is driven by several factors, including the rising prevalence of endocrine disorders, increasing awareness of routine health check-ups, and government-backed initiatives aimed at improving healthcare accessibility. The growing emphasis on preventive healthcare has led to a surge in demand for endocrine tests, particularly among individuals managing chronic conditions such as diabetes and thyroid disorders.

Technological advancements in diagnostic tools and improved access to testing services are further accelerating market expansion. The integration of innovative testing methods, such as point-of-care diagnostics and personalized healthcare solutions, is also reshaping the landscape, making endocrine testing more accessible and efficient. As healthcare systems worldwide prioritize early detection and management of endocrine-related conditions, the market is expected to witness sustained growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 8.2% |

Among the various test types, the human chorionic gonadotropin (hCG) hormone test is anticipated to grow at a CAGR of 7.6%, reaching USD 2 billion by 2034. Widely used for pregnancy detection, hCG tests are favored for their accuracy and ease of use. These tests are readily available in both clinical settings and for at-home use, making them a convenient option for individuals seeking reliable pregnancy confirmation. The increasing adoption of these tests reflects the growing demand for user-friendly and precise diagnostic solutions.

The market is segmented by end-use, with clinical laboratories holding the largest share in 2024. This segment is projected to reach USD 3.4 billion by 2034. Clinical laboratories are equipped with advanced diagnostic technologies and staffed by skilled professionals, making them the preferred choice for accurate hormone testing. These facilities specialize in comprehensive diagnostic services for conditions such as diabetes, thyroid dysfunction, and adrenal disorders, which require detailed and precise testing. The expertise and reliability offered by clinical laboratories continue to drive their dominance in the market.

The U.S. endocrine testing market generated USD 1.2 billion in 2024 and is forecast to grow at a CAGR of 7.2% through 2034. The presence of leading diagnostic firms and laboratories offering state-of-the-art testing solutions supports the market's growth in the United States. Government initiatives aimed at addressing chronic illnesses and promoting preventive care further contribute to the market's expansion. Additionally, the increasing adoption of point-of-care testing and personalized healthcare solutions is driving demand for endocrine testing across the country. As the focus on early diagnosis and tailored treatment options intensifies, the U.S. market is expected to remain a key contributor to the global endocrine testing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes, thyroid, and obesity

- 3.2.1.2 Supportive government funding initiatives

- 3.2.1.3 Technological advancements

- 3.2.1.4 Growing awareness of routine health monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost for the development of testing technologies

- 3.2.2.2 Lack of awareness

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Human chorionic gonadotropin (hCG) hormone test

- 5.3 Thyroid stimulating hormone (TSH) test

- 5.4 Insulin test

- 5.5 Progesterone test

- 5.6 Luteinizing hormone (LH) test

- 5.7 Prolactin test

- 5.8 Other test types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoassay

- 6.3 Mass spectroscopy

- 6.4 Chromatography

- 6.5 Nucleic acid based

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical laboratories

- 7.3 Hospitals

- 7.4 Diagnostic centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Agilent

- 9.3 BECKMAN COULTER

- 9.4 BIO RAD

- 9.5 biomedical TECHNOLOGIES

- 9.6 BIOMERIEUX

- 9.7 DH TECH

- 9.8 Diasorin

- 9.9 labcorp

- 9.10 QuidelOrtho

- 9.11 QIAGEN

- 9.12 Quest Diagnostics

- 9.13 Roche

- 9.14 SCIEX

- 9.15 SIEMENS Healthineers

- 9.16 Thermo Fisher SCIENTIFIC