|

市場調査レポート

商品コード

1685179

アテレクトミーデバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Atherectomy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アテレクトミーデバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月10日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

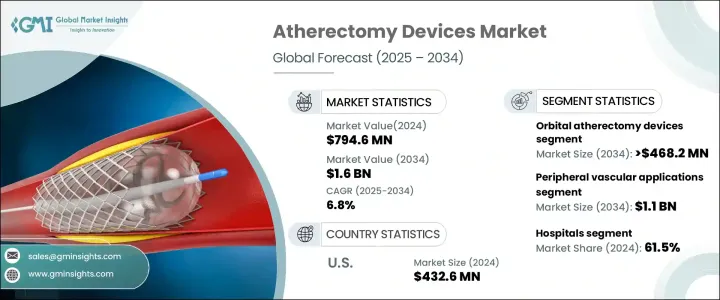

アテレクトミーデバイスの世界市場は2024年に7億9,460万米ドルに達し、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。

末梢動脈疾患(PAD)と冠動脈疾患(CAD)の有病率の上昇が、高度な治療ソリューションに対する需要を促進しています。高齢化が進み、座りっぱなしのライフスタイルが一般的になるにつれ、糖尿病や肥満の症例が急増し、低侵襲手術の必要性がさらに高まっています。ヘルスケア・プロバイダーは、合併症を最小限に抑えながらプラーク除去を強化する精密主導型のソリューションを求めており、アテレクトミーデバイスが心血管治療における不可欠なツールとなっています。

患者中心のヘルスケアへのシフトが進むにつれ、病院や医療センターは臨床転帰を改善する技術を採用するようになっています。低侵襲アテローム切除術は、従来の治療法と比較して、回復時間の短縮、入院期間の短縮、術後合併症のリスクの低減を実現します。このシフトは、医師と患者の間でより高い採用率を促しています。継続的な技術の進歩、規制当局の承認、進行中の臨床試験により、これらの機器に対する信頼が強まり、より広範な導入への道が開かれつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億9,460万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 6.8% |

市場拡大は、研究開発投資の拡大によっても推進されています。各社は、優れた効率性、精度、安全性を提供する革新的なアテレクトミー・システムを導入しています。自動化されAIと統合されたデバイスが登場し、臨床医は治療アプローチを最適化しながら手技時間を短縮できるようになっています。好意的な償還政策と外来循環器処置の増加が市場成長をさらに後押ししています。医療機関が高い成功率を実現する費用対効果の高いソリューションを優先する中、アテレクトミーデバイスは引き続き勢いを増しています。

市場セグメンテーションは、製品タイプ別に、オービタルアテレクトミー、レーザーアテレクトミー、指向性アテレクトミー、回転アテレクトミーに区分されます。オービタルアテレクトミーデバイスは大幅な成長が見込まれ、市場規模は2034年までにCAGR 6.6%で4億6,820万米ドルに達すると予測されます。これらの器具は、高速回転するクラウンまたはバリを利用して、動脈の完全性を維持しながらプラークを除去することにより、手技の精度を向上させる。末梢動脈と冠動脈の両方の治療で一貫した成功を収めていることから、複雑な症例を管理するヘルスケア専門家の間で好ましい選択肢として位置づけられています。病院や外科センターが革新的で効率的な治療オプションを優先するにつれて、軌道アテレクトミーデバイスの需要は増加の一途をたどっています。

用途別に見ると、市場は末梢血管用と冠動脈用に分けられます。末梢血管セグメントは大幅な拡大が見込まれており、CAGR 6.3%で2034年までに11億米ドルに達すると予測されています。末梢動脈疾患は可動性や生活の質に深刻な影響を与えるため、効果的な代替治療が急務となっています。アテレクトミー手術は、従来の手術に比べて回復期間の短縮、合併症の減少、入院期間の短縮など、特筆すべき利点があります。このような利点に対する認識が高まるにつれ、より多くの患者やヘルスケアプロバイダーが低侵襲治療を選択するようになり、粥腫切除装置の需要を押し上げています。

米国のアテレクトミーデバイス市場は、2024年に4億3,260万米ドルを占め、2025年から2034年にかけてCAGR 6.2%で成長すると予測されています。同国ではPADやCADを含む心血管疾患の負担が増加しており、高度な治療ソリューションに対する需要が高まっています。高齢者人口の増加は、肥満や糖尿病率の高さと相まって、市場の成長をさらに加速させています。医療機関では、手技の精度を高め、患者の安全性を向上させ、回復を早める最先端のアテレクトミーデバイスの導入が進んでいます。低侵襲心血管系処置の需要が高まるにつれ、米国市場は世界的に優位な地位を維持すると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術への嗜好の高まり

- 対象患者数の増加

- 最近の技術的進歩

- 末梢動脈疾患の有病率の上昇

- 業界の潜在的リスク&課題

- 製品の高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- 技術情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- オービタルアテレクトミーデバイス

- レーザーアテレクトミーデバイス

- 方向性アテレクトミーデバイス

- 回転アテレクトミーデバイス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 末梢血管アプリケーション

- 冠動脈アプリケーション

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- angiodynamics

- AVINGER

- B. Braun

- BD(Becton, Dickinson and Company)

- BIOMERICS

- Boston Scientific

- Cardinal Health

- Cardiovascular Systems

- Cordis

- Philips

- Medtronic

- Nipro

- Rex Medical

- TERUMO

The Global Atherectomy Devices Market reached USD 794.6 million in 2024 and is projected to grow at a CAGR of 6.8% between 2025 and 2034. The rising prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD) is fueling demand for advanced treatment solutions. As aging populations increase and sedentary lifestyles become more common, cases of diabetes and obesity are surging, further driving the need for minimally invasive procedures. Healthcare providers are seeking precision-driven solutions to enhance plaque removal while minimizing complications, making atherectomy devices an essential tool in cardiovascular treatment.

The increasing shift toward patient-centric healthcare is pushing hospitals and medical centers to adopt technologies that improve clinical outcomes. Minimally invasive atherectomy procedures offer faster recovery times, reduced hospital stays, and lower risks of post-surgical complications compared to traditional treatment methods. This shift is encouraging higher adoption rates among physicians and patients. Continuous technological advancements, regulatory approvals, and ongoing clinical trials are strengthening confidence in these devices, paving the way for their broader implementation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $ 794.6 Million |

| Forecast Value | $ 1.6 Billion |

| CAGR | 6.8% |

Market expansion is also being driven by growing investment in research and development. Companies are introducing innovative atherectomy systems that provide superior efficiency, precision, and safety. Automated and AI-integrated devices are emerging, allowing clinicians to optimize treatment approaches while reducing procedure times. Favorable reimbursement policies and an increasing number of outpatient cardiovascular procedures are further propelling market growth. As medical institutions prioritize cost-effective solutions that deliver high success rates, atherectomy devices continue to gain momentum.

By product type, the market is segmented into orbital, laser, directional, and rotational atherectomy devices. Orbital atherectomy devices are set to experience substantial growth, with market value expected to reach USD 468.2 million by 2034 at a CAGR of 6.6%. These devices improve procedural accuracy by utilizing a high-speed spinning crown or burr to remove plaque while preserving arterial integrity. Their consistent success in treating both peripheral and coronary arteries has positioned them as a preferred choice among healthcare professionals managing complex cases. As hospitals and surgical centers prioritize innovative and efficient treatment options, the demand for orbital atherectomy devices continues to rise.

Based on application, the market is divided into peripheral vascular and coronary procedures. The peripheral vascular segment is expected to expand significantly, projected to reach USD 1.1 billion by 2034 at a CAGR of 6.3%. Peripheral artery disease severely impacts mobility and quality of life, creating an urgent need for effective treatment alternatives. Atherectomy procedures offer notable advantages, including reduced recovery periods, fewer complications, and shorter hospital stays compared to traditional surgery. As awareness of these benefits grows, more patients and healthcare providers are opting for minimally invasive interventions, boosting the demand for atherectomy devices.

The U.S. atherectomy devices market accounted for USD 432.6 million in 2024 and is anticipated to grow at a CAGR of 6.2% from 2025 to 2034. The country's increasing burden of cardiovascular diseases, including PAD and CAD, is driving demand for advanced treatment solutions. A growing elderly population, coupled with high obesity and diabetes rates, is further accelerating market growth. Medical institutions are increasingly adopting cutting-edge atherectomy devices that enhance procedural precision, improve patient safety, and ensure faster recoveries. As the demand for minimally invasive cardiovascular procedures rises, the U.S. market is expected to maintain its dominant position in the global landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in preference for minimally invasive procedures

- 3.2.1.2 Growing target patient population

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Rising prevalence of peripheral arterial diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Orbital atherectomy devices

- 5.3 Laser atherectomy devices

- 5.4 Directional atherectomy devices

- 5.5 Rotational atherectomy devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular applications

- 6.3 Coronary applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 angiodynamics

- 9.3 AVINGER

- 9.4 B. Braun

- 9.5 BD (Becton, Dickinson and Company)

- 9.6 BIOMERICS

- 9.7 Boston Scientific

- 9.8 Cardinal Health

- 9.9 Cardiovascular Systems

- 9.10 Cordis

- 9.11 Philips

- 9.12 Medtronic

- 9.13 Nipro

- 9.14 Rex Medical

- 9.15 TERUMO