|

市場調査レポート

商品コード

1685178

経腸栄養デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Enteral Feeding Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 経腸栄養デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

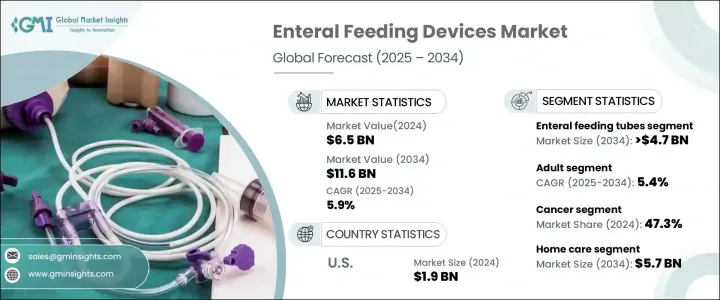

経腸栄養デバイスの世界市場は、2024年には65億米ドルと評価され、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

この分野の成長の原動力は、慢性疾患の有病率の増加、新生児・早産児への給餌需要の増加、在宅介護環境における経腸栄養ソリューションの採用拡大です。食物を自然に摂取する能力が損なわれる状態に直面する人が増えるにつれて、これらの機器に対する需要は上昇を続けています。経腸栄養は、病状により経口摂取ができない人に必要な栄養素を届けるという重要な役割を担っています。咀嚼能力や嚥下能力に影響を及ぼす治療を受けている患者は、十分な栄養を維持するためにこれらの器具に依存しています。在宅ケアは、その費用対効果と利便性から大きな伸びを示しています。ヘルスケアプロバイダーは、短期的および長期的な栄養ニーズの管理に経腸栄養ソリューションを推奨するようになっています。

経腸栄養デバイス市場は、経腸栄養チューブ、ポンプ、シリンジ、投与セット、付属品などの製品タイプに基づいて分類されます。経腸栄養チューブはCAGR 5.6%で市場拡大をリードし、2034年には47億米ドル以上に達すると予測されています。これらの経腸栄養チューブは、様々な健康状態にある人々に標的を絞った栄養を供給するために不可欠です。急性期医療や慢性期医療におけるその役割は、適切な栄養補給を確保するための好ましいソリューションとなっています。さまざまなタイプの栄養チューブが利用可能なため、ヘルスケア専門家は個々の患者のニーズに基づいて治療をカスタマイズすることができます。病院、診療所、在宅介護施設での幅広い採用により、経腸栄養チューブは引き続き市場成長の主要な原動力となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 116億米ドル |

| CAGR | 5.9% |

同市場はまた、成人や小児などの患者グループに基づいてセグメント化されています。成人のカテゴリーが最大のシェアを占めており、2025年から2034年にかけてCAGR 5.4%で成長すると予測されます。経腸栄養を必要とする成人の数が増加していることが、これらの機器の持続的な需要に寄与しています。長期疾患を持つ成人の多くは、健康維持と合併症予防のために長期間の経腸栄養を必要としています。従来の栄養補給が不可能な場合に重要な栄養補給を提供するため、緩和ケアにおけるこれらのソリューションの採用が増加しており、需要をさらに押し上げています。

用途別では、経腸栄養デバイスは、がん、神経疾患、消化器疾患など、さまざまな病状で広く使用されています。がん分野は2024年の市場シェアの47.3%を占めています。多くの治療により食事の摂取が困難になるため、十分な栄養を維持するために経腸栄養が必要となります。長期療養を必要とする患者にとって、これらの機器はさらなる合併症を予防しながらエネルギーレベルを安定させるために不可欠な役割を果たしています。

市場はまた、在宅介護、病院、その他の施設など、最終用途によっても分けられています。在宅介護分野は2024年に市場をリードし、2034年には57億米ドルに達すると予測されています。高齢化により在宅経腸栄養の需要が高まり、自立性を維持しながら必要な栄養補給ができるようになりました。長期入院と比較して、在宅ケアは手ごろな価格であるため、多くの患者にとって好ましい選択肢となっています。利用しやすくなったことで、特に医療費の自己負担が大きい地域では、より多くの患者がこうしたソリューションの恩恵を受けることができます。

米国の経腸栄養機器市場は、2024年に19億米ドルと評価され、2034年までCAGR 5.2%で成長すると予測されています。高齢者人口の増加と在宅ヘルスケアサービスの普及が市場拡大を支えています。主要企業による研究開発は、技術革新と製品供給に貢献しています。好意的な償還政策と栄養療法を推進する政府のイニシアティブが市場成長をさらに強化します。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の上昇

- 新生児および早産の経腸栄養需要の増加

- 在宅医療現場での経腸栄養への嗜好の高まり

- 経腸栄養デバイスの技術的進歩

- 業界の潜在的リスク&課題

- 経腸栄養チューブに伴う合併症

- 厳しい政府規制とコンプライアンス要件

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 経腸栄養チューブ

- 経腸/経鼻栄養チューブ

- 経鼻胃チューブ

- 経鼻空腸チューブ

- 腹腔/オステオトミー栄養チューブ

- 胃瘻チューブ

- 空腸瘻/空腸チューブ

- 胃空腸(GJ)または経空腸チューブ

- 経腸/経鼻栄養チューブ

- 経腸栄養ポンプ

- 経腸用シリンジ

- ギビングセット

- アクセサリ

第6章 市場推計・予測:患者別、2021年~2034年

- 主要動向

- 成人

- 小児

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- がん

- 頭頸部がん

- 消化器がん

- その他のがん

- 中枢神経系(CNS)とメンタルヘルス

- 非悪性胃腸(GI)障害

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 在宅医療

- 病院

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ALCOR SCIENTIFIC

- Abbott

- AMSINO

- AMT

- -Braun

- Baxter

- Becton Dickinson

- Boston Scientific

- Cardinal Health

- CONMED

- Cook Medical

- DANONE

- FRESENIUS KABI

- HALYARD

- MOOG

- VYGON

The Global Enteral Feeding Devices Market was valued at USD 6.5 billion in 2024 and is projected to grow at a CAGR of 5.9% from 2025 to 2034. Growth in this sector is driven by the increasing prevalence of chronic illnesses, rising demand for neonatal and preterm feeding, and the expanding adoption of enteral feeding solutions in home care settings. As more individuals face conditions that impair their ability to consume food naturally, the demand for these devices continues to climb. Enteral feeding plays a crucial role in delivering essential nutrients to individuals who cannot eat orally due to medical conditions. Patients undergoing treatments that impact their ability to chew or swallow rely on these devices to maintain adequate nutrition. Home-based care is seeing significant growth due to its cost-effectiveness and convenience. Healthcare providers increasingly recommend enteral feeding solutions for managing both short-term and long-term nutritional needs.

The enteral feeding devices market is categorized based on product type, including enteral feeding tubes, pumps, syringes, giving sets, and accessories. Enteral feeding tubes are expected to lead market expansion with a projected CAGR of 5.6%, reaching over USD 4.7 billion by 2034. These tubes are essential for delivering targeted nutrition to individuals dealing with various health conditions. Their role in acute and chronic care settings makes them a preferred solution for ensuring proper nourishment. The availability of different types of feeding tubes enables healthcare professionals to customize treatments based on individual patient needs. With broad adoption across hospitals, clinics, and home care facilities, enteral feeding tubes remain a primary driver of market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 5.9% |

The market is also segmented based on patient groups, including adult and pediatric populations. The adult category holds the largest share and is expected to grow at a CAGR of 5.4% from 2025 to 2034. A rising number of adults requiring enteral nutrition contributes to sustained demand for these devices. Many adults with long-term conditions need enteral feeding for extended periods to maintain health and prevent complications. The increasing adoption of these solutions in palliative care further boosts demand, as they provide vital nutritional support in cases where traditional feeding is not an option.

In terms of application, enteral feeding devices are widely used across various medical conditions, including cancer, neurological disorders, and gastrointestinal diseases. The cancer segment accounted for 47.3% of the market share in 2024. Many treatments lead to difficulties in consuming food, making enteral feeding necessary to maintain adequate nutrition. For individuals requiring long-term care, these devices play an essential role in ensuring energy levels remain stable while preventing further complications.

The market is also divided by end-use, including home care, hospitals, and other facilities. The home care sector led the market in 2024 and is expected to reach USD 5.7 billion by 2034. An aging population drives demand for home-based enteral feeding, allowing individuals to receive necessary nutritional support while maintaining independence. The affordability of home-based care, compared to extended hospital stays, makes it a preferred choice for many patients. With increased accessibility, more individuals can benefit from these solutions, particularly in regions with high out-of-pocket healthcare expenses.

The U.S. enteral feeding devices market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 5.2% through 2034. A growing elderly population and increasing adoption of home healthcare services support market expansion. Research and development efforts by leading companies contribute to innovation and product availability. Favorable reimbursement policies and government-backed initiatives promoting nutritional therapies further strengthen market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Increase in demand for neonatal and preterm enteral feeding

- 3.2.1.3 Surging preference for enteral feeding at home care settings

- 3.2.1.4 Technological advancements in enteral feeding devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications associated with enteral feeding tubes

- 3.2.2.2 Stringent government regulations and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Enteral feeding tubes

- 5.2.1 Nasoenteric/nasal feeding tube

- 5.2.1.1 Nasogastric tube

- 5.2.1.2 Nasojejunal tube

- 5.2.2 Abdominal/ostotomy feeding tube

- 5.2.2.1 Gastrostomy tube

- 5.2.2.2 Jejunostomy/jejunal tube

- 5.2.2.3 Gastrojejunal (GJ) or transjejunal tube

- 5.2.1 Nasoenteric/nasal feeding tube

- 5.3 Enteral feeding pumps

- 5.4 Enteral syringes

- 5.5 Giving sets

- 5.6 Accessories

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer

- 7.2.1 Head and neck cancer

- 7.2.2 Gastrointestinal cancer

- 7.2.3 Other cancer types

- 7.3 Central nervous system (CNS) and mental health

- 7.4 Non-malignant gastrointestinal (GI) disorders

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Hospitals

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALCOR SCIENTIFIC

- 10.2 Abbott

- 10.3 AMSINO

- 10.4 AMT

- 10.5 - Braun

- 10.6 Baxter

- 10.7 Becton Dickinson

- 10.8 Boston Scientific

- 10.9 Cardinal Health

- 10.10 CONMED

- 10.11 Cook Medical

- 10.12 DANONE

- 10.13 FRESENIUS KABI

- 10.14 HALYARD

- 10.15 MOOG

- 10.16 VYGON