IDS/IPSの市場機会、成長促進要因、業界動向分析、2025年~2034年予測

Intrusion Detection System / Intrusion Prevention System (IDS / IPS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685148

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

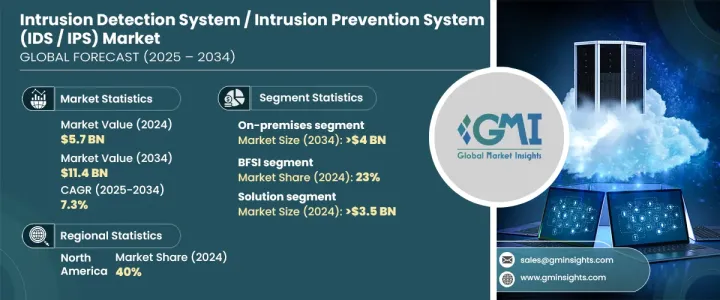

IDS/IPSの世界市場は、2024年に57億米ドルと評価され、2025~2034年にかけてCAGR 7.3%で成長すると予測されています。

サイバー脅威の高度化により、ネットワーク、アプリケーション、機密データを保護する先進的IDS/IPSソリューションの需要が高まっています。各産業の企業は、セキュリティを強化し、不正アクセスを防止し、潜在的な侵害をリアルタイムで検出するために、これらのシステムを優先しています。市場の成長は、デジタル技術の急速な導入、データ侵害に対する懸念の高まり、厳格なデータ保護規制を遵守する必要性によってさらに加速しています。

企業は機密データの価値が高まっていることを認識しており、IDS/IPSソリューションへの投資はサイバーセキュリティ戦略の重要な要素となっています。さらに、クラウドコンピューティング、IoTデバイス、リモートワーク環境への依存度が高まっているため、強固なセキュリティ対策の必要性が高まっており、市場の拡大をさらに後押ししています。また、IDS/IPSシステムに人工知能や機械学習を統合することで、その機能が強化され、リアルタイムでの脅威検知や進化するサイバーリスクへの事前対応が可能となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 57億米ドル |

| 予測金額 | 114億米ドル |

| CAGR | 7.3% |

市場は展開モデル別にオンプレミス、クラウド、ハイブリッドソリューションに区分されます。2024年には、オンプレミス型が市場シェアの40%以上を占め、2034年には40億米ドルを超えると予測されています。政府機関、金融、医療など、機密性の高いデータを扱う産業では、管理とセキュリティが強化されているオンプレミス型システムが好まれます。これらの産業では、サードパーティリスクを軽減し、HIPAA、PCI DSS、GDPRなどの規制へのコンプライアンスを確保することを優先しています。さらに、航空宇宙やエネルギーなどの産業では、特定のセキュリティニーズに合わせて検出ルールをカスタマイズできるため、オンプレミスのIDS/IPSソリューションが有益です。クラウドとハイブリッドの導入モデルも、その拡大性、費用対効果、遠隔操作をサポートする能力によって、支持を集めています。

用途別に見ると、IDS/IPS市場は、BFSI(銀行、金融サービス、保険)、医療、IT・通信、政府、製造、運輸・物流、小売など、さまざまなセクターにサービスを提供しています。BFSIセグメントは2024年に市場シェアの約23%を占め、デジタル取引の普及とサイバー犯罪リスクの高まりがその要因となっています。デジタルバンキングが成長を続ける中、金融機関は機密性の高い顧客データを保護し、信頼を維持するためにIDS/IPSソリューションに多額の投資を行っています。同様に、医療セグメントでは、患者データを保護し、規制を遵守するためにこれらのシステムを導入しており、IT・通信産業では、膨大なネットワークを保護し、サービスの中断を防ぐためにIDS/IPSを活用しています。

2024年のIDS/IPS市場は北米が40%のシェアを占め、米国が最大の貢献国となっています。この地域では、重要インフラ、政府機関、金融機関を標的としたサイバー攻撃の頻度が高まっており、先進的セキュリティシステムへの需要が高まっています。サイバー犯罪者はネットワークへの侵入や電子メールの漏洩など、より巧妙な手口を用いるようになっており、信頼性の高いIDS/IPSソリューションの必要性が高まっています。北米の企業や政府が引き続きサイバーセキュリティを優先する中、IDS/IPSシステムの採用は引き続き堅調に推移し、進化する脅威に対する強固な保護が確保されると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- IDS/IPSソリューションプロバイダー

- IDS/IPSサービスプロバイダー

- システムインテグレーター

- 付加価値再販業者(VAR)と販売業者

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- サイバーセキュリティの脅威(地域別)

- 使用事例

- 影響要因

- 促進要因

- サイバー攻撃の頻度と巧妙さの増加

- クラウドサービスとハイブリッドインフラの急速な普及

- IoTデバイスの統合の増加

- 規制コンプライアンス要件の高まり

- 産業の潜在的リスク・課題

- 高い導入コストと運用コスト

- 誤検知の管理とシステムの精度維持の複雑化

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:コンポーネント別、2021~2034年

- 主要動向

- ソリューション

- IDS/IPSソフトウェア

- 物理/仮想アプライアンス

- 統合セキュリティプラットフォーム

- サービス

- マネージドサービス

- プロフェッショナルサービス

第6章 市場推定・予測:ソリューションアーキテクチャ別、2021~2034年

- 主要動向

- ホスト型IDS/IPS

- ワイヤレスベースIDS/IPS

- ネットワークベースIDS/IPS

第7章 市場推定・予測:検知アーキテクチャ別、2021~2034年

- 主要動向

- シグネチャ型

- アノマリーベース

- 施策ベース

第8章 市場推定・予測:導入モデル別、2021~2034年

- 主要動向

- オンプレミス

- クラウド

- ハイブリッド

第9章 市場推定・予測:組織規模別、2021~2034年

- 主要動向

- 大企業

- 中小企業

第10章 市場推定・予測:用途別、2021~2034年

- 主要動向

- BFSI

- 航空宇宙・防衛

- 医療

- IT・通信

- 政府機関

- 製造業

- 運輸・物流

- 小売

- その他

第11章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Alert Logic

- AT&T

- Barracuda Networks

- Check Point Software Technologies

- Cisco

- CrowdStrike

- Darktrace

- F5 Networks

- FireEye

- Fortinet

- IBM

- Imperva

- Juniper Networks

- McAfee

- Palo Alto Networks

- SonicWall

- Sophos

- Splunk

- Trend Micro

- Trustwave

目次

The Global Intrusion Detection System / Intrusion Prevention System Market was valued at USD 5.7 billion in 2024 and is projected to grow at a CAGR of 7.3% from 2025 to 2034. The increasing sophistication of cyber threats has driven the demand for advanced IDS/IPS solutions to protect networks, applications, and sensitive data. Businesses across industries are prioritizing these systems to enhance security, prevent unauthorized access, and detect potential breaches in real-time. The market's growth is further fueled by the rapid adoption of digital technologies, rising concerns over data breaches, and the need to comply with stringent data protection regulations.

As organizations recognize the growing value of sensitive data, investments in IDS/IPS solutions have become a critical component of their cybersecurity strategies. Additionally, the increasing reliance on cloud computing, IoT devices, and remote work environments has heightened the need for robust security measures, further propelling the market's expansion. The integration of artificial intelligence and machine learning into IDS/IPS systems is also enhancing their capabilities, enabling real-time threat detection and proactive responses to evolving cyber risks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.7 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 7.3% |

The market is segmented by deployment models into on-premises, cloud, and hybrid solutions. In 2024, the on-premises segment accounted for over 40% of the market share and is expected to surpass USD 4 billion by 2034. Industries handling highly sensitive data, such as government, finance, and healthcare, prefer on-premises systems due to their enhanced control and security. These sectors prioritize mitigating third-party risks and ensuring compliance with regulations like HIPAA, PCI DSS, and GDPR. Additionally, industries such as aerospace and energy benefit from on-premises IDS/IPS solutions, as they allow for customized detection rules tailored to specific security needs. The cloud and hybrid deployment models are also gaining traction, driven by their scalability, cost-effectiveness, and ability to support remote operations.

By application, the IDS/IPS market serves various sectors, including BFSI (banking, financial services, and insurance), healthcare, IT and telecom, government, manufacturing, transportation and logistics, and retail. The BFSI segment held approximately 23% of the market share in 2024, driven by the increasing prevalence of digital transactions and the rising risk of cybercrime. As digital banking continues to grow, financial institutions are investing heavily in IDS/IPS solutions to safeguard sensitive customer data and maintain trust. Similarly, the healthcare sector is adopting these systems to protect patient data and comply with regulations, while the IT and telecom industry leverages IDS/IPS to secure vast networks and prevent service disruptions.

North America dominated the IDS/IPS market in 2024, holding a 40% share, with the United States being the largest contributor. The region's demand for advanced security systems is driven by the increasing frequency of cyberattacks targeting critical infrastructure, government organizations, and financial institutions. Cybercriminals are employing more sophisticated tactics, such as network intrusions and email compromises, which has intensified the need for reliable IDS/IPS solutions. As businesses and governments in North America continue to prioritize cybersecurity, the adoption of IDS/IPS systems is expected to remain strong, ensuring robust protection against evolving threats.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 IDS/IPS solution providers

- 3.1.2 IDS/IPS service providers

- 3.1.3 System integrators

- 3.1.4 Value-Added Resellers (VARs) and distributors

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cybersecurity threats, by region

- 3.9 Case studies

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing frequency and sophistication of cyberattacks

- 3.10.1.2 Rapid adoption of cloud services and hybrid infrastructures

- 3.10.1.3 Rising integration of IoT devices

- 3.10.1.4 Growing regulatory compliance requirements

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation and operational costs

- 3.10.2.2 Increasing complexity in managing false positives and maintaining system accuracy

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 IDS/IPS software

- 5.2.2 Physical/virtual appliances

- 5.2.3 Integrated security platforms

- 5.3 Services

- 5.3.1 Managed services

- 5.3.2 Professional services

Chapter 6 Market Estimates & Forecast, By Solution Architecture, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Host-based IDS/IPS

- 6.3 Wireless-based IDS/IPS

- 6.4 Network-based IDS/IPS

Chapter 7 Market Estimates & Forecast, By Detection Method, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Signature-based

- 7.3 Anomaly-based

- 7.4 Policy-based

Chapter 8 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Cloud

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Large enterprises

- 9.3 SME

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 Aerospace & defense

- 10.4 Healthcare

- 10.5 IT & telecom

- 10.6 Government

- 10.7 Manufacturing

- 10.8 Transportation & logistics

- 10.9 Retail

- 10.10 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Alert Logic

- 12.2 AT&T

- 12.3 Barracuda Networks

- 12.4 Check Point Software Technologies

- 12.5 Cisco

- 12.6 CrowdStrike

- 12.7 Darktrace

- 12.8 F5 Networks

- 12.9 FireEye

- 12.10 Fortinet

- 12.11 IBM

- 12.12 Imperva

- 12.13 Juniper Networks

- 12.14 McAfee

- 12.15 Palo Alto Networks

- 12.16 SonicWall

- 12.17 Sophos

- 12.18 Splunk

- 12.19 Trend Micro

- 12.20 Trustwave

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日