|

市場調査レポート

商品コード

1685144

磁気共鳴イメージングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Magnetic Resonance Imaging (MRI) Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 磁気共鳴イメージングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月08日

発行: Global Market Insights Inc.

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

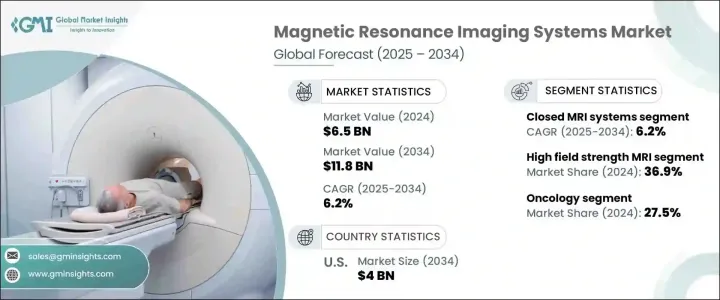

磁気共鳴イメージングシステムの世界市場は、2024年に65億米ドルに達し、2025年から2034年にかけてCAGR 6.2%で成長すると予測されています。

MRI技術は、強力な磁場と電波を利用して体内構造の詳細な画像を生成する非侵襲的イメージング手法であり、現代の診断において重要な役割を果たしています。他の画像診断技術とは異なり、MRIは切開や電離放射線への曝露を必要としないため、軟部組織の精密な可視化に適しています。神経疾患、心血管疾患、筋骨格系疾患などの慢性疾患の増加により、高度な診断ソリューションに対する需要が高まっています。

MRIシステムの技術的進歩は、画像解像度の向上、スキャン時間の短縮、患者の快適性の向上に重点を置き、市場拡大の原動力となっています。MRI画像診断への人工知能(AI)の統合は、画像判読の自動化とばらつきの低減によって診断精度をさらに向上させています。さらに、ポータブルMRIシステムやオープンMRIシステムへのシフトにより、移動に課題がある患者や閉所恐怖症の患者でも画像診断が利用しやすくなっています。ヘルスケア投資の増加と疾病の早期発見の重視が相まって、市場の成長を促進すると予想されます。政府や民間ヘルスケアプロバイダーは、精密画像診断に対する需要の高まりに対応するため、最先端の診断機器に投資しています。特に新興国では、ヘルスケアのインフラ整備が進むにつれて、高性能MRIシステムの採用が加速していくと思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 118億米ドル |

| CAGR | 6.2% |

市場はアーキテクチャによってオープンMRIシステムとクローズドMRIシステムに区分されます。クローズドMRIシステム分野は、予測期間を通じてCAGR 6.2%で成長すると予測されます。これらのシステムは、完全に密閉された円筒形の設計が特徴で、外部干渉やモーションアーチファクトを最小限に抑えることで優れた画質を実現します。クローズドMRI装置は、異常の検出に正確な撮像が重要な神経学や腫瘍学の高解像度診断に広く使用されています。最近の技術革新により、より広々とした設計とスキャン時間の短縮が実現し、閉所恐怖症や撮像処置中の不快感に対する患者の懸念が軽減されています。

MRIシステムは磁場強度に基づいて、低磁場強度、中磁場強度、高磁場強度に分類されます。高磁場強度セグメントは2024年に36.9%のシェアで市場を独占し、今後も主導的地位を維持すると予想されます。通常、1.5テスラ以上で動作する高磁場MRIシステムは、極めて鮮明な画像を提供し、正確な診断を保証します。これらのシステムは、画像の忠実度を高め、歪みを減らし、スキャンを迅速化する進歩の恩恵を受けており、患者の全体的な体感を大幅に改善しています。病院や画像診断センターが精密診断を優先するにつれ、高磁場MRI技術に対する需要は増加の一途をたどっています。

米国MRIシステム市場は、最先端診断技術への強い注目により、2034年までに40億米ドルを創出すると予測されています。全米の病院や画像診断センターは、診断精度と効率性を高めるため、次世代MRI装置に多額の投資を行っています。米国のヘルスケア部門は、AIと機械学習を統合し、ワークフローを最適化してスキャン時間を短縮する、より高度な画像診断システムへとシフトしています。患者の予後改善に対する要求が高まる中、MRI技術の拡大は、医療診断の進化する状況において重要な役割を果たすと予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 先進国および新興経済諸国における高齢者人口の増加

- 世界の慢性疾患有病率の増加

- 北米および欧州における早期診断に対する意識の高まり

- 新興経済諸国におけるMRIシステムの技術進歩

- アジア太平洋およびその他の新興経済圏における事故件数の増加

- 業界の潜在的リスク&課題

- 熟練した専門家の不足

- MRIシステムの高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- 2024年の価格分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:アーキテクチャ別、2021年~2034年

- 主要動向

- オープンシステム

- クローズドシステム

第6章 市場推計・予測:電界強度別、2021年~2034年

- 主要動向

- 低電界強度

- 中電界強度

- 高電界強度

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 腫瘍学

- 神経

- 筋骨格系

- 血管

- 消化器内科

- 心臓病学

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 画像センター

- 外来手術センター

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- ポーランド

- スイス

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- タイ

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- チリ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- イスラエル

第10章 企業プロファイル

- Aurora Imaging Technologies

- Esaote

- Fonar

- FUJIFILM

- GE HealthCare Technologies

- Koninklijke Philips

- Neusoft Medical Systems

- Sanrad Medical Systems

- Siemens Healthineers

- Toshiba

The Global Magnetic Resonance Imaging Systems Market reached USD 6.5 billion in 2024 and is set to grow at a CAGR of 6.2% between 2025 and 2034. MRI technology, a non-invasive imaging method that utilizes strong magnetic fields and radio waves to generate detailed images of the body's internal structures, plays a crucial role in modern diagnostics. Unlike other imaging techniques, MRI does not require incisions or exposure to ionizing radiation, making it a preferred choice for precise visualization of soft tissues. The rising prevalence of chronic diseases, including neurological disorders, cardiovascular conditions, and musculoskeletal issues, has intensified the demand for advanced diagnostic solutions.

Technological advancements in MRI systems are driving market expansion, with a focus on improved image resolution, shorter scan times, and enhanced patient comfort. The integration of artificial intelligence (AI) into MRI imaging has further refined diagnostic accuracy by automating image interpretation and reducing variability. Additionally, the shift toward portable and open MRI systems has made imaging more accessible for patients with mobility challenges or claustrophobia. Increasing healthcare investments, coupled with a growing emphasis on early disease detection, are expected to propel market growth. Governments and private healthcare providers are investing in cutting-edge diagnostic equipment to meet the rising demand for precision imaging. As healthcare infrastructure advances, particularly in emerging economies, the adoption of high-performance MRI systems will continue to accelerate.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 6.2% |

The market is segmented based on architecture into open and closed MRI systems. The closed MRI system segment is anticipated to grow at a 6.2% CAGR throughout the forecast period. These systems, characterized by fully enclosed cylindrical designs, deliver superior image quality by minimizing external interference and motion artifacts. Closed MRI machines are widely used for high-resolution diagnostics in neurology and oncology, where precise imaging is critical for detecting abnormalities. Recent innovations have led to more spacious designs and shorter scan durations, alleviating patient concerns about claustrophobia and discomfort during imaging procedures.

Based on field strength, MRI systems are categorized into low, mid, and high field strength. The high field strength segment dominated the market in 2024 with a 36.9% share and is expected to maintain its leading position. Typically operating above 1.5 Tesla, high-field MRI systems provide exceptional image clarity, ensuring accurate diagnostics. These systems benefit from advancements that enhance image fidelity, reduce distortions, and expedite scanning, significantly improving the overall patient experience. As hospitals and imaging centers prioritize precision diagnostics, the demand for high-field MRI technology continues to rise.

U.S. MRI systems market is projected to generate USD 4 billion by 2034, driven by a strong focus on cutting-edge diagnostic technologies. Hospitals and imaging centers across the country are making significant investments in next-generation MRI equipment to enhance diagnostic accuracy and efficiency. The U.S. healthcare sector is shifting toward more advanced imaging systems that integrate AI and machine learning, optimizing workflow and reducing scan times. As the demand for improved patient outcomes grows, the expansion of MRI technology is expected to play a key role in the evolving landscape of medical diagnostics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population in developed as well as developing economies

- 3.2.1.2 Increasing chronic disease prevalence globally

- 3.2.1.3 Growing awareness pertaining to early diagnosis in North America and Europe

- 3.2.1.4 Technological advancements in MRI system in developed economies

- 3.2.1.5 Increasing number of accidents in Asia Pacific and other emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled professionals

- 3.2.2.2 High cost of MRI system

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Pricing analysis, 2024

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Architecture, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Open system

- 5.3 Closed system

Chapter 6 Market Estimates and Forecast, By Field Strength, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Low field strength

- 6.3 Mid field strength

- 6.4 High field strength

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oncology

- 7.3 Neurology

- 7.4 Musculoskeletal

- 7.5 Vascular

- 7.6 Gastroenterology

- 7.7 Cardiology

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Imaging centers

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Poland

- 9.3.8 Switzerland

- 9.3.9 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.5.5 Chile

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Israel

Chapter 10 Company Profiles

- 10.1 Aurora Imaging Technologies

- 10.2 Esaote

- 10.3 Fonar

- 10.4 FUJIFILM

- 10.5 GE HealthCare Technologies

- 10.6 Koninklijke Philips

- 10.7 Neusoft Medical Systems

- 10.8 Sanrad Medical Systems

- 10.9 Siemens Healthineers

- 10.10 Toshiba