|

市場調査レポート

商品コード

1685116

肺機能検査システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Pulmonary Function Testing Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 肺機能検査システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

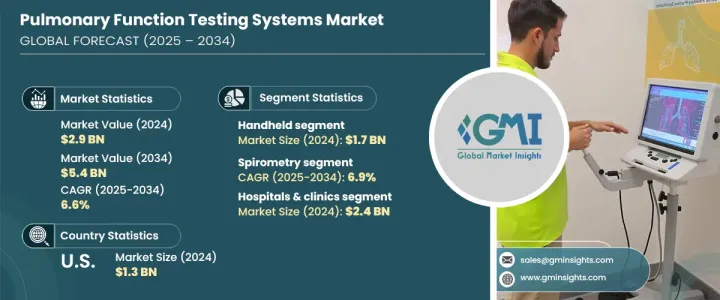

肺機能検査システムの世界市場は2024年に29億米ドルに達し、2025年から2034年にかけてCAGR 6.6%で拡大する見通しです。

この急成長の背景には、診断技術の絶え間ない進歩、人口の高齢化、疾患の早期発見に対する意識の高まり、ヘルスケアインフラの改善があります。呼吸器疾患が蔓延する中、ヘルスケアプロバイダーは早期診断と効率的な疾患管理を優先しており、これが高度肺機能検査システムの需要を大幅に押し上げています。小型で高精度な機器の革新により、さまざまなヘルスケア環境において肺機能評価がより身近なものとなっています。費用対効果が高く、使いやすい診断ツールへのシフトが業界を形成し、臨床や在宅環境での採用を促進しています。

市場の成長は、医療技術とデジタル統合への継続的な投資により、肺評価の効率と信頼性が向上していることがさらに後押ししています。継続的な呼吸モニタリングのニーズの高まりは、機能性と精度を向上させた機器の開発をメーカーに促しています。ウェアラブルおよび遠隔モニタリングソリューションの台頭は呼吸器診断に変革をもたらし、患者とヘルスケア専門家の双方にとってより便利なものとなっています。個別化医療に向けた業界の動きに伴い、肺機能検査システムはより正確で患者に特化した知見を提供するよう進化しています。予防医療への取り組みと広範なスクリーニング・プログラムが普及を加速させており、今後数年間の着実な拡大を確実なものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 29億米ドル |

| 予測金額 | 54億米ドル |

| CAGR | 6.6% |

ポータブルでコンパクトな診断機器は、その使いやすさと、さまざまなヘルスケア環境において正確な結果を提供する能力により、大きな需要が生じています。ハンドヘルド・セグメンテーションが市場をリードし、2024年には17億米ドルの売上を計上しました。このようなコスト効率の高い機器は、特に、手頃な価格でありながら正確な呼吸評価を必要とする小規模ヘルスケア施設では、ラボベースの大型機器よりも好まれています。リアルタイムの検査に柔軟に対応できることから、複数の医療用途で採用が進んでいます。メーカーが機器の性能を改良し、ユーザーの利便性を高めるにつれて、業界はデジタル接続と遠隔モニタリング機能へとシフトしています。正確で利用しやすい肺機能検査ソリューションに対する需要の高まりが技術革新を促進し、現代のヘルスケアシステムにおける肺機能検査ソリューションの重要な役割を強化しています。

慢性呼吸器疾患は市場拡大の主要因であり、慢性疾患が需要のかなりの部分を占めています。慢性閉塞性肺疾患(COPD)セグメントは、2024年に39.8%の市場シェアを占めました。環境汚染物質やライフスタイル要因による肺疾患の罹患率の上昇により、肺機能検査は日常のヘルスケアに欠かせないものとなっています。慢性呼吸器疾患が蔓延するにつれ、ヘルスケアプロバイダーは早期介入を促進するために高度な診断機器に投資しています。疾患の進行を遅らせるためには早期発見が重要であることから、精密な肺機能評価に対する需要が高まっています。検査技術の進歩は効率を向上させ、より優れたモニタリングと疾病管理ソリューションを提供しています。ヘルスケアインフラの拡大も最先端の肺機能検査機器へのアクセスを改善し、市場全体の成長を促進しています。

米国の肺機能検査システム市場は、2024年に13億米ドルと評価され、2034年までCAGR 5.4%で成長すると予測されています。医療技術の世界的リーダーである米国は、高精度の診断ツールをヘルスケア機関に統合し続け、肺機能評価の精度と効率を向上させています。デジタル機器やワイヤレス対応機器の普及により肺機能検査がさらに合理化され、市場全体の需要が高まっています。ヘルスケアの技術革新への投資が活発化し、疾病の早期発見への関心が高まっていることから、米国市場は今後10年間にわたって安定した成長を遂げることができます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性呼吸器疾患の増加

- 技術の進歩

- 政府の積極的な取り組み

- 業界の潜在的リスク&課題

- 肺機能検査機器に関連する高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 償還シナリオ

- 価格分析

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ハンドヘルド

- テーブルトップ

第6章 市場推計・予測:検査タイプ別、2021年~2034年

- 主要動向

- スパイロメトリー

- 運動負荷試験

- 肺活量検査

- 高地シミュレーション検査

- ガス拡散試験

- その他の検査

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 慢性閉塞性肺疾患

- 喘息

- 慢性息切れ

- 肺線維症

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院・診療所

- 診断センター

- 在宅ケア環境

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Baxter

- CHEST M.I

- COSMED

- ECO MEDICS

- FUKUDA SANGYO

- GANSHORN SCHILLER GROUP

- Geratherm Respiratory

- medical equipment europe

- MGC DIAGNOSTICS

- MINATO MEDICAL SCIENCE

- MORGAN

- ndd Medical Technologies

- PHILIPS

- Vitalograph

- Vyaire MEDICAL

The Global Pulmonary Function Testing Systems Market reached USD 2.9 billion in 2024 and is on track to expand at a CAGR of 6.6% between 2025 and 2034. This rapid growth is fueled by continuous advancements in diagnostic technologies, an aging population, increased awareness of early disease detection, and improved healthcare infrastructure. With respiratory diseases becoming more prevalent, healthcare providers are prioritizing early diagnosis and efficient disease management, which is significantly boosting the demand for advanced pulmonary function testing systems. Innovations in compact, high-precision devices are making pulmonary assessments more accessible across various healthcare settings. The shift toward cost-effective and user-friendly diagnostic tools is shaping the industry, driving greater adoption in clinical and home-based environments.

Market growth is further supported by ongoing investments in medical technology and digital integration, enhancing the efficiency and reliability of pulmonary assessments. The increasing need for continuous respiratory monitoring is pushing manufacturers to develop devices with improved functionality and accuracy. The rise of wearable and remote monitoring solutions is transforming respiratory diagnostics, making them more convenient for both patients and healthcare professionals. As the industry moves toward personalized medicine, pulmonary function testing systems are evolving to provide more precise and patient-specific insights. Preventive care initiatives and widespread screening programs are accelerating adoption, ensuring steady expansion in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 6.6% |

Portable and compact diagnostic devices are experiencing significant demand due to their ease of use and ability to provide precise results in various healthcare environments. The handheld segment led the market, generating USD 1.7 billion in revenue in 2024. These cost-efficient devices are favored over larger, laboratory-based equipment, particularly by smaller healthcare facilities that require affordable yet accurate respiratory assessments. Their flexibility in delivering real-time testing has led to increased adoption across multiple medical applications. As manufacturers refine device performance and enhance user convenience, the industry is shifting toward digital connectivity and remote monitoring capabilities. The rising demand for accurate and accessible pulmonary function testing solutions is driving innovation, reinforcing their essential role in modern healthcare systems.

Chronic respiratory conditions are a major factor driving market expansion, with chronic diseases accounting for a substantial portion of demand. The chronic obstructive pulmonary disease (COPD) segment held a 39.8% market share in 2024. The rising incidence of pulmonary disorders due to environmental pollutants and lifestyle factors has made pulmonary function testing a crucial part of routine healthcare. As chronic respiratory diseases become more prevalent, healthcare providers are investing in advanced diagnostic equipment to facilitate early intervention. The importance of early detection in slowing disease progression is increasing demand for precise pulmonary assessments. Advancements in testing technology are improving efficiency, thus offering better monitoring and disease management solutions. Expanding healthcare infrastructure is also improving access to state-of-the-art pulmonary function testing devices, driving overall market growth.

The US pulmonary function testing systems market was valued at USD 1.3 billion in 2024 and is projected to grow at a CAGR of 5.4% through 2034. As a global leader in medical technology, the US continues to integrate high-precision diagnostic tools into healthcare institutions, improving accuracy and efficiency in pulmonary assessments. The widespread adoption of digital and wireless-enabled devices is further streamlining pulmonary function testing, increasing overall market demand. With strong investments in healthcare innovation and a rising focus on early disease detection, the US market is well-positioned for consistent growth over the next decade.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in prevalence of chronic respiratory diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Favourable government initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with pulmonary function testing devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 — 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld

- 5.3 Tabletop

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 — 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Spirometry

- 6.3 Exercise stress test

- 6.4 Lung volume test

- 6.5 High altitude simulation testing

- 6.6 Gas diffusion test

- 6.7 Other test types

Chapter 7 Market Estimates and Forecast, By Application, 2021 — 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chronic obstructive pulmonary disease

- 7.3 Asthma

- 7.4 Chronic shortness of breath

- 7.5 Pulmonary fibrosis

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 — 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals & clinics

- 8.3 Diagnostic centers

- 8.4 Homecare settings

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 — 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Baxter

- 10.2 CHEST M.I

- 10.3 COSMED

- 10.4 ECO MEDICS

- 10.5 FUKUDA SANGYO

- 10.6 GANSHORN SCHILLER GROUP

- 10.7 Geratherm Respiratory

- 10.8 medical equipment europe

- 10.9 MGC DIAGNOSTICS

- 10.10 MINATO MEDICAL SCIENCE

- 10.11 MORGAN

- 10.12 ndd Medical Technologies

- 10.13 PHILIPS

- 10.14 Vitalograph

- 10.15 Vyaire MEDICAL