|

市場調査レポート

商品コード

1684815

電解槽市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Electrolyzer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電解槽市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

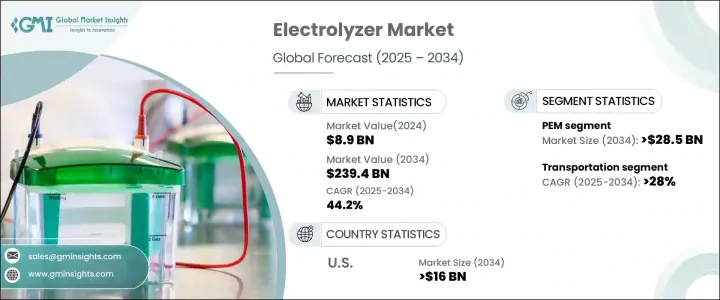

電解槽の世界市場は2024年に89億米ドルに達し、2025年から2034年までのCAGRは44.2%と堅調な予測で、著しい成長を遂げようとしています。

電気分解による水素製造を可能にする電解槽は、クリーンエネルギーの主要技術として大きな注目を集めています。このプロセスは、電力によって水を水素と酸素に分解します。電解槽は、風力や太陽光などの再生可能エネルギー源と組み合わされることで、持続可能なエネルギーの未来への移行において極めて重要な役割を果たします。電解によって製造された水素は、さまざまな産業用途、エネルギー貯蔵システム、輸送に使用することができ、世界の脱炭素化への取り組みにおいて、水素をゲームチェンジャーとして位置づけることができます。

よりクリーンな代替燃料としてグリーン水素への注目が高まるにつれ、世界中の政府や企業が持続可能なエネルギー・ソリューションへの投資を強化する中、電解槽の需要が加速しています。世界各国が排出量削減とエネルギー安全保障向上のためにより厳しい政策を採用する中、電解槽はクリーン・エネルギー・ミックスの不可欠な一部となりつつあります。これらのシステムは、特に化学生産、モビリティ、発電などの産業が水素ベースのソリューションにシフトするにつれて、水素サプライチェーンにおいても牽引力を増しています。技術が成熟するにつれ、システム効率の向上と、風力や太陽光発電のような断続的な再生可能エネルギー源との統合が、さらに大きな需要を牽引しています。さらに、有利な規制枠組み、補助金、脱炭素化目標が大規模な導入を後押ししており、今後10年間の市場見通しは明るいです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 89億米ドル |

| 予測金額 | 2,394億米ドル |

| CAGR | 44.2% |

電解槽市場は製品タイプ別に区分され、プロトン交換膜(PEM)電解槽は2034年までに285億米ドルの市場規模になると予測されます。PEM電解槽は、電気を水素に変換する優れた効率性で知られ、特に再生可能エネルギーの供給が変動する環境において高い評価を得ています。その迅速な応答時間とスケーラビリティは、大規模なアプリケーションに理想的であり、研究開発への投資の増加がその採用を加速すると予想される理由です。現場での水素生成、エネルギー貯蔵、系統安定化ソリューションを支援する金融優遇措置は、メーカーに新たなビジネスチャンスをもたらし、効率的で費用対効果の高い水素生成技術に対する需要の高まりに対応するための生産急増を促しています。

輸送分野は電解槽市場の重要な促進要因であり、2034年までのCAGRは28%と予想されます。燃料電池車開発への投資の波は、炭素排出を抑制する規制の義務化と相まって、モビリティ・ソリューションへの水素の採用を後押ししています。自動車産業が水素ベースの代替燃料に軸足を移す中、メーカー各社は再生可能燃料を輸送網に統合することに注力しています。政府の支援による研究とパイロット・プロジェクトが商業化を加速させ、水素を持続可能なモビリティへのシフトにおける主要プレーヤーとして位置づけています。

米国の電解槽市場は、2034年までに160億米ドルを生み出すと予想されています。助成金や税額控除を含む政府のインセンティブが、水素製造に有利な投資環境を作り出しています。最近のインフラ投資など、クリーンエネルギーに焦点を当てた連邦政策も、この分野の成長を後押ししています。脱炭素プロセスにおける高純度水素に対する産業界の需要の高まりが、大規模電解槽の設置をさらに後押ししています。エネルギー多消費型産業がよりクリーンな代替エネルギーへの移行を進める中、水素の採用が加速しており、世界の電解槽市場における米国の地位は確固たるものとなっています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場の定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- アルカリ

- PEM

- 固体酸化物

- その他

第6章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 500 kW以下

- 500kW~2MW

- 2MW以上

第7章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 発電

- 輸送

- エネルギー産業

- 産業用原料

- ビル熱電併給

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- オランダ

- デンマーク

- スペイン

- ノルウェー

- アジア太平洋

- 中国

- オーストラリア

- 日本

- インド

- 世界のその他の地域

第9章 企業プロファイル

- Air Liquide

- Asahi Kasei

- Erredue

- Hystar

- IHT

- ITM Power

- McPhy Energy

- Nel

- Plug Power

- Siemens

- Sunfire

- Thyssenkrupp Nucera

- Toshiba

The Global Electrolyzer Market reached USD 8.9 billion in 2024 and is poised for remarkable growth, with projections showing a robust CAGR of 44.2% from 2025 to 2034. Electrolyzers, which enable hydrogen production through electrolysis, are gaining significant attention as a key technology for clean energy. This process splits water into hydrogen and oxygen when powered by electricity. When integrated with renewable energy sources such as wind and solar, electrolyzers play a pivotal role in the transition to a sustainable energy future. Hydrogen produced through electrolysis can be used in a variety of industrial applications, energy storage systems, and transportation, positioning it as a game-changer in decarbonization efforts worldwide.

The increasing focus on green hydrogen as a cleaner fuel alternative is accelerating the demand for electrolyzers as governments and businesses across the globe ramp up investments in sustainable energy solutions. With countries worldwide adopting more stringent policies to reduce emissions and improve energy security, electrolyzers are becoming an essential part of the clean energy mix. These systems are also gaining traction in the hydrogen supply chain, particularly as industries, including chemical production, mobility, and power generation, shift toward hydrogen-based solutions. As the technology matures, rising system efficiency and integration with intermittent renewable energy sources like wind and solar power are driving even greater demand. Furthermore, favorable regulatory frameworks, subsidies, and decarbonization targets are propelling large-scale adoption, ensuring a bright market outlook for the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $239.4 Billion |

| CAGR | 44.2% |

The electrolyzer market is segmented by product type, with Proton Exchange Membrane (PEM) electrolyzers expected to generate USD 28.5 billion by 2034. PEM electrolyzers are renowned for their superior efficiency in converting electricity into hydrogen, particularly in settings with fluctuating renewable energy supply. Their rapid response times and scalability make them ideal for large-scale applications, which is why increasing investments in research and development are expected to accelerate their adoption. Financial incentives supporting on-site hydrogen generation, energy storage, and grid stabilization solutions are creating new business opportunities for manufacturers, prompting a surge in production to meet the growing demand for efficient, cost-effective hydrogen generation technologies.

The transportation segment is a significant growth driver for the electrolyzer market, with an anticipated CAGR of 28% through 2034. A wave of investments in fuel cell vehicle development, coupled with regulatory mandates to curb carbon emissions, is boosting the adoption of hydrogen in mobility solutions. As the automotive industry pivots toward hydrogen-based alternatives, manufacturers are focusing on integrating renewable fuels into transportation networks while advancements in hydrogen refueling infrastructure continue to enhance product deployment. Government-backed research and pilot projects are accelerating commercialization, positioning hydrogen as a leading player in the shift to sustainable mobility.

The US electrolyzer market is expected to generate USD 16 billion by 2034. Government incentives, including grants and tax credits, are creating a favorable investment climate for hydrogen production. Federal policies focused on clean energy, such as recent infrastructure investments, are also driving the growth of the sector. Rising industrial demand for high-purity hydrogen in decarbonization processes is further boosting large-scale electrolyzer installations. As energy-intensive industries increasingly transition to cleaner alternatives, hydrogen adoption is picking up pace, solidifying the US's position in the global electrolyzer market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Alkaline

- 5.3 PEM

- 5.4 Solid Oxide

- 5.5 Others

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 ≤ 500 kW

- 6.3 > 500 kW – 2 MW

- 6.4 Above 2 MW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 Power Generation

- 7.3 Transportation

- 7.4 Industry Energy

- 7.5 Industry Feedstock

- 7.6 Building Heat & Power

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Netherlands

- 8.3.6 Denmark

- 8.3.7 Spain

- 8.3.8 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 India

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Air Liquide

- 9.2 Asahi Kasei

- 9.3 Erredue

- 9.4 Hystar

- 9.5 IHT

- 9.6 ITM Power

- 9.7 McPhy Energy

- 9.8 Nel

- 9.9 Plug Power

- 9.10 Siemens

- 9.11 Sunfire

- 9.12 Thyssenkrupp Nucera

- 9.13 Toshiba