暗号化ソフトウェアの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Encryption Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684798

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

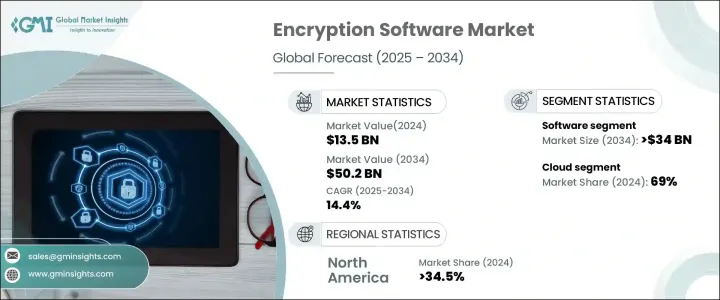

暗号化ソフトウェアの世界市場は、2024年に135億米ドルと評価され、2025年から2034年にかけてCAGR14.4%で成長する見通しです。

世界中の企業がサイバー脅威の増大、データ漏洩、コンプライアンス規制の強化に直面する中、強固な暗号化ソリューションに対する需要は高まり続けています。各業界の組織は、機密データを保護し、サイバーセキュリティリスクを軽減し、進化する規制要件を満たすために、暗号化ソフトウェアを優先しています。技術の急速な進歩に伴い、暗号化ソフトウェアはより洗練され、人工知能、ブロックチェーン、量子暗号を活用して次世代のセキュリティソリューションを提供しています。

AIを活用した暗号化は、新たな脅威に継続的に適応し、リアルタイムのリスク検知を向上させることで、データ保護を再定義しています。一方、ブロックチェーンベースの暗号化は、改ざん防止されたデータ転送を保証することでセキュリティを強化し、金融取引、ヘルスケア記録、政府通信に理想的なものとなっています。量子暗号化はまだ初期段階ですが、量子力学の原理を活用して不正アクセスを防止することで、前例のないレベルのデータセキュリティを約束します。デジタルトランスフォーメーションが加速する中、企業は信頼を維持し、知的財産を保護し、重要なインフラを保護するために、暗号化技術に多額の投資を行っています。クラウドコンピューティング、モノのインターネット(IoT)デバイス、リモートワークの急激な増加は、分散ネットワーク上のデータを保護する高度な暗号化ソリューションの必要性をさらに強調しています。市場の成長軌道は、サイバーセキュリティのフレームワーク強化を求める世界の動きを反映しており、企業も政府も同様に、暗号化をサイバー脅威に対する不可欠な防御手段として認識しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 135億米ドル |

| 予測金額 | 502億米ドル |

| CAGR | 14.4% |

2024年に市場シェアの70%を占めたソフトウェア分野は、2034年までに340億米ドルを生み出すと予測されています。さまざまなネットワーク、ストレージシステム、デジタルプラットフォームにわたって機密情報を保護できることから、企業は引き続き暗号化ソフトウェアを支持しています。サイバー攻撃の急増により、企業は構造化データと非構造化データの両方を保護する最先端の暗号化ツールを導入する必要性が高まっています。金融、ヘルスケア、小売などの業界では、厳格なデータ保護法を遵守すると同時に、顧客や社内業務のシームレスなセキュリティを確保するために、暗号化ソフトウェアに依存しています。

クラウドベースのデータストレージとコンピューティングへの移行が広がっていることを反映して、2024年の暗号化ソフトウェア市場シェアの69%をクラウド展開が占めました。企業はますます業務をクラウドに移行しており、サイバー脅威や不正アクセスから機密情報を保護するための強力な暗号化対策が必要となっています。クラウドネイティブの暗号化ソリューションは、データの完全性、コンプライアンス、アクセス制御に関する懸念の高まりに対応し、保存中と転送中の両方でデータの安全性を確保します。企業は、暗号化がGDPR、CCPA、HIPAAなどの枠組みの規制コンプライアンスを維持する上で重要な役割を果たすことを認識しており、高度なクラウドセキュリティソリューションへの投資の増加につながっています。

北米は、2024年の暗号化ソフトウェア市場で34.5%のシェアを占め、サイバーセキュリティ革新の重要な拠点としての地位を確立しました。技術インフラが整備され、データプライバシー規制が厳しいこの地域の企業は、暗号化ソフトウェアをセキュリティ戦略に積極的に組み込んでいます。金融セクター、ヘルスケア産業、政府機関は、高価値資産の保護、データ漏洩の防止、安全な取引の確保のために暗号化を優先しています。サイバーセキュリティリスクに対する意識の高まりは、デジタルトランスフォーメーションへの投資の増加と相まって、引き続き市場拡大の原動力となっています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- クラウドサービスプロバイダー

- マネージドセキュリティサービスプロバイダー

- 暗号化ソフトウェアインテグレーター

- エンドユーザー

- 利益率分析

- テクノロジーとイノベーションの展望

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 成長促進要因

- データセキュリティに対する懸念の高まり

- データ量の増加

- クラウドサービスの普及

- 暗号化技術の革新

- 業界の潜在的リスク・課題

- 導入の複雑さとコスト

- 既存システムとの統合課題

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- エンドポイント暗号化

- 電子メール暗号化

- クラウド暗号化

- ディスク暗号化

- データベース暗号化

- その他

- サービス内容

- トレーニング・コンサルティング

- インテグレーション・メンテナンス

- マネージドサービス

第6章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- IT・通信

- BFSI

- ヘルスケア

- 小売

- 政府・公共部門

- 製造業

- その他

第8章 市場規模推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AO Kaspersky Lab

- Bitdefender

- Broadcom

- Check Point Software

- Cisco Systems

- Dell Technologies

- ESET

- F-Secure

- HPE

- IBM

- McAfee

- Microsoft

- OpenText

- Oracle

- Palo Alto

- Panda Security

- Proofpoint

- Sophos Ltd.

- Thales

- Trend Micro

目次

The Global Encryption Software Market, valued at USD 13.5 billion in 2024, is on track to grow at a CAGR of 14.4% between 2025 and 2034. As businesses worldwide face increasing cyber threats, data breaches, and stricter compliance regulations, the demand for robust encryption solutions continues to rise. Organizations across industries prioritize encryption software to safeguard sensitive data, mitigate cybersecurity risks, and meet evolving regulatory requirements. With rapid technological advancements, encryption software is now more sophisticated, leveraging artificial intelligence, blockchain, and quantum encryption to provide next-generation security solutions.

AI-driven encryption is redefining data protection by continuously adapting to new threats and improving real-time risk detection. Meanwhile, blockchain-based encryption enhances security by ensuring tamper-proof data transfers, making it ideal for financial transactions, healthcare records, and government communications. Quantum encryption, though still in its early stages, promises an unprecedented level of data security by leveraging the principles of quantum mechanics to prevent unauthorized access. As digital transformation accelerates, enterprises are investing heavily in encryption technologies to maintain trust, protect intellectual property, and secure critical infrastructure. The exponential growth of cloud computing, Internet of Things (IoT) devices, and remote workforces further underscores the necessity for advanced encryption solutions that protect data across distributed networks. The market's upward trajectory reflects a global push for stronger cybersecurity frameworks, with businesses and governments alike recognizing encryption as an essential defense against cyber threats.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.5 Billion |

| Forecast Value | $50.2 Billion |

| CAGR | 14.4% |

The software segment, which accounted for 70% of the market share in 2024, is set to generate USD 34 billion by 2034. Companies continue to favor encryption software due to its ability to secure sensitive information across various networks, storage systems, and digital platforms. The surge in cyberattacks has heightened the need for businesses to deploy cutting-edge encryption tools that protect both structured and unstructured data. Industries such as finance, healthcare, and retail rely on encryption software to comply with stringent data protection laws while ensuring seamless security for their customers and internal operations.

Cloud deployment accounted for 69% of the encryption software market share in 2024, reflecting the widespread shift toward cloud-based data storage and computing. Businesses increasingly migrate their operations to the cloud, necessitating strong encryption measures to protect sensitive information from cyber threats and unauthorized access. Cloud-native encryption solutions ensure data remains secure both in storage and in transit, addressing growing concerns over data integrity, compliance, and access control. Enterprises recognize the critical role encryption plays in maintaining regulatory compliance with frameworks such as GDPR, CCPA, and HIPAA, leading to increased investment in advanced cloud security solutions.

North America held a 34.5% share of the encryption software market in 2024, establishing itself as a key hub for cybersecurity innovation. With a well-developed technological infrastructure and stringent data privacy regulations, businesses in the region actively integrate encryption software into their security strategies. The financial sector, healthcare industry, and government institutions prioritize encryption to protect high-value assets, prevent data breaches, and ensure secure transactions. Growing awareness of cybersecurity risks, coupled with increasing investments in digital transformation, continues to drive market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud service providers

- 3.2.2 Managed security service providers

- 3.2.3 Encryption software integrators

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising data security concerns

- 3.7.1.2 Increasing data volume

- 3.7.1.3 Proliferation of cloud services

- 3.7.1.4 Innovations in encryption technologies

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Complexity and cost of implementation

- 3.7.2.2 Integration challenges with existing systems

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Endpoint encryption

- 5.2.2 Email encryption

- 5.2.3 Cloud encryption

- 5.2.4 Disk encryption

- 5.2.5 Database encryption

- 5.2.6 Others

- 5.3 Services

- 5.3.1 Training & consulting

- 5.3.2 Integration & maintenance

- 5.3.3 Managed service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 IT & telecom

- 7.3 BFSI

- 7.4 Healthcare

- 7.5 Retail

- 7.6 Government & public sector

- 7.7 Manufacturing

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AO Kaspersky Lab

- 10.2 Bitdefender

- 10.3 Broadcom

- 10.4 Check Point Software

- 10.5 Cisco Systems

- 10.6 Dell Technologies

- 10.7 ESET

- 10.8 F-Secure

- 10.9 HPE

- 10.10 IBM

- 10.11 McAfee

- 10.12 Microsoft

- 10.13 OpenText

- 10.14 Oracle

- 10.15 Palo Alto

- 10.16 Panda Security

- 10.17 Proofpoint

- 10.18 Sophos Ltd.

- 10.19 Thales

- 10.20 Trend Micro

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日