|

市場調査レポート

商品コード

1684729

長期進化型基地局市場の機会、成長促進要因、産業動向分析、2025~2034年予測Long-Term Evolution Base Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 長期進化型基地局市場の機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月18日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

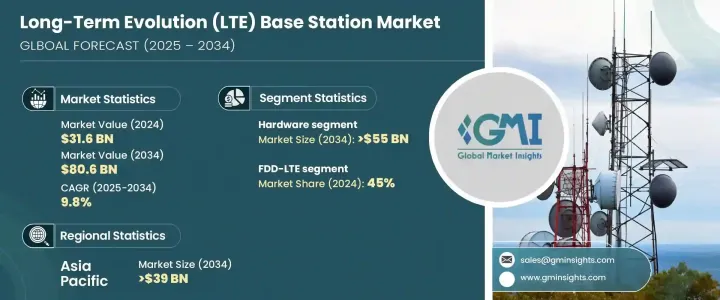

世界の長期進化型基地局市場は2024年に316億米ドルと評価され、2025年から2034年にかけてCAGR 9.8%と予測され、大きな成長を遂げようとしています。

この急拡大の背景には、高速モバイルインターネットへの需要の高まり、モバイルデータ消費の急増、高度なワイヤレスネットワークの広範な展開があります。モバイルユーザーがシームレスな接続性を求め続ける中、時代遅れの3GネットワークからLTE、そしてそれ以上への移行が必須となっています。スマートデバイスやモノのインターネット(IoT)の普及が進むにつれ、より信頼性が高く効率的なネットワークインフラへのニーズがさらに高まっています。また、LTE基地局の展開を進める上で、世界各国の政府の取り組みも重要な役割を果たしており、ネットワークのアップグレードや5G対応ソリューションの統合に多額の投資が行われています。その結果、LTEインフラはもはや単なる接続オプションではなく、現代のデジタル・エコシステムのバックボーンとなり、高速で中断のない通信を求める企業や消費者を同様にサポートしています。

市場はハードウェアとソフトウェアに区分され、2024年の市場シェアはハードウェアが65%を占めています。この分野は、技術の進歩によって効率と性能の向上が促進されるため、2034年には550億米ドルに達すると予想されています。ハードウェアの状況を形成する最も注目すべき動向のひとつは、基地局とアンテナの小型化です。この技術革新により、ネットワーク・プロバイダーはコンパクトでスペース効率の高い形式で高性能ソリューションを展開できるようになりました。さらに、メーカー各社はエネルギー効率の高いハードウェア・コンポーネントを優先的に採用し、ピーク時のネットワーク性能を維持しながら消費電力を最適化しています。モジュラー・ハードウェア設計は勢いを増しており、ネットワークのアップグレードを簡素化し、既存のインフラを将来にわたって保護するスケーラブルなソリューションを提供しています。LTEネットワークが拡大するにつれて、事業者は、中断のない接続性に対する増大し続ける需要に対応するため、コスト効率に優れた高性能ハードウェアソリューションをますます求めるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 316億米ドル |

| 予測金額 | 806億米ドル |

| CAGR | 9.8% |

LTE基地局市場は3つの主要技術セグメントに分けられる:FDD-LTE、TDD-LTE、スモールセルです。FDD-LTEは、主にアップロードとダウンロードの速度をバランスよく提供できることから、2024年のシェアは45%と圧倒的です。この技術は、都市部と郊外にまたがるシームレスなユーザー体験を保証するため、データトラフィックの多い地域に特に適しています。特に新興国市場では、FDD-LTEインフラの持続的な拡大が続いており、その普及を後押ししています。さらに、ネットワーク・プロバイダーは、堅牢な接続性を維持しながら運用コストを削減するエネルギー効率の高い基地局に投資しています。拡張性とコスト効率に優れたLTEソリューションへのニーズが高まる中、FDD-LTEはネットワーク事業者と消費者の双方にとって好ましい選択肢であり続けています。

アジア太平洋地域は2024年に39%のシェアを獲得して世界のLTE基地局市場をリードし、2034年には390億米ドルを超えると予測されています。中国のような主要市場におけるLTEの急速な普及が、この成長の大きな原動力となっています。スペクトラム効率の高さで知られるTDD-LTE技術の導入が進んでいることも、この地域の優位性をさらに強めています。アジア太平洋諸国が次世代接続ソリューションへの投資を続ける中、LTE市場は拡大し、現行技術と来るべき5G革命とのギャップを埋めることになると思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品サプライヤー

- 機器メーカー

- ソフトウェアプロバイダー

- システム・インテグレーター

- 電気通信事業者

- エンドユーザー

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- コスト内訳分析

- 主要ニュースと取り組み

- 規制状況

- 技術の差別化要因

- FDD-LTE対TDD-LTE

- マイクロvsピコ vsフェムト

- 影響要因

- 促進要因

- 高速モバイル・ブロードバンドに対する需要の高まり

- モバイル・データ・トラフィックと消費量の増加

- 世界の4GおよびLTEネットワークの拡大

- IoTおよびコネクテッド・デバイスの採用拡大

- 業界の潜在的リスク&課題

- LTEネットワーク・インフラ展開の高コスト

- 周波数割り当てと管理の課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ベースバンドユニット(BBU)

- リモート無線ユニット(RRU)

- アンテナ

- パワーアンプ

- 冷却システム

- ソフトウェア

- 基地局コントローラー

- ネットワーク管理ソフトウェア

- 最適化ツール

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- FDD-LTE

- TDD-LTE

- スモールセル

第7章 市場推計・予測:プロビジョン別、2021年~2034年

- 主要動向

- 都市部

- 郊外

- 農村部

第8章 市場推計・予測:エンドユーザー別、2021年~2034年

- 主要動向

- 住宅・SOHO

- 企業

- 通信事業者

- 官公庁

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Airspan

- Alpha Wireless

- AT&T

- Baicells

- Blinq Networks

- Cassava Technologies

- Cisco

- CommScope

- Ericsson

- Fujitsu

- Huawei

- Motorola

- NEC

- Nokia

- NuRAN Solutions

- Qualcomm

- Samsung

- Tektelic Communications

- ZTE

The Global Long-Term Evolution Base Station Market, valued at USD 31.6 billion in 2024, is poised for significant growth, with projections indicating a CAGR of 9.8% between 2025 and 2034. This rapid expansion is fueled by the increasing demand for high-speed mobile internet, surging mobile data consumption, and the widespread deployment of advanced wireless networks. As mobile users continue to expect seamless connectivity, the transition from outdated 3G networks to LTE and beyond has become a necessity. The growing penetration of smart devices and the Internet of Things (IoT) is further intensifying the need for more reliable and efficient network infrastructure. Government initiatives worldwide are also playing a crucial role in advancing LTE base station deployment, with substantial investments in network upgrades and the integration of 5G-ready solutions. As a result, LTE infrastructure is no longer just a connectivity option; it has become the backbone of modern digital ecosystems, supporting businesses and consumers alike in their quest for high-speed, uninterrupted communication.

The market is segmented into hardware and software, with the hardware segment accounting for 65% of the market share in 2024. This segment is expected to reach USD 55 billion by 2034 as technological advancements drive efficiency and performance improvements. One of the most notable trends shaping the hardware landscape is the miniaturization of base stations and antennas. This innovation allows network providers to deploy high-performance solutions in compact and space-efficient formats. Additionally, manufacturers are prioritizing energy-efficient hardware components to optimize power consumption while maintaining peak network performance. Modular hardware designs are gaining momentum, offering scalable solutions that simplify network upgrades and future-proof existing infrastructure. As LTE networks expand, operators are increasingly looking for cost-effective, high-performance hardware solutions to meet the ever-growing demand for uninterrupted connectivity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $31.6 billion |

| Forecast Value | $80.6 billion |

| CAGR | 9.8% |

The LTE base station market is divided into three key technology segments: FDD-LTE, TDD-LTE, and small cells. FDD-LTE held a dominant 45% share in 2024, primarily due to its ability to deliver balanced upload and download speeds. This technology is particularly well-suited for regions with high data traffic, as it ensures a seamless user experience across urban and suburban areas. The sustained expansion of FDD-LTE infrastructure, especially in developed markets, continues to drive its adoption. Additionally, network providers are investing in energy-efficient base stations that lower operational costs while maintaining robust connectivity. With the growing need for scalable and cost-effective LTE solutions, FDD-LTE remains a preferred choice for both network operators and consumers.

Asia Pacific led the global LTE base station market with a 39% share in 2024 and is projected to surpass USD 39 billion by 2034. Rapid LTE adoption in key markets like China is a major driving force behind this growth, supported by government-backed network upgrades and a rising demand for mobile data. The increasing deployment of TDD-LTE technology, known for its spectrum efficiency, further strengthens the region's dominance. As Asia Pacific nations continue investing in next-generation connectivity solutions, the LTE market is set to expand, bridging the gap between current technologies and the upcoming 5G revolution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Equipment manufacturers

- 3.2.3 Software providers

- 3.2.4 System integrators

- 3.2.5 Telecom operators

- 3.2.6 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Technology differentiators

- 3.9.1 FDD-LTE vs TDD-LTE

- 3.9.2 Micro vs Pico vs Femto

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for high-speed mobile broadband

- 3.10.1.2 Increasing mobile data traffic and consumption

- 3.10.1.3 Expansion of 4G and LTE networks worldwide

- 3.10.1.4 Growing adoption of IoT and connected devices

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High cost of LTE network infrastructure deployment

- 3.10.2.2 Challenges in spectrum allocation and management

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Baseband units (BBU)

- 5.2.2 Remote radio units (RRU)

- 5.2.3 Antennas

- 5.2.4 Power amplifiers

- 5.2.5 Cooling systems

- 5.3 Software

- 5.3.1 Base station controllers

- 5.3.2 Network management software

- 5.3.3 Optimization tools

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 FDD-LTE

- 6.3 TDD-LTE

- 6.4 Small cells

Chapter 7 Market Estimates & Forecast, By Provision, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Urban

- 7.3 Suburban

- 7.4 Rural

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Residential & SOHO

- 8.3 Enterprise

- 8.4 Telecom operators

- 8.5 Government and public sector

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Number of base stations)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airspan

- 10.2 Alpha Wireless

- 10.3 AT&T

- 10.4 Baicells

- 10.5 Blinq Networks

- 10.6 Cassava Technologies

- 10.7 Cisco

- 10.8 CommScope

- 10.9 Ericsson

- 10.10 Fujitsu

- 10.11 Huawei

- 10.12 Motorola

- 10.13 NEC

- 10.14 Nokia

- 10.15 NuRAN Solutions

- 10.16 Qualcomm

- 10.17 Samsung

- 10.18 Tektelic Communications

- 10.19 ZTE